Meta Platforms (META) just delivered its strongest sales growth since 2021, with Q1 2026 revenue up 33% year-over-year (YOY) to $56.3 billion, but the stock still fell 8% after management raised its 2026 CapEx spending plans to a steep $125 billion–$145 billion to build out new AI infrastructure and “Superintelligence Labs.”

At the same time, China blocked Meta’s planned $2 billion purchase of Manus, and the company is dealing with legal and regulatory battles in the U.S., from a child‑safety fight in New Mexico to new Senate efforts to limit how chatbots interact with minors.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Even with all that hanging over the stock, Cathie Wood is stepping in, not stepping away. Her ARK funds bought a total of 47,201 Meta shares across several ETFs, including ARK Innovation ETF (ARKK), spending roughly $28–31 million at the lower prices.

When a high‑profile growth investor is willing to look past the spending headlines and the legal noise, it naturally leads to one key question about what happens next with Meta’s share price. Let’s dive in.

META’s Numbers Still Back Cathie Wood’s Dip‑Buying Bet

Meta is a Menlo Park–based technology company that runs Facebook, Instagram, WhatsApp, Messenger, Threads, and other online services used by more than 3.5 billion people every day. The business is one of the largest digital advertising networks in the world and makes most of its money by selling targeted ads across these apps.

Its stock is down 7.52% so far this year but still up 2.25% over the past 12 months.

www.barchart.com

www.barchart.com The company has a forward price‑to‑earnings multiple of 20.53 times versus a sector median of 13.49 times, and the price‑to‑earnings‑to‑growth ratio stands at 0.96 times compared with a sector median of 1.22 times, so investors are paying more than the average stock in the group but not more than its growth suggests is reasonable.

META carries an equity value of about $1.54 trillion and pays a forward annual dividend of $2.10 per share, which works out to a 0.34% yield.

Meta’s latest earnings report, released on April 23, showed revenue of $56.31 billion for the first quarter of 2026, up 33% from the same period a year earlier, or 29% on a constant‑currency basis. The company reported diluted earnings per share of $7.31, ahead of the $6.71 Wall Street estimate. That worked out to an 8.94% positive surprise and shows META is still growing profits even as it spends more to support AI and other long‑term projects.

META reported total costs and expenses of $33.44 billion, up 35% YOY as it expanded its data centers and other infrastructure. This increase pushed capital expenditures, including payments on finance leases, to $19.84 billion for the quarter.

The company still returned $1.35 billion through dividends and dividend equivalents. It finished March 31 with $81.18 billion in cash, cash equivalents, and marketable securities, which helped support the operating cash flow of $32.23 billion and the free cash flow of $12.39 billion. These numbers show META has the financial strength to keep investing heavily in its future while still sending some cash back to shareholders.

Meta's Aggressive AI CapEx Push

To see why Cathie Wood is comfortable buying META’s dip, it helps to look at what the company is actually spending on, not just the size of the bill. Meta has lifted its 2026 capital‑expenditure (CapEx) outlook to a range of $125 billion to $145 billion, up from an earlier forecast of $115 billion to $135 billion.

A big chunk of that is going into raw computing power. META and AMD (AMD) signed a multi‑year deal to roll out up to 6 gigawatts of AMD Instinct GPUs across Meta’s global footprint, with shipments for the first 1 gigawatt set to start in the second half of 2026. That arrangement, built on AMD’s Helios rack‑scale design, gives META more than one major chip source and secures high‑end hardware at a large scale.

Cloud capacity is another pillar. CoreWeave (CRWV) has an expanded agreement to supply AI cloud services to META through December 2032, a deal valued at about $21 billion. Nebius then agreed to provide up to $27 billion of dedicated AI capacity using Nvidia’s next‑generation Vera Rubin platform, with deliveries beginning in early 2027. These long‑dated contracts are meant to keep META supplied with the computing muscle it needs for years.

Chip design is also moving in‑house. Broadcom (AVGO) has a three‑year co‑design agreement with META that runs through 2029 and covers several generations of META’s MTIA accelerators and networking chips, starting with at least 1 gigawatt of AI computing capacity. Mark Zuckerberg has framed this work as building the “massive computing foundation” needed for new AI features.

Even the power supply is part of the plan. META teamed up with Overview Energy to secure up to 1 gigawatt of space‑based solar power. The aim is simple. It wants round‑the‑clock energy from orbit so that the electricity grid does not become a ceiling on how far it can scale its data centers.

What the Pros Are Signaling on META

Wall Street might complain about META’s spending plans, but the numbers analysts are working with look pretty steady. The next earnings release is penciled in for July 29, 2026, and the current quarter (June 2026) has an average earnings estimate of $7.18 per share, only a touch above the $7.14 delivered a year earlier, which works out to about 0.56% expected growth.

That tone shows up clearly in the research calls. Guggenheim’s Michael Morris stuck with a “Buy rating” on META and kept his $850 price target in place, even after management raised its AI investment outlook. His stance implies he still believes the extra spending will lift earnings power over time, enough to offset the hit to margins and free cash flow.

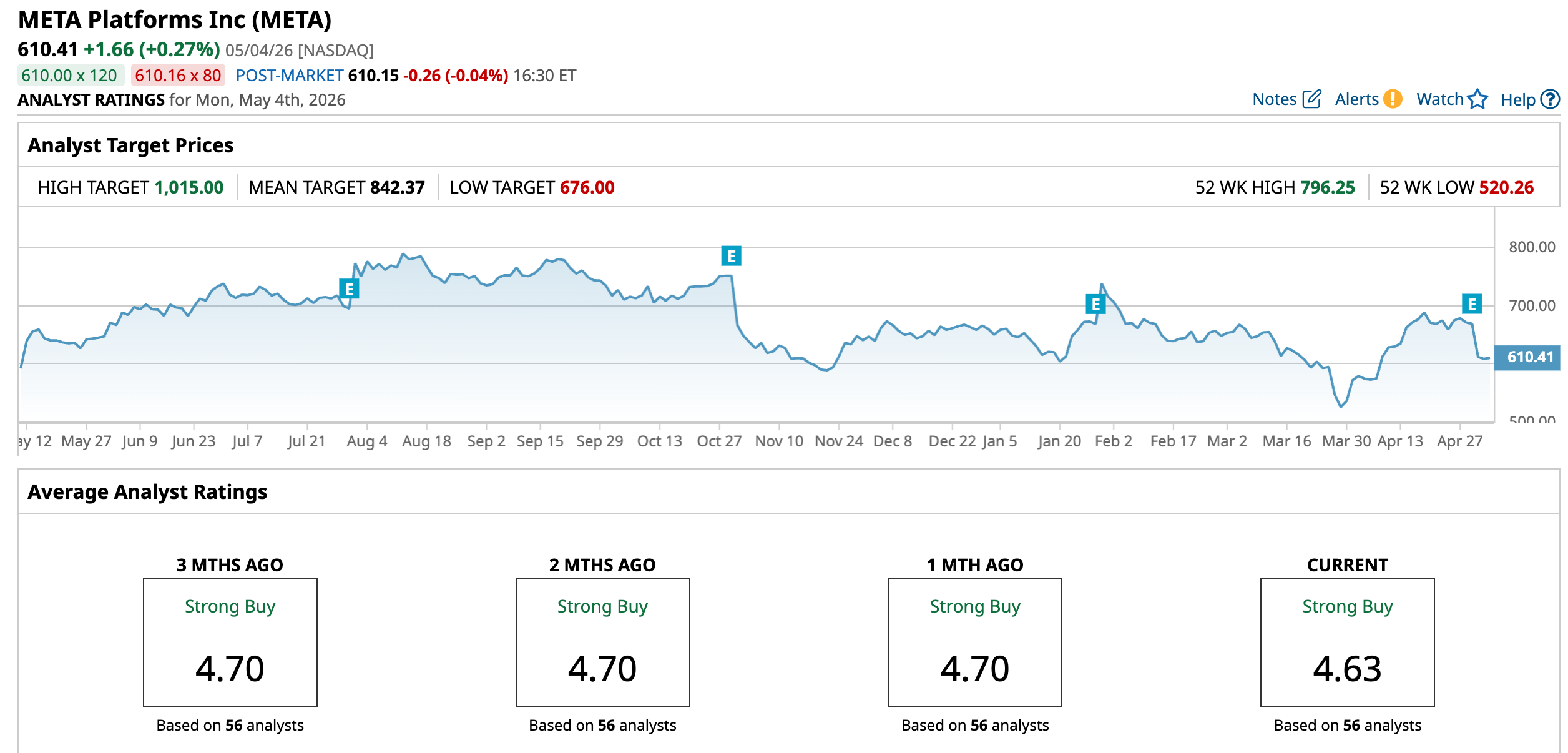

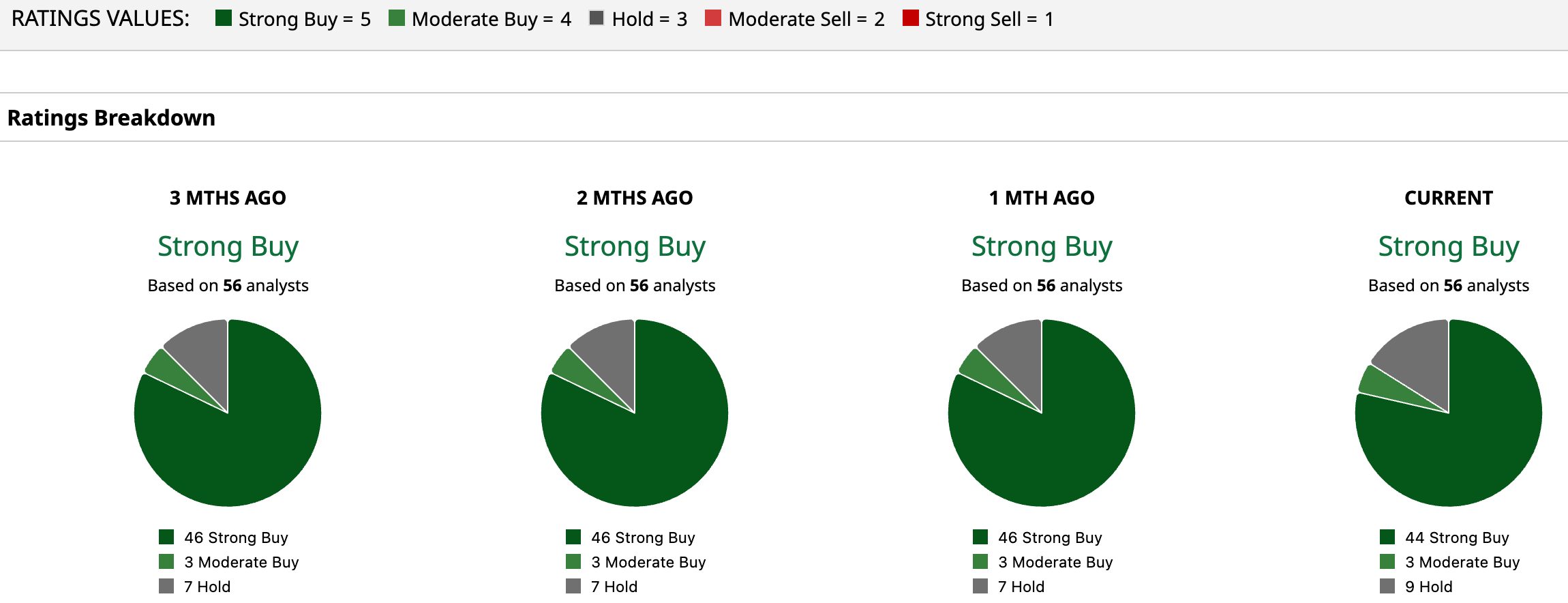

Broader coverage points in the same direction. A group of 56 analysts tracking the stock has reached a consensus Strong Buy rating. Their average price target stands around $842.37, which suggests an upside of roughly 38% if the stock simply grows into the Street’s base case.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

Meta’s recent drop looks more like investors stepping back over the size of its spending plans than giving up on the company. The business is still bringing in strong cash, signing long-term infrastructure deals, and getting plenty of support from analysts, which helps explain why Cathie Wood has been buying the pullback. In the near term, the stock could stay uneven, but the direction still looks more likely up than down if Meta keeps delivering solid results and keeps its spending under control.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Cathie Wood Is Shrugging Off CapEx Fears and Buying the Dip in Meta Platforms Stock Dear Western Digital Stock Fans, Mark Your Calendars for June 5 CRM Stock Jumps as Salesforce Makes Clear It’s an AI Agent Company Now More AI Is Coming to iOS 27. Why That Could Make Apple Stock a Buy Here.