Software stocks continue to lose their charm as artificial intelligence (AI) and chip stocks steal the limelight. The iShares Expanded Tech-Software Sector ETF (IGV) is down 19% so far this year despite a recovery in April. There seems to be no respite for software companies as AI models get better and better by the day. Yet, someone notable has just bet on a rebound for software stocks: Michael Burry.

Burry once called out AI stocks like Microsoft (MSFT) for poor accounting practices to inflate remaining performance obligations, but the famed investor is now backing the company. In his defense, MSFT stock is already down from the time he called out the AI backlog and capex concerns. At one point, MSFT stock was down as much as 35%.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Michael Burry's stake in Microsoft, as well as his stakes in Adobe (ADBE) and PayPal (PYPL), point to a renewed confidence in software and platform stocks, likely because of the beating these names have already taken this year. With that said, it wouldn’t be surprising that, after a horrid first quarter, software stocks post a rebound in the second quarter.

Michael Burry Stock #1: Microsoft (MSFT)

Microsoft (MSFT) is a global technology company that develops and sells a wide range of software, cloud services, devices, and business solutions. It serves both individual users and enterprise customers worldwide. The company operates through multiple segments and offers flagship products including Windows, Microsoft 365, Azure, LinkedIn, and Xbox.

Over the past year, Microsoft has delivered an 8% return, compared to the S&P 500’s ($SPX) gain of around 30%. This underperformance has continued into the current year as well, with the stock giving up all of its earlier gains so far. While the broader market has seen occasional dips due to geopolitical uncertainty, the S&P 500 is still up by more than 4%. In contrast, Microsoft is down 12% year-to-date (YTD).

www.barchart.com

www.barchart.com Microsoft reported its second-quarter fiscal 2026 earnings on Jan. 28, surpassing both earnings and revenue estimates. Revenue for the quarter came in at $81.3 billion, roughly $1.02 billion above consensus estimates. Similarly, the company delivered non-GAAP EPS of $4.14, beating market expectations by about $0.22.

Looking ahead, Q3 revenue is expected to be in a range between $80.65 billion and $81.75 billion, reflecting 15% to 17% growth. Operating expenses are projected to range from $17.8 billion to $17.9 billion, indicating a 10% to 11% increase. Excluding the impact of OpenAI investments, operating margins are forecast to decline slightly year-over-year (YOY). At the same time, gross margin is anticipated to be around 65%, demonstrating a YOY decrease driven by ongoing investments in AI.

On April 16, TD Cowen analyst Derrick Wood reaffirmed a “Buy” rating on MSFT stock with a price target of $540. Jefferies analyst Brent Thill also recently maintained a “Buy” rating on Microsoft while keeping a price target of $675.

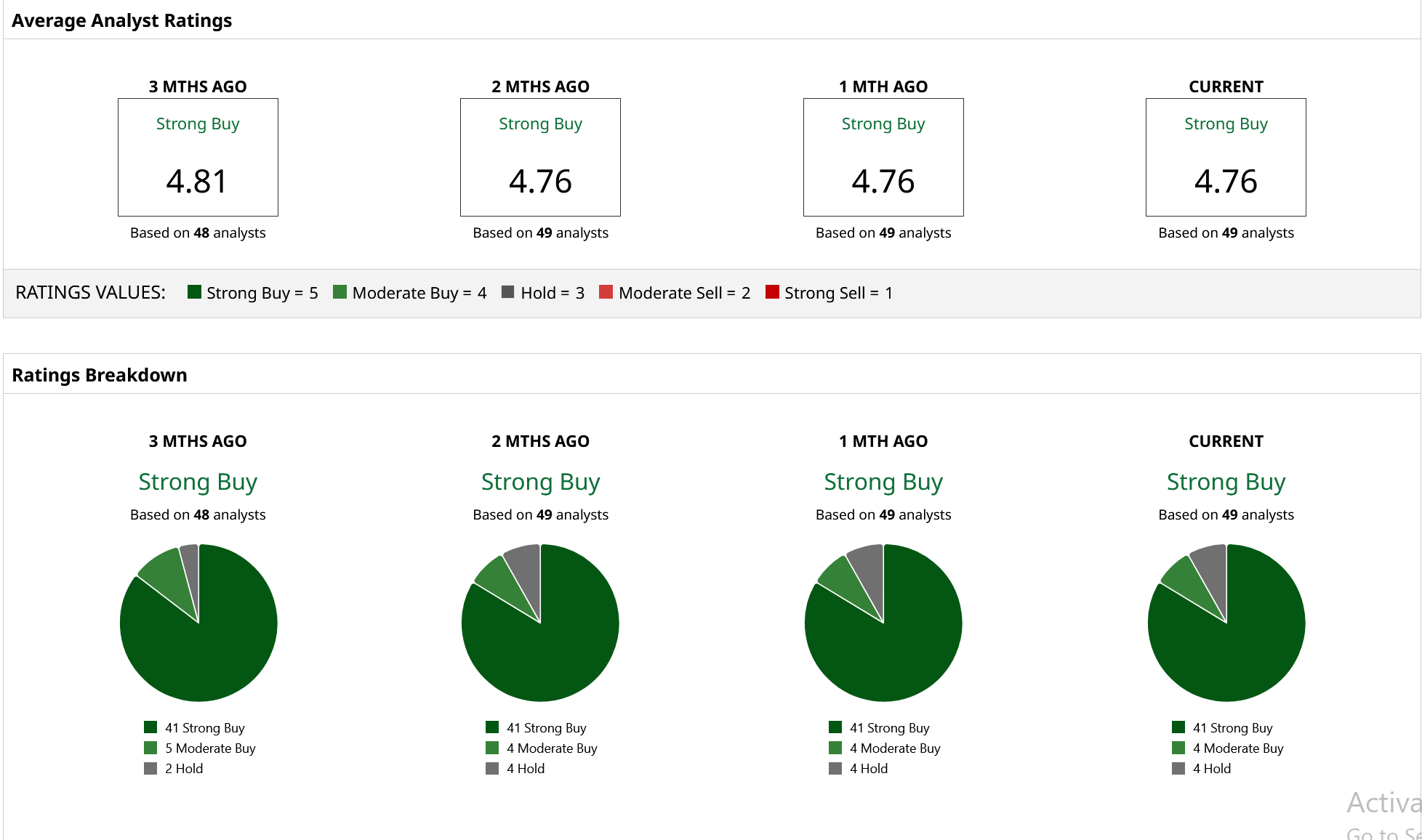

MSFT stock enjoys a consensus “Strong Buy” rating from 49 Wall Street analysts covering the stock. The mean price target of $579.01 implies 36% potential upside from current levels.

www.barchart.com

www.barchart.com Michael Burry Stock #2: Adobe (ADBE)

Adobe (ADBE) is a technology company that helps enterprises, individuals, and teams to publish, create, and promote content. Moreover, the company offers an integrated platform, along with products and services that allow businesses and brands to manage and optimize customer experiences from analytics to commerce.

The S&P 500 has outperformed shares of Adobe over the past year, gaining around 30% while the stock has declined by approximately 35% during the same period. The lack of performance has mainly been due to fears that AI will render most of the company's tools useless.

www.barchart.com

www.barchart.com Adobe posted better-than-expected Q1 fiscal 2026 results on March 12. The company generated $6.4 billion in revenue, beating market expectations by $120 million. On the earnings side, non-GAAP EPS came in at $6.06, exceeding analyst estimates by $0.19.

For Q2, the company projects total revenue to be in the range of $6.43 billion to $6.48 billion. Of this, about $1.8 billion to $1.82 billion is expected to come from Business Professionals & Consumers, while a larger share of $4.41 billion to $4.44 billion is forecast to come from Creative & Marketing Professionals. GAAP EPS is estimated at $4.35 to $4.40, while non-GAAP EPS is estimated at $5.80 to $5.85. The company continues to expect total ARR growth of 10.2% for fiscal 2026.

D.A. Davidson analyst Gil Luria recently reiterated a “Buy” rating on ADBE stock, along with a price target of $300. Stifel analyst J. Parker Lane also has a “Buy” rating on Adobe with a $400 target. Analysts maintaining these positive ratings signals confidence in ADBE's growth prospects, consistent with what Michael Burry sees in the stock.

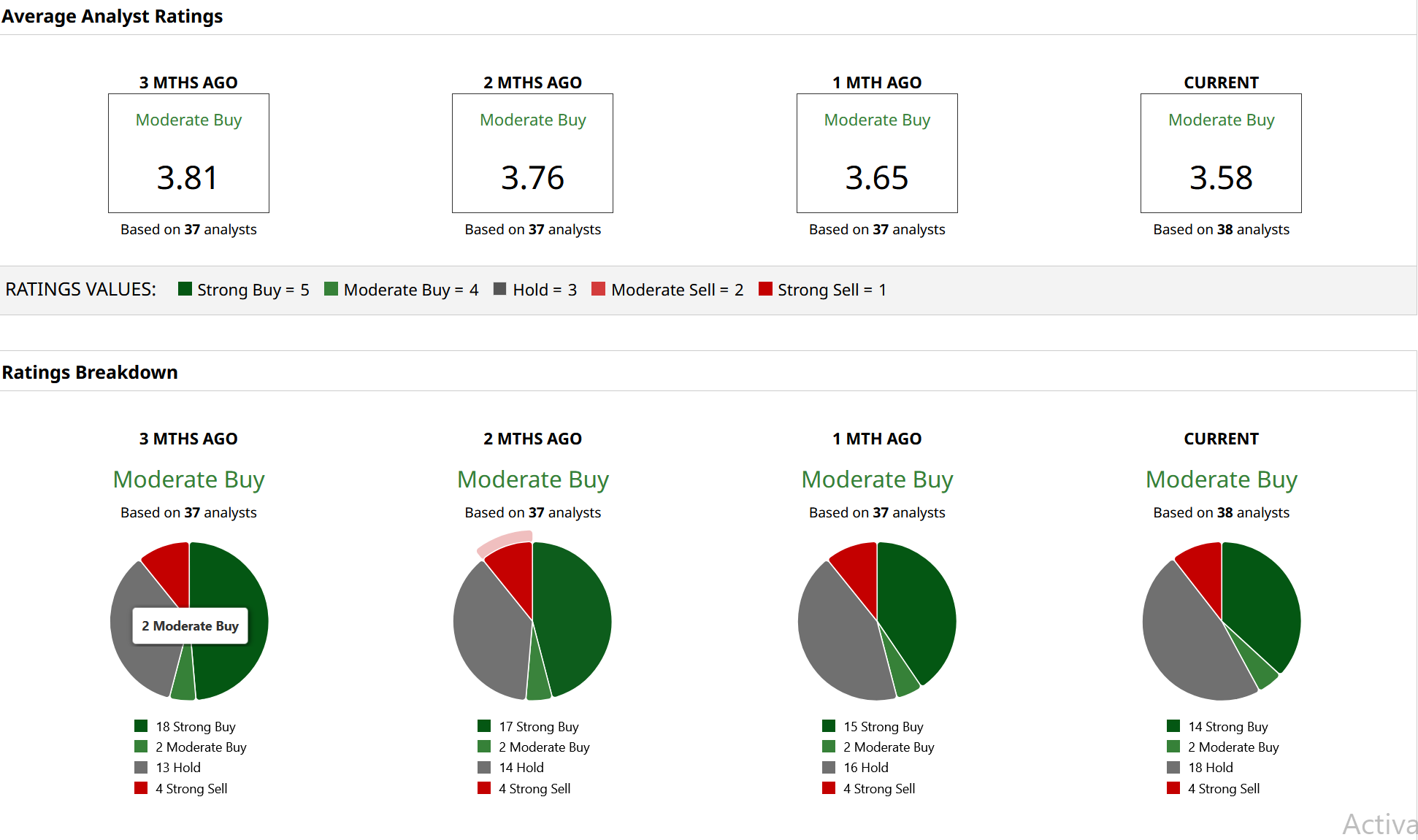

ADBE stock carries a consensus “Moderate Buy” rating based on 38 Wall Street analysts with coverage. Adobe has a mean price target of $323.83, reflecting 35% potential upside from the current levels.

www.barchart.com

www.barchart.com Michael Burry Stock #3: PayPal (PYPL)

PayPal (PYPL) runs a technology platform that allows businesses and customers around the world to receive and make digital payments. The company offers payment solutions under the PayPal, Hyperwallet, Venmo, Xoom, Honey, Braintree, and Paidy names. PayPal was founded in 1998 and is based in San Jose, California.

PYPL stock has lost almost 24% over the last 12 months, despite being up roughly 14% from its March lows. The short-term surge is a far cry from the past glory of PYPL stock, when shares used to trade as high as $300.

www.barchart.com

www.barchart.com The company reported its Q4 2025 earnings on Feb. 3, and the earnings call provided some interesting insights. Analysts probed about the execution speed and strategy, and management maintained a defensive tone, refusing to give exact targets that it intends to achieve. When asked about the 2026 outlook, management only said it expects the changes to start gaining traction throughout the year. Management also refused to reiterate the 2027 guidance it gave on last year’s Investor Day, sticking to a one-year outlook.

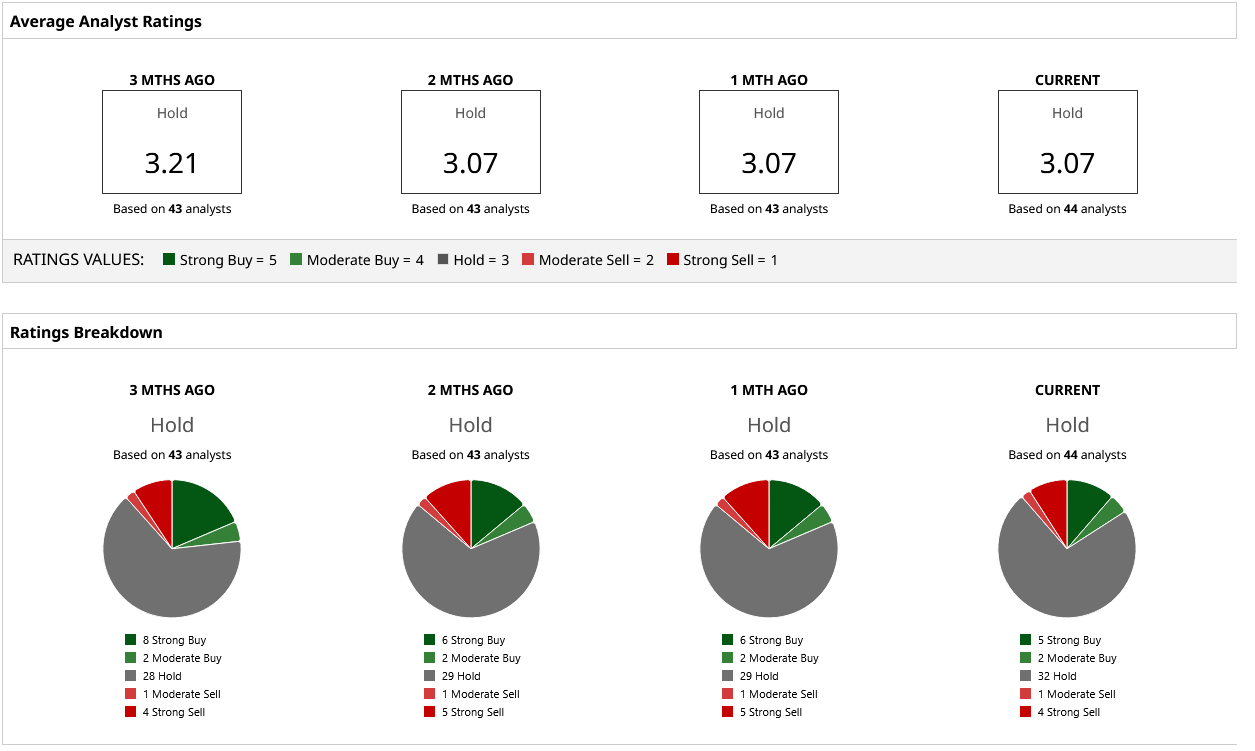

On April 24, Truist raised its target price on PYPL stock from $39 to $45 — still well below the current share price — and also maintained a “Sell” rating. In contrast, Cantor Fitzgerald recently raised its price target for PayPal from $42 to $54. The mean target price is $51.26, which is quite close to where the stock currently trades.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Michael Burry Disagrees With the AI Narrative, Buys Microsoft Stock and 2 Unexpected Names Domino's Pizza Stock Drop May Be Overdone, Based on Its Strong FCF Margins A $7.5 Billion Reason to Buy Applied Digital Stock Here Is Alphabet Stock a Buy, Sell, or Hold Ahead of Q1 Earnings?