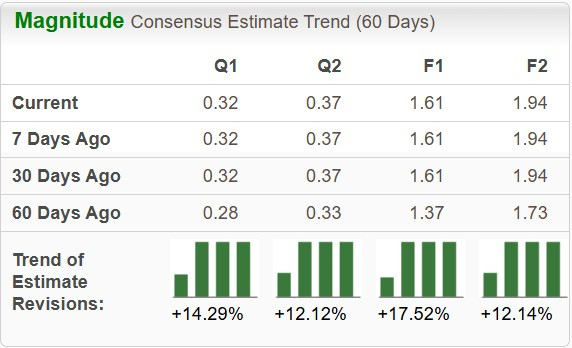

BrightSpring Health Services, Inc. BTSG is set to report first-quarter 2026 earnings on May 1, before the market opens. The Zacks Consensus Estimate for sales and earnings is pegged at $3.34 billion and 32 cents per share, respectively.

Earnings per share (EPS) estimates for BTSG have remained stable at $1.61 for 2026 and at $1.94 for 2027 over the past 30 days.

Image Source: Zacks Investment Research

Earnings Surprise History

In the last reported quarter, BTSG delivered a negative earnings surprise of 2.94%. Its earnings beat estimates in three of the trailing four quarters and missed once, delivering an average surprise of 40.37%.

BrightSpring Health Services, Inc. Price and EPS Surprise

BrightSpring Health Services, Inc. price-eps-surprise | BrightSpring Health Services, Inc. Quote

What the Zacks Model Unveils for BTSG

Our proven model does not conclusively predict an earnings beat for BrightSpring this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. However, this is not the case here, as you will see below.

BTSG has an Earnings ESP of 0.00% and a Zacks Rank #1 at present. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Factors Likely to Drive BTSG's Q1 Performance

BrightSpring is expected to have delivered a solid first-quarter 2026 performance, supported by continued momentum across its Pharmacy Solutions and Provider Services segments, along with early contributions from recent acquisitions. Growth is likely to have been driven by strong prescription volumes, expanding specialty pharmacy capabilities and steady demand for home-based care services.

Revenue growth is expected to have remained robust, albeit at a moderate pace compared to the strong momentum seen in 2025. Adjusted EBITDA is likely to have outpaced revenue growth, aided by favorable product mix, operational efficiency initiatives and early benefits from procurement and technology-driven cost optimization. However, margin expansion may have been slower as the company continues to invest in growth initiatives, salesforce expansion, AI deployment and integration of acquired assets.

A key area of focus will be the recent divestiture of the Community Living business. The use of sale proceeds to reduce first-lien term loan debt is likely to have supported improved financial flexibility and lower leverage, which could be a positive for long-term earnings quality. While the transaction is expected to streamline operations and sharpen focus on core healthcare services, investors will potentially look for clarity on how the new portfolio mix impacts near-term growth and profitability during the first quarter earnings call.

BTSG’s Segmental Performance Outlook

The Pharmacy Solutions segment is expected to have remained the primary growth engine in the first quarter. Strong performance is likely to have been driven by expansion in specialty and infusion services, supported by new limited distribution drug (LDD) wins, increased adoption of existing therapies and growth in fee-for-service business.

Specialty and infusion volumes are expected to have benefited from robust demand for complex therapies and continued commercial execution. Generic drug utilization and favorable pricing dynamics are likely to have supported margin expansion in the segment.

However, revenue growth may have been partially offset by headwinds from brand to generic conversions and lingering impacts from the company’s decision to exit uneconomic or bankrupt customers in the home and community pharmacy business.

The Provider Services segment is expected to have delivered steady growth, supported by continued demand for home-based care and rehabilitation services. Home health, which represents the largest portion of this segment, is likely to have benefited from strong patient volumes, expanding partnerships and de novo growth initiatives.

The integration of Amedisys and LHC assets is expected to have contributed modestly to revenue growth in the quarter, though profitability impact may have remained limited in the near term due to integration costs and system alignment efforts. Over time, these assets are expected to enhance geographic reach and enable cross-service synergies, particularly in hospice and home health.

Rehab services are likely to have maintained solid momentum, driven by increased patient volumes and expansion into new care settings, while personal care services are expected to have delivered stable growth.

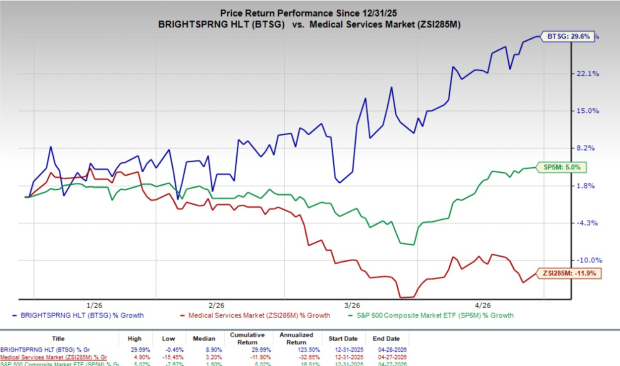

BrightSpring's Price Performance

Shares of BrightSpring have climbed 29.6% in the year-to-date period against the industry’s 11.9% decline. The S&P 500 Index has increased 5% in the same timeframe.

Image Source: Zacks Investment Research

Conclusion

BrightSpring is expected to exit its first-quarter with solid operational momentum, supported by strong growth in specialty pharmacy and home-based care. While portfolio optimization and acquisitions position the company well for long-term expansion, near-term execution risks around integration, margin trajectory and revenue headwinds remain. Given the balanced risk-reward profile and expected moderation in growth, a hold stance appears prudent ahead of the earnings release.

Stocks Worth a Look

Here are some medical product stocks worth considering as these have the right combination of elements to post an earnings beat this reporting cycle.

Fresenius Medical Care AG & Co. FMS has an Earnings ESP of +3.39% and a Zacks Rank #3 at present. The company is set to release first-quarter 2026 results on May 5. You can see the complete list of today’s Zacks #1 Rank stocks here.

FMS’ earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 9.67%. The Zacks Consensus Estimate for FMS’ first-quarter EPS indicates an improvement of 34.1% from the year-ago reported figure.

Intuitive Surgical ISRG has an Earnings ESP of +0.06% and a Zacks Rank of 2 at present. The company released its first-quarter 2026 results on April 21.

ISRG’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 16.82%. The Zacks Consensus Estimate for ISRG’s second-quarter EPS implies an improvement of 13.2% from the year-ago reported figure.

Hims & Hers Health HIMS has an Earnings ESP of +150.94% and a Zacks Rank of 3 at present. The company is slated to release first-quarter 2026 results on May 11.

HIMS’ earnings surpassed estimates in two of the trailing four quarters and missed in the other two, the average surprise being 69.45%. The Zacks Consensus Estimate for HIMS’ first-quarter EPS calls for a decline of 70% from the year-ago reported figure.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Fresenius Medical Care AG & Co. KGaA (FMS): Free Stock Analysis Report

Hims & Hers Health, Inc. (HIMS): Free Stock Analysis Report

BrightSpring Health Services, Inc. (BTSG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).