Coinbase Global COIN is set to report first-quarter 2026 results on May 7, after market close.

The Zacks Consensus Estimate for COIN’s first-quarter revenues is pegged at $1.5 billion, indicating a 26.1% decrease from the year-ago reported figure.

The consensus estimate for earnings is pegged at 36 cents per share. The Zacks Consensus Estimate for COIN’s first-quarter earnings has moved down 16.3% in the past 30 days. The estimate suggests a year-over-year decrease of 81.4%.

Image Source: Zacks Investment Research

COIN’s Decent Earnings Surprise History

COIN’s earnings beat the Zacks Consensus Estimates in two of the trailing four quarters and missed in the other two, the average surprise being negative 18.38%.

What the Zacks Model Unveils for COIN

Our proven model does not conclusively predict an earnings beat for Coinbase this time around. This is because a stock needs to have the right combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold), which increases the odds of an earnings beat. This is not the case, as you can see below.

Earnings ESP: Coinbase’s Earnings ESP is -18.69%. This is because the Most Accurate Estimate of 29 cents per share is pegged lower than the Zacks Consensus Estimate of 36 cents. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Coinbase Global, Inc. Price and EPS Surprise

Coinbase Global, Inc. price-eps-surprise | Coinbase Global, Inc. Quote

Zacks Rank: Coinbase currently has a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Likely to Shape COIN’s Q1 Results

A weaker crypto market and declining prices likely dampened trading activity in the first quarter of 2026. The Zacks Consensus Estimate places trading volume at 233 million, implying a 40.7% drop compared to the same quarter last year. Both institutional and retail trading activity are expected to have declined during the period.

However, Coinbase’s expansion into international markets, growing derivatives and spot trading, and stronger integration of USD Coin (USDC) within the crypto ecosystem likely supported its key revenue streams—trading fees and stablecoins.

Despite these positives, lower trading volumes and prices are expected to have pressured transaction activity. The Zacks Consensus Estimate for transaction revenue stands at $837 million, suggesting a 33.7% year-over-year decline. Transaction expenses are projected to remain in the low-to-mid teens as a percentage of net revenues.

Meanwhile, subscription and services revenues are likely to have benefited from blockchain rewards, stablecoin income, and growth in Coinbase One subscriptions. The company anticipates this segment to generate between $550 million and $630 million in the first quarter, supported by rising USDC market capitalization and a larger subscriber base. The consensus estimate is $617 million.

On the cost side, increased digital marketing efforts are expected to have driven sales and marketing expenses, projected between $215 million and $315 million. Additionally, investments in technology to enhance efficiency, along with disciplined cost management, are likely to have supported margin improvement.

Coinbase expects technology and development, as well as general and administrative expenses, to range between $925 million and $975 million, primarily due to increased headcount.

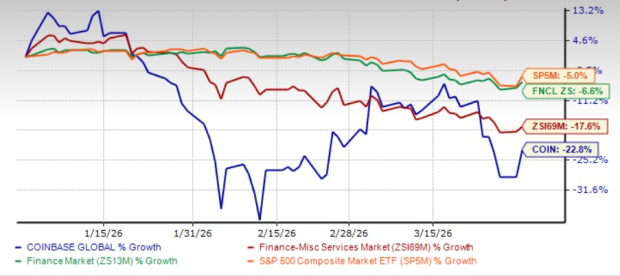

COIN’s Price Performance & Valuation

The stock underperformed the industry, sector and the S&P 500 in the first quarter of 2026.

Image Source: Zacks Investment Research

The stock is trading at a price-to-earnings ratio of 28.35, higher than the industry’s 13.35.

Image Source: Zacks Investment Research

Shares of Robinhood Markets HOOD and Interactive Brokers Group, Inc. IBKR, two other crypto-oriented stocks, are also trading at multiples higher than the industry average.

Investment Thesis

In 2026, Coinbase aims to focus on real-world asset (RWA) perpetuals, specialized exchanges, advanced trading platforms, next-generation DeFi infrastructure, and deeper integration of AI and robotics to enhance its ecosystem. The company has received conditional approval from the Office of the Comptroller of the Currency (OCC) to establish a national trust bank, signaling efforts to bridge traditional finance and the crypto sector.

Coinbase is also accelerating international expansion by listing more cryptocurrencies and tokenized equities, while promoting assets aligned with a pro-crypto ecosystem. The rollout of stock and ETF trading for U.S. users has broadened its addressable market beyond digital assets and strengthened its position against diversified fintech brokers.

Financially, the company remains stable, backed by strong liquidity and ongoing debt reduction, improving its debt-to-capital ratio. However, its performance remains closely tied to crypto price volatility, with declines in major assets like Bitcoin and Ethereum potentially impacting earnings, valuations, cash flow, and liquidity.

To support growth, Coinbase is increasing investments in technology, marketing, and administrative functions. At the same time, pricing pressures have led to impairment charges, while restructuring initiatives continue to add to operating expenses.

What Should Investors Do Now With COIN Stock?

Coinbase’s focus on growing the broader crypto ecosystem and enhancing the trading experience through ongoing innovation is expected to drive strong growth. This crypto leader is leaving no stone unturned to be a one-stop destination for trading of any digital assets or providing financial services related to crypto or digital assets.

Given a premium valuation, lowered volatility, lowered asset prices, and below-average return on equity, it is wise to stay cautious on the stock.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Interactive Brokers Group, Inc. (IBKR): Free Stock Analysis Report

Coinbase Global, Inc. (COIN): Free Stock Analysis Report

Robinhood Markets, Inc. (HOOD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).