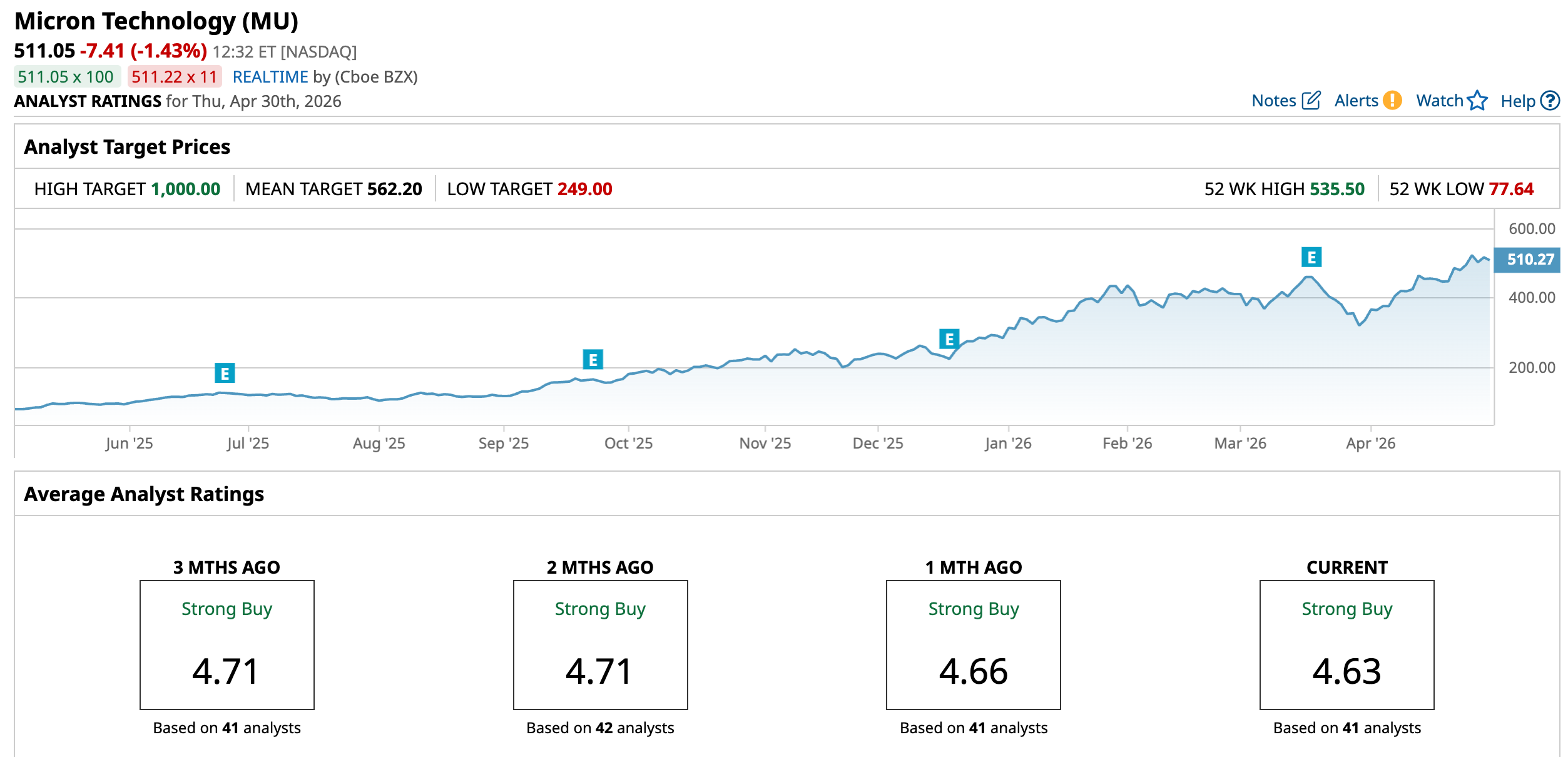

Micron Technology (MU) is rapidly emerging as one of the most talked-about plays on the artificial-intelligence (AI) infrastructure boom, with DA Davidson issuing the most bullish call on Wall Street with a “Buy” rating and a Street-high $1,000 price target.

The firm’s thesis hinges on a structural shift in the memory industry, where AI-driven demand for high-bandwidth memory and data center capacity is breaking the traditional cycle that has long defined the sector.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

According to the analyst, a powerful feedback loop between compute deployment and memory consumption is driving a “structurally higher ceiling” for both pricing and demand, supported by long-term supply agreements and tightening industry capacity.

With MU shares already up substantially over the past year and still trading at relatively modest valuation multiples, the call underscores a growing view that this might just be the beginning of a multi-year AI-led supercycle that could materially re-rate memory stocks.

About Micron Technology Stock

Micron Technology is a semiconductor company that designs, develops, manufactures and sells memory and storage products globally, including DRAM, NAND flash memory, HBM, solid-state drives (SSDs) and other memory modules. Headquartered in Boise, Idaho, Micron operates multiple business units serving cloud/data-center, mobile and client, automotive/embedded, and enterprise segments worldwide. Micron’s market cap stands at $584.7 billion, putting it among the largest and most valuable players in the global semiconductor industry.

Shares of Micron Technology have delivered exceptional price performance, firmly establishing the stock as one of the top beneficiaries of the AI-driven semiconductor rally. Over the past 52 weeks, MU has surged 565.5%, driven by tight memory supply, accelerating demand for high-bandwidth memory, and a sharp recovery in pricing across DRAM and NAND markets.

This momentum has extended into 2026, with the stock posting strong year-to-date (YTD) gains of 81.9%, supported by robust analyst upgrades and sustained investor enthusiasm around AI infrastructure spending. The rally culminated in a fresh 52-week high on April 27, when shares hit $531.36. Investors are increasingly pricing Micron as a structural AI winner rather than a traditional memory stock.

www.barchart.com

www.barchart.com In spite of the momentum, the stock still seems to be trading at a discount compared to industry peers at 8.74 times forward earnings.

Better-than-Expected Q2 Performance

Micron Technology reported its fiscal second quarter 2026 (ended Feb. 26, 2026) results on March 18, delivering one of the strongest quarters in its history, driven by unprecedented demand for AI-related memory products.

The company posted revenue of $23.86 billion, representing a massive year-over-year (YOY) increase of 196.3%. This surge reflects a sharp recovery in DRAM and NAND pricing alongside explosive demand for HBM used in AI data centers.

Profitability expanded even more dramatically. Micron reported adjusted EPS of $12.20, up roughly 682.1% YOY from about $1.56 in fiscal Q2 2025 and exceeding expectations.

At the segment level, the Cloud Memory Business Unit generated $7.8 billion in revenue, representing an increase of roughly 163% YOY, while gross margins improved to 74% from 55%.

The Core Data Center Business Unit delivered one of the strongest growth trajectories, with revenue rising to $5.7 billion from $1.8 billion, with margins also expanding meaningfully as gross margin improved to 74% from 47%.

In the Mobile and Client Business Unit, revenue reached $7.7 billion, marking a sharp 244.9% YOY increase. This segment’s gross margin rose dramatically to 79% from just 15%.

The Automotive and Embedded Business Unit also posted strong growth, with revenue climbing to $2.7 billion from $1 billion.

Management further issued exceptionally strong guidance for fiscal Q3 2026, signaling continued momentum. The company expects revenue of around $33.5 billion (plus or minus $750 million) and EPS of $19.15 (plus or minus $0.40).

Also, the consensus EPS estimate of $57.72 for fiscal 2026 reflects an increase of 651.6%, while the EPS estimate of $98.13 for fiscal 2027 indicates a 70% rise YOY.

What Do Analysts Expect for Micron Stock?

In addition to DA Davidson, many other analysts are turning increasingly bullish on Micron.

Recently, TD Cowen raised its price target on Micron to $660 and maintained a “Buy” rating, citing strong AI-driven demand and long-term margin visibility.

And Melius Research initiated Micron with a “Buy” and $700 target, citing sustained AI-driven demand and durable pricing across memory markets.

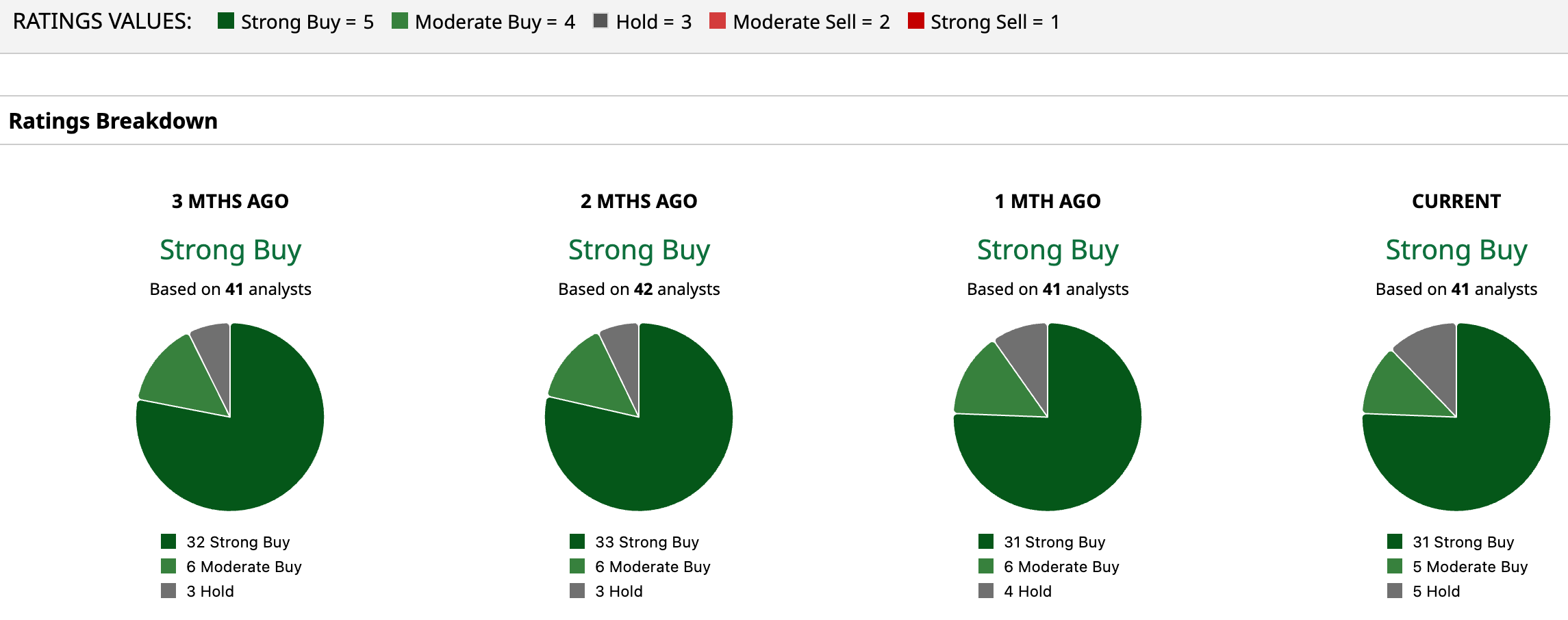

Overall, MU has a consensus “Strong Buy” rating. Of the 41 analysts covering the stock, 31 advise a “Strong Buy,” five suggest a “Moderate Buy,” and five analysts are on the sidelines, giving it a “Hold” rating.

While the average analyst price target of $562.20 suggests an upside of 10%, DA Davidson’s Street-high target price of $1,000 suggests that the stock could rally as much as 95.7%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Should You Buy Intel Stock in Q2? According to This Analyst, It's Critical for the 'American Way of Life' Up Over 17% in the Past 5 Days, Should You Keep Buying Sandisk Stock in May 2026? Micron Stock to $1,000? Surging Memory Demand Could Take MU to New Highs, Says DA Davidson Dozens of Experts Built This Simple Stock Screener for Traders & Investors. It Was Me.