Spectrum Brands Holdings, Inc. SPB is expected to register a year-over-year decline in the top line when it reports second-quarter fiscal 2026 results on May 7, 2026, before the opening bell. The Zacks Consensus Estimate for SPB’s revenues is pegged at $672.8 million, indicating a drop of 0.43% from the year-ago quarter.

The consensus estimate for Spectrum Brands’ earnings per share (EPS) is pegged at $1.04 per share, indicating growth of 52.9% from the figure in the year-ago quarter. The consensus mark for EPS has been stable in the past 30 days.

In the last reported quarter, the company delivered an earnings surprise of 81.8%. SPB has recorded an earnings surprise of 67.6% in the trailing four quarters, on average.

Spectrum Brands Holdings Inc. Price, Consensus and EPS Surprise

Spectrum Brands Holdings Inc. price-consensus-eps-surprise-chart | Spectrum Brands Holdings Inc. Quote

Factors Likely to Influence SPB's Q1 Results

Spectrum Brands’ second-quarter fiscal 2026 results are expected to reflect a challenging year-over-year comparison, primarily due to continued softness in consumer demand, especially within the Home & Personal Care (HPC) segment. Management has indicated that macroeconomic pressures and tariff-related pricing actions are still weighing on volumes, particularly in North America. While pricing initiatives have helped offset cost pressures, demand elasticity and reduced product offerings aimed at protecting profitability are likely to have constrained top-line growth in the quarter.

Another key factor shaping second-quarter performance is the ongoing weakness in global consumer sentiment for discretionary categories such as home appliances and personal care. The company expects these categories to remain under pressure, with only gradual normalization in demand trends. Additionally, inventory adjustments by retailers following weaker holiday sales may continue to impact replenishment orders, further limiting near-term sales recovery in HPC.

In contrast, the Global Pet Care segment is likely to have remained a relative bright spot in the second quarter. The business has already returned to growth in the first quarter, supported by strong brand performance, innovation and market share gains in companion animal categories. This momentum is expected to have continued into the second quarter, aided by improving POS trends and ongoing investments in brand-building and product innovation.

The Home & Garden segment, however, is expected to exhibit a more back-half-weighted recovery profile, which could limit second-quarter upside. Retailers are anticipated to have remained disciplined in inventory build, unlike the prior year’s early stocking patterns. Moreover, the seasonal nature of this business means that meaningful sales acceleration is likely to occur later in the quarter or into the second half, depending on weather conditions and consumer activity.

What Does the Zacks Model Predict for SPB Stock?

Our proven model does not conclusively predict an earnings beat for Snap-on this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that is not the case here.

SPB has an Earnings ESP of -5.31% and a Zacks Rank of 2 at present. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Valuation Picture

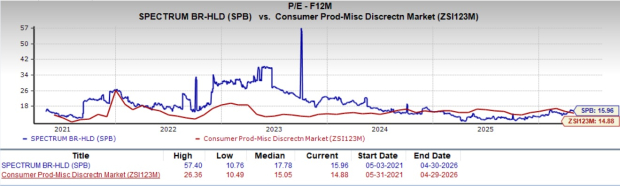

From a valuation perspective, Spectrum Brands has a forward 12-month price-to-earnings ratio of 15.96X, which is higher than the Zacks Consumer Products – Discretionary industry’s average of 14.88X. The stock has a five-year high of 57.40X.

Image Source: Zacks Investment Research

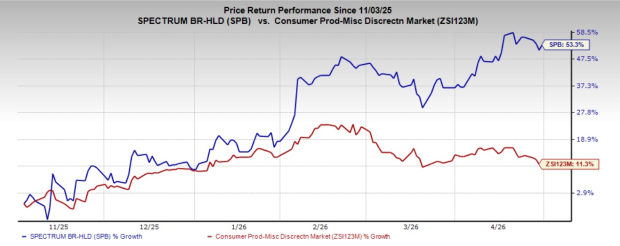

The recent market movements show that SPB’s shares have gained 53.3% in the past six months compared with the industry's 11.3% growth.

Image Source: Zacks Investment Research

Stocks With the Favorable Combination

Here are some companies, which, according to our model, have the right combination of elements to post an earnings beat:

AMC Entertainment Holdings, Inc. AMC currently has an Earnings ESP of +5.82% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for first-quarter 2026 revenues is pegged at $997.7 million, indicating 15.7% growth from the figure reported in the year-ago quarter. The consensus estimate for AMC Entertainment’s earnings is pegged at a loss of 32 cents per share, implying an 44.8% improvement from the year-ago quarter’s actual. AMC delivered an earnings surprise of 10% in the last quarter.

Marriott International Inc. MAR currently has an Earnings ESP of +0.44% and a Zacks Rank of 3. MAR is likely to register a top-line increase when it reports first-quarter 2026 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $6.59 billion, indicating a 5.3% rise from the figure reported in the prior-year quarter.

The consensus estimate for Marriott International’s earnings is pegged at $2.60 per share, implying 12.1% growth from the year-ago quarter’s actual. MAR delivered a negative earnings surprise of 2.3% in the last quarter.

Cintas Corporation CTAS currently has an Earnings ESP of +1.14% and a Zacks Rank of 3. CTAS is likely to register a top-line increase when it reports fourth-quarter fiscal 2026 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $2.88 billion, indicating a 7.8% rise from the figure reported in the prior-year quarter.

The consensus estimate for Cintas’s earnings is pegged at $1.24 per share, implying 13.8% growth from the year-ago quarter’s actual. CTAS delivered an earnings surprise of 0.8% in the fiscal third quarter.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Marriott International, Inc. (MAR): Free Stock Analysis Report

Cintas Corporation (CTAS): Free Stock Analysis Report

Spectrum Brands Holdings Inc. (SPB): Free Stock Analysis Report

AMC Entertainment Holdings, Inc. (AMC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).