Valued at a market cap of $6.1 billion, The Campbell's Company (CPB) is a leading packaged food manufacturer with a portfolio centered on meals, snacks, and pantry staples. Headquartered in Camden, New Jersey, the company has evolved from its iconic canned soup roots into a broader branded food business with strong positions in both grocery and snacking categories.

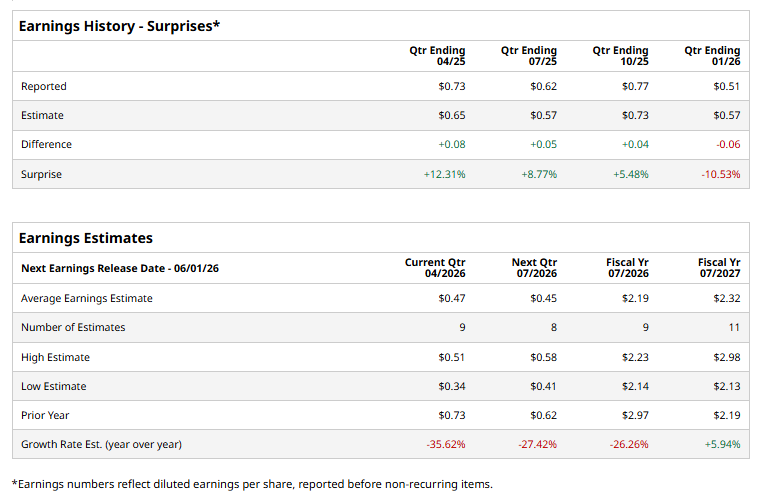

CPB is expected to announce its fiscal Q3 2026 earnings results shortly. Ahead of this event, analysts expect Campbell to report adjusted earnings of $0.47 per share, a 35.6% decline from $0.73 per share in the year-ago quarter. Moreover, the company has surpassed Wall Street's earnings estimates in three of the last four quarters, while missing on another occasion.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For fiscal 2026, analysts expect Campbell to report an adjusted EPS of $2.19, down 26.3% from $2.97 in fiscal 2025. But, adjusted EPS is projected to rebound in FY2027, rising 5.9% annually to $2.32.

www.barchart.com

www.barchart.comCPB stock has declined 43.9% over the past 52 weeks, considerably trailing both the S&P 500 Index's ($SPX) 30.6% surge and the Consumer Staples Select Sector SPDR Fund’s (XLP) 2.7% return over the same period.

www.barchart.com

www.barchart.comCampbell's has trailed the broader market over the past year primarily due to muted growth and margin pressures typical of the consumer staples sector. While demand for its products remains relatively stable, volume softness, as consumers trade down to private labels or shift toward fresher alternatives, has limited revenue momentum. Additionally, in a market increasingly driven by high-growth, tech-oriented stocks, Campbell’s defensive, low-growth profile has made it less attractive to investors, contributing to its relative underperformance.

Analysts' consensus view on Campbell’s stock is cautious, with a "Hold" rating overall. Among 20 analysts covering the stock, two recommend a "Strong Buy," 12 suggest "Hold," one advises "Moderate Sell," and five "Strong Sells." Its mean price target of $22.53 indicates an upswing potential of 9.3% from the prevailing market prices.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

3 Under-the-Radar Dividend Stocks Yielding Up to 13% That Wall Street Rates a Strong Buy Intel Is Leading SanDisk Higher. Should You Chase SNDK Stock Today? Should You Buy the Dip in Oracle Stock? Dan Ives Thinks So. Much Like Their Pants, I’m Not Ready for Another Tight Squeeze with Lululemon’s Stock