Electric Vehicle (EV) giant Tesla (TSLA) has just reported its fiscal Q1 2026 earnings, and it’s the kind of quarter that keeps the Tesla story as polarizing as ever. The results came in mixed, leaving Wall Street split on the near-term outlook, while a larger-than-expected capex push raised fresh questions around spending. Yet, amid the noise, management chose to spotlight what could be a defining milestone.

On the earnings call, CEO Elon Musk confirmed that production of the long-awaited Cybercab robotaxi has officially begun at Giga Texas, with ramps now underway as of April 2026. The first steering-wheel-less unit rolled off the line back in February, but continuous production has only just started this month. For now, Tesla is building both versions, a fully autonomous model without a steering wheel and another with one, keeping its options open as autonomy technology continues to evolve.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Moreover, Musk cautioned investors that the company has just started Cybercab production while emphasizing that any new product with a completely new supply chain follows a stretched S-curve. That means initial production of Cybercab and Semi is expected to be slow before ramping sharply and potentially turning exponential toward the end of the year. Strategically, Cybercab sits at the center of Tesla’s long-term vision. Musk pointed out that most trips involve one or two passengers, making a purpose-built robotaxi the logical direction for mass adoption.

Over time, this could shift a significant share of Tesla’s production mix toward Cybercab. The real bottleneck, however, remains autonomy. The Cybercab is designed to run without a driver, but truly unsupervised self-driving is still out of reach. Elon Musk said Full Self-Driving (FSD) will make its way to customer vehicles around Q4 this year, but if history is any guide, Tesla’s FSD timelines have a habit of stretching well beyond initial targets. Nevertheless, with Cybercab now finally transitioning from concept to production reality, here’s a closer look at TSLA stock.

About Tesla Stock

Founded in 2003 and headquartered in Austin, Texas, Tesla began as a bold bet on EVs, and has since evolved into something far bigger. What started with sleek EVs like the Model Y and Model 3 has transformed into a full-scale technology ecosystem spanning energy storage, solar solutions, and cutting-edge manufacturing. Under the leadership of Elon Musk, Tesla isn’t just selling cars anymore. The company is building Gigafactories across the globe, pushing the boundaries of autonomous driving, and doubling down on artificial intelligence (AI) with initiatives like FSD and the Optimus humanoid robot.

Today, Tesla sits at the intersection of EVs, physical AI, and energy innovation, positioning itself not just as an automaker but as a company aiming to redefine how the world moves, powers, and automates its future. Currently valued at around $1.40 trillion by market capitalization, TSLA stock has come under pressure this year, weighed down by a slowing EV business, heavy capex plans, and rising concerns over its ambitious pivot toward becoming a physical AI company.

After rallying 45% in 2025, TSLA’s momentum has stalled in 2026, with shares sliding nearly 16.43% year-to-date (YTD), sharply underperforming the S&P 500 Index ($SPX), which is up about 4.67% during the same stretch. The reversal is even more pronounced from its December peak of $498.83, with the stock now down 32.6%, signaling a notable shift in investor sentiment.

www.barchart.com

www.barchart.com Tesla’s Q1 Earnings Snapshot

Tesla’s Q1 2026 earnings, released on April 22, underscored a company deep in the middle of a capital-heavy transformation, one that sparked a 3.6% sell-off in the following session. On the surface, the numbers impressed. Revenue climbed 16% year-over-year (YOY) to $22.39 billion, beating expectations of $21.92 billion, while adjusted EPS came in at $0.41, comfortably ahead of the $0.36 consensus and surging 52% from a year ago. Beneath that headline strength, the core EV business remained the primary engine.

Automotive revenue rose 16% to $16.2 billion from $14 billion last year, reinforcing that the legacy business is still carrying the weight. Profitability also staged a notable comeback. Total GAAP gross margin expanded to 21.1%, up sharply from 16.3% a year ago, while automotive gross margin (excluding regulatory credits) improved to 19.2%, up from 12.5% in Q1 2025 and 17.9% in Q4 2025.

At the same time, Tesla acknowledged intensifying competition and an aging lineup, signaling plans to introduce more affordable trims for its Model Y SUV and Model 3 sedan as rivals, especially Chinese players like BYD Company (BYDDY) and Xiaomi (XIACY), continue to roll out newer, cheaper, and more advanced vehicles. Liquidity remained solid, with quarter-end cash, cash equivalents, and short-term investments at $44.7 billion, up from $44.1 billion sequentially.

The increase was driven by $1.4 billion in free cash flow and $1.2 billion in financing inflows, partially offset by a $2 billion equity investment in SpaceX. However, the defining narrative, and the key driver behind the stock’s pullback, was Tesla’s aggressive spending ramp tied to its “Physical AI” pivot. The company raised its 2026 capex guidance to over $25 billion, a sharp jump from $8.6 billion in 2025, as it pours capital into AI infrastructure, new product launches, and manufacturing scale.

Management cautioned that this investment cycle, particularly around AI training clusters and the Cybercab supply chain, could push free cash flow into negative territory for the rest of the year. Looking forward, the company aims to boost volumes through a tightly managed, high-impact product portfolio while maximizing output from existing factories before committing to new capacity.

Meanwhile, its next wave of products, Cybercab, Semi, and Megapack 3, remains on track for volume production in 2026, with early production lines for Optimus already being installed, signaling that Tesla’s next phase is not just about vehicles, but an integrated AI-powered ecosystem.

What Do Analysts Think About Tesla Stock?

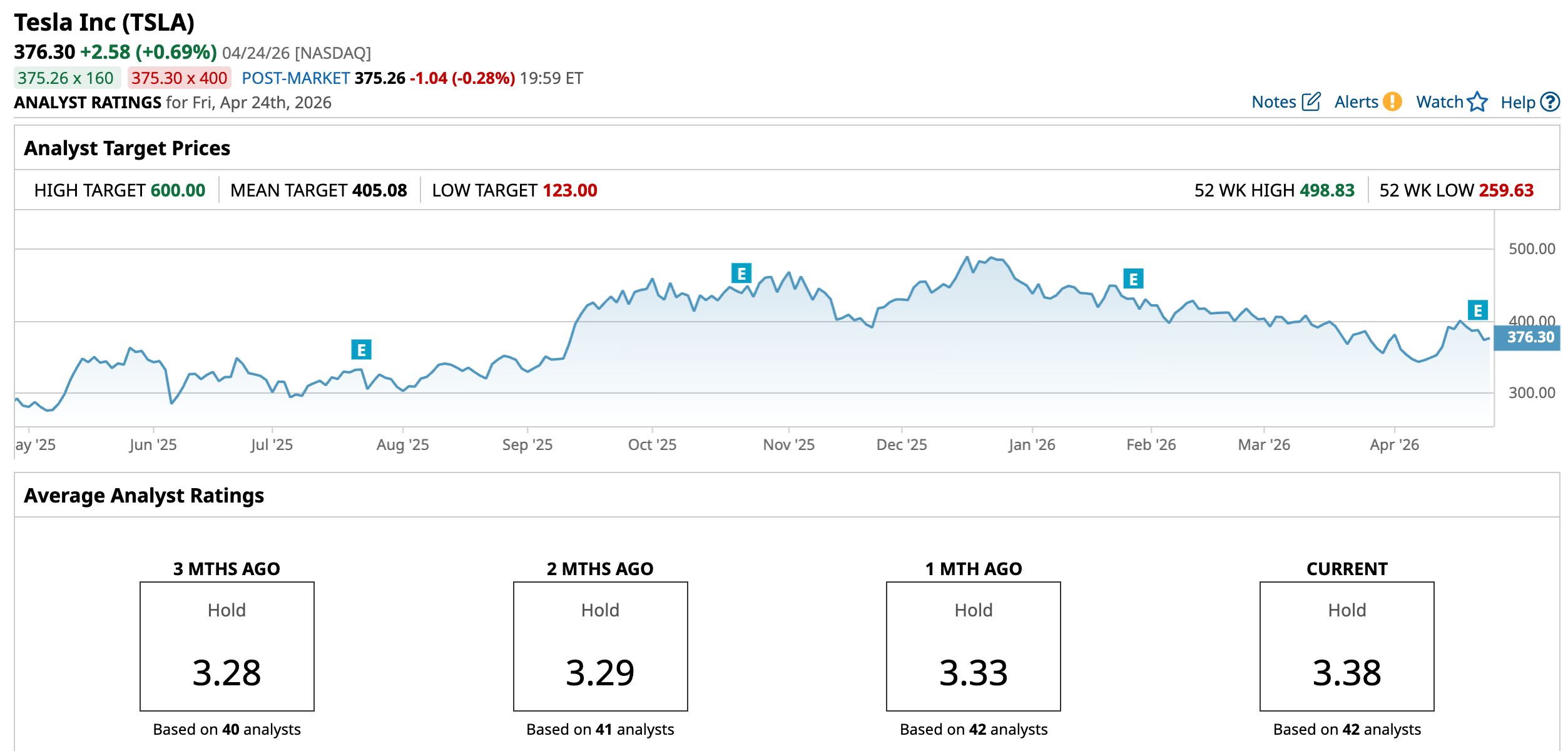

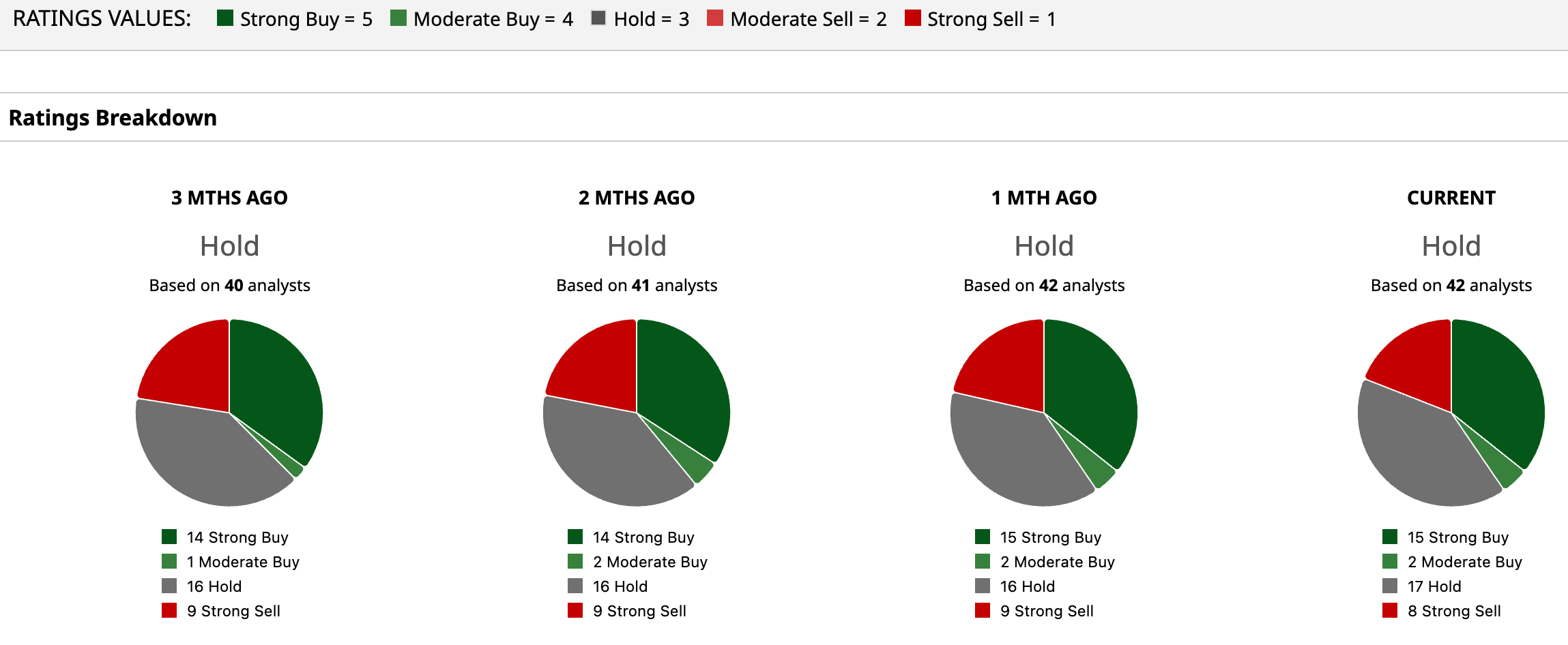

Overall, Wall Street is treading carefully on Tesla, with the stock carrying a consensus “Hold” rating. Out of 42 analysts, sentiment is sharply split, 15 remain firmly bullish with “Strong Buy” calls, two lean “Moderate Buy,” 17 prefer to stay on the sidelines, and eight take a distinctly bearish stance with “Strong Sell” ratings. The average price target of $405.08 suggests a 7.65% upside, but the Street-high target of $600 hints at a far more bullish scenario, implying the stock could rally as much as 59.45% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Better Later Than Never? Tesla Stock Hangs in the Crosshairs as Cybercab Finally Enters Production Intel Could Still Be Undervalued Based on Strong Free Cash Flow Spirit Airlines Stock Is Ready for Takeoff Thanks to Trump, but Can This Plane Stay in the Sky? Dan Ives: Tesla Is ‘Morphing into a Physical AI Stalwart’ So Don’t Sweat the CapEx and Just Buy TSLA Stock