Chevron Corporation CVX is slated to release first-quarter 2026 results on May 1, before market open.

The Zacks Consensus Estimate for revenues is pegged at $47.4 billion, implying only a modest decrease of 0.5% from the year-ago quarter. The consensus earnings mark of 92 cents per share has remained unchanged over the past seven days, suggesting a 57.8% decline from the year-ago reported number.

For full-year 2026, the Zacks Consensus Estimate for CVX’s revenues is pegged at $214 billion, implying an improvement of 13.2% year over year. The consensus mark for 2026 earnings per share stands at $13.55, indicating a surge of 85.9%.

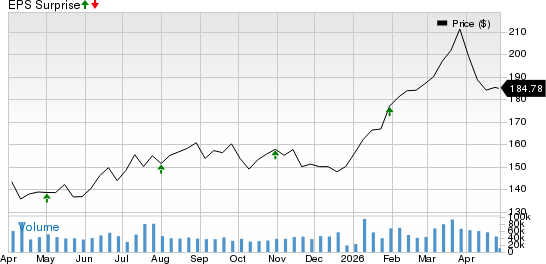

CVX's Earnings Surprise History

In the last reported quarter, the company delivered an earnings surprise of 5.6%. Chevron’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 5.6%.

Chevron Corporation Price and EPS Surprise

Chevron Corporation price-eps-surprise | Chevron Corporation Quote

Q1 Earnings Whispers for Chevron

The proven Zacks model does not conclusively show that Chevron is likely to beat estimates in the first quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of beating estimates. But that’s not the case here.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Earnings ESP: CVX has an Earnings ESP of 0.00%. This is because the Most Accurate Estimate and the Zacks Consensus Estimate are pegged at 92 cents per share each.

Zacks Rank: Chevron currently carries a Zacks Rank #1, which increases the predictive power of ESP. However, the company’s 0.00% ESP makes surprise prediction difficult this earnings season.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping CVX’s Upcoming Q1 Results

Chevron’s ongoing cost restructuring is quietly strengthening its earnings base. The company has already delivered $1.5 billion in structural cost savings in 2025, with a clear roadmap to reach $3-$4 billion by the end of 2026, driven largely by efficiency improvements and technology integration. These savings are not one-off — they are embedded into operations, lowering unit costs and lifting margins. Combined with a leaner operating model and improved supply-chain execution, this creates a stronger free cash flow profile, even in a volatile price environment. This is likely to have had a positive effect on Chevron’s first-quarter earnings and cash flows.

But on a somewhat bearish note, Chevron’s first-quarter performance is likely to have been weighed down by lower volumes and downstream pressures. According to the Zacks Consensus Estimate, production is expected to fall to 3,860 thousand oil-equivalent barrels per day (MBOE/d) from more than 4,000 MBOE/d in fourth-quarter 2025, mainly due to downtime at Tengiz and weaker output in Israel and the Partitioned Zone.

At the same time, downstream earnings face added strain from turnarounds, downtime ($275–$325 million impact) and a legal charge of $350-$400 million. These combined factors could temporarily compress overall earnings despite stronger upstream pricing. Consequently, the Zacks Consensus Estimate for the first-quarter downstream segment is currently pegged at a loss of $1.3 billion. In the year-ago period, Chevron had reported a profit of $325 million.

While near-term volumes dip, Chevron’s longer-term trajectory remains intact. Management continues to guide for 7-10% production growth in 2026, supported by ramp-ups in high-margin assets like the Permian, Guyana and the Gulf of America. Major developments, including Tengiz expansion and offshore projects, are expected to add scale progressively through 2026. This growth, paired with higher commodity price sensitivity ($1.6-$2.2 billion upstream uplift in first-quarter 2026), positions the company to expand earnings beyond the current quarter. Consequently, the Zacks Consensus Estimate for CVX’s first-quarter upstream income is pegged at $3.7 billion, implying a 21.2% improvement from the profit achieved in the fourth quarter of 2025.

Updates From Chevron’s Global Peers: ExxonMobil and Shell

Rival ExxonMobil XOM signaled that its first-quarter 2026 earnings may decline despite stronger oil and gas prices driven by Iran war-related supply disruptions. ExxonMobil expects upstream earnings gains from higher prices, but large negative timing effects from hedging — estimated at several billion dollars — will weigh on overall profits. ExxonMobil also faces a 6% drop in production due to the Middle East disruptions. Downstream performance is expected to be significantly impacted by delayed cargo deliveries. Despite these challenges, ExxonMobil indicated that these temporary effects should unwind, with profitability likely improving in the upcoming quarters.

Meanwhile, European oil major Shell plc SHEL has outlined a mixed Q1’26 outlook, as weaker gas production and geopolitical disruptions weigh on performance. However, Shell expects strong oil trading and marketing gains to offset some of this pressure. Shell continues to face challenges in Qatar, impacting output and liquidity, but LNG volumes remain stable. Despite rising debt, Shell maintains a manageable balance sheet, and its diversified operations and trading strength help it navigate volatility and support overall earnings stability.

CVX Price Performance & Stock Valuation

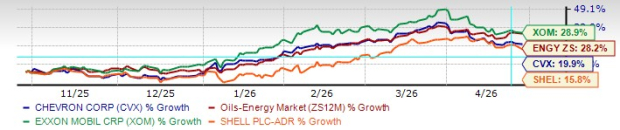

Shares of Chevron have gone up 19.9% in the past six-month period compared with the broader Zacks Energy sector’s growth of more than 28%. Shares of ExxonMobil have gained 28.9%, while the Shell stock has gone up 15.8%.

6-Month Price Performance

From a valuation perspective — in terms of forward price-to-earnings ratio — Chevron is trading at a premium compared to the industry average. The stock is also trading above its five-year mean of 11.86.

How Should You Play CVX Pre-Q1 Earnings?

Chevron is well-positioned heading into its first-quarter results, benefiting from a sharp rise in oil and gas prices driven by Middle East supply disruptions. With minimal exposure to the region, the company stands to capitalize on higher commodity prices while avoiding the operational setbacks impacting several peers. Management expects a significant sequential boost in upstream earnings, supported by strong pricing trends.

Although production is set to dip modestly due to temporary project-related downtime, long-term growth prospects remain intact with key developments in Guyana, the Permian and other regions. Ongoing cost reduction efforts are enhancing margins and cash flow. Coupled with strong shareholder returns and a resilient asset base, Chevron presents a compelling investment case ahead of its quarterly release.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chevron Corporation (CVX): Free Stock Analysis Report

Exxon Mobil Corporation (XOM): Free Stock Analysis Report

Shell PLC Unsponsored ADR (SHEL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).