Wall Street was rattled after e-commerce giant Amazon (AMZN) made a bold move into the logistics arena on May 4, unveiling Amazon Supply Chain Services (ASCS), a sweeping platform that opens the company’s massive freight, fulfillment, distribution, and shipping network to outside businesses. The announcement immediately sent shockwaves through the U.S. logistics industry and sparked a sharp selloff in logistics stocks, with United Parcel Service (UPS) tumbling nearly 10.5% on the same day.

The new service allows companies of all sizes across industries, including retail, healthcare, and manufacturing, to tap into Amazon’s sprawling supply-chain infrastructure spanning ocean freight, trucking, rail, air cargo, warehousing, fulfillment, and parcel delivery. The move signals Amazon’s ambitions to evolve far beyond e-commerce and establish itself as a dominant force in the U.S. logistics market, a space long dominated by UPS and other traditional freight giants.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

The announcement carried even more weight after Amazon revealed that major corporations, including Procter & Gamble (PG), 3M (MMM), and American Eagle Outfitters (AEO), have already signed on to use the service. Still, not everyone on Wall Street believes Amazon’s latest push will completely reshape the industry overnight. William Blair analyst Dylan Carden, for instance, questioned whether ASCS will prove as disruptive to the freight business as investors currently fear, even as transportation stocks reel from the announcement.

And more importantly, despite the market’s knee-jerk reaction, UPS’ grip on the logistics industry remains deeply entrenched. Combined with its shareholder-friendly approach and a dividend yield approaching 7%, the shipping giant may still have plenty of appeal for long-term investors even as Amazon ramps up the competitive pressure.

About UPS Stock

Founded in 1907, United Parcel Service is one of the world’s largest logistics companies, generating $88.7 billion in revenue in 2025 while providing integrated transportation and supply-chain solutions across more than 200 countries and territories. The company operates with a strategy centered on customer service, workforce leadership, and innovation, supported by a global employee base of roughly 460,000 people.

UPS has also continued focusing on environmental initiatives and community support efforts across the markets where it operates. In recent months, United Parcel Service has ramped up efforts to reinvent its business, shedding lower-margin operations, streamlining its delivery network, and expanding further into higher-margin opportunities like healthcare logistics.

This strategic pivot has prompted analysts to reassess the company’s long-term outlook. At the heart of the transformation is UPS’ deliberate shift away from lower-profit Amazon-related volume toward more lucrative segments, a move designed to strengthen margins and improve the quality of revenue, even if it results in slower package-volume growth overall.

Currently valued at roughly $83.27 billion by market capitalization, United Parcel Service has struggled to keep pace with the broader market as margin pressures and intensifying competition continue to weigh on investor sentiment. The stock has gained 5.83% over the past year, sharply lagging the broader S&P 500 Index ($SPX), which surged 30.8% during the same period. The underperformance has continued into 2026, with UPS shares gaining marginally 0.09% year-to-date (YTD), while the broader market has advanced 7.13%.

www.barchart.com

www.barchart.com Even though United Parcel Service stock has been under pressure, the company has remained firmly committed to returning cash to shareholders. UPS paid its latest quarterly dividend of $1.64 per share on March 5, reinforcing its reputation as a shareholder-friendly company. On an annualized basis, the logistics giant now offers a hefty dividend payout of $6.56 per share, translating to a highly attractive yield of about 6.69%. Notably, UPS is distributing a substantial portion of its profits back to investors, with its dividend payout ratio standing at 97.28%.

UPS’ Q1 Earnings Snapshot

United Parcel Service released its first-quarter 2026 results on April 28, calling the period a “critical transition” phase as the company continues executing its large-scale business overhaul. Revenue came in at $21.2 billion, down 1.6% from the prior year but still modestly ahead of Wall Street expectations of $20.96 billion. However, profitability remained under pressure, with adjusted operating profit declining 25% year-over-year (YOY) to $1.32 billion as operating margins compressed to 6.2%, down from 8.2% a year ago.

Adjusted earnings per share landed at $1.07, marking a 28.2% decline from last year but still topping analyst estimates of $1.03. Digging deeper, the company’s U.S. Domestic business absorbed the bulk of the pressure during the quarter. Revenue in the segment slipped 2.3% to $14.1 billion, largely due to an 8% decline in average daily package volume. Notably, UPS said roughly two-thirds of that drop stemmed from its intentional reduction in Amazon-related shipping volume as the company pivots toward higher-quality, more profitable business.

Last year, the company launched the most extensive U.S. network reconfiguration in its history, targeting a 50% reduction in the volume it delivers for Amazon by June 2026. Even so, UPS managed to partially offset the volume decline through stronger pricing and improved revenue mix, driving a 6.5% increase in revenue per piece. Meanwhile, other areas of the business delivered encouraging signs of strength.

International revenue rose 3.8% to $4.5 billion, helped by a sharp 10.7% increase in revenue per piece despite softer global shipping demand. Supply Chain Solutions also stood out, with adjusted operating profit more than doubling to $206 million. Looking ahead, UPS reaffirmed its full-year 2026 outlook, projecting consolidated revenue of roughly $89.7 billion alongside an adjusted operating margin target of 9.6%.

UPS also reaffirmed its commitment to both long-term investment and shareholder returns, maintaining plans for roughly $3 billion in capital expenditures while expecting to return approximately $5.4 billion to investors through dividend payments this year, supported by a free cash flow forecast of about $5.5 billion.

Why Wall Street May Be Overreacting to Amazon’s Logistics Push

While Amazon’s foray into logistics might hurt UPS to some extent, William Blair analyst Dylan Carden isn’t convinced the freight industry is headed for a major shake-up just yet. Carden pointed out that Amazon has spent the past 15 years making headline-grabbing moves into industries such as grocery and pharmacy, announcements that often triggered steep short-term declines in related stocks.

However, many of those reactions ultimately proved to be overly dramatic, as Amazon’s expansion efforts in several new categories delivered mixed results rather than outright disruption. Furthermore, the analyst questioned how ASCS materially differs from “Supply Chain by Amazon,” the company’s end-to-end logistics framework introduced back in 2023, and said it remains unclear what the latest announcement truly changes for the freight industry.

According to Carden, the earlier Supply Chain by Amazon platform never appeared to become “a runaway success,” noting that relatively few large organizations signed on to use the service. “We live in a weird market,” Carden remarked, highlighting what he sees as investors’ tendency to react aggressively to Amazon-related headlines. In fact, Carden suggested the ASCS launch may partly represent a strategic “rebranding” effort, one made more credible by high-profile clients such as Procter & Gamble.

With William Blair’s cautious view in mind, the steep selloff in UPS stock could ultimately prove to be more panic-driven than a reflection of any immediate threat to UPS’ long-standing dominance in logistics.

How Are Analysts Viewing UPS Stock?

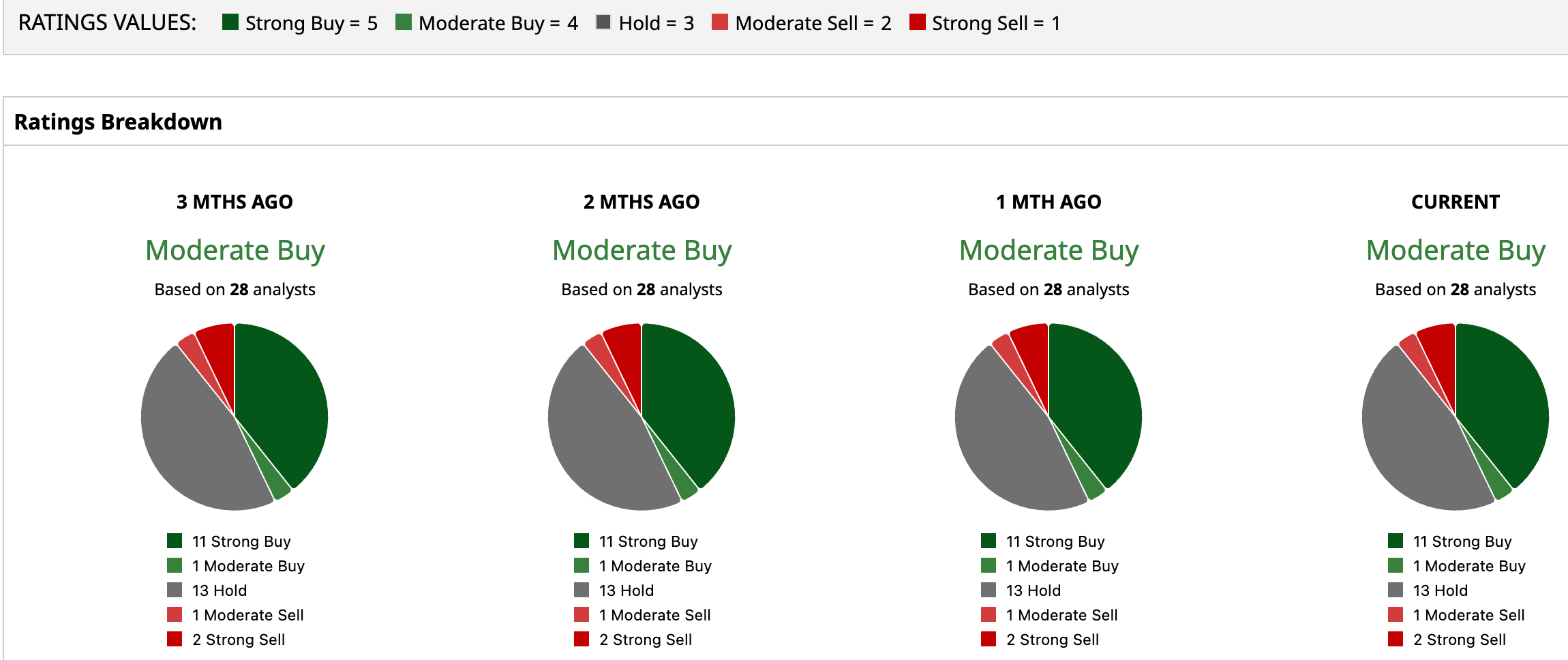

Despite the recent sharp pullback in shares, Wall Street hasn’t lost faith in UPS. The stock still carries a consensus “Moderate Buy” rating, reflecting a cautiously optimistic outlook from analysts. Among the 28 analysts covering UPS, 11 rate it a “Strong Buy,” one recommends “Moderate Buy,” while 13 remain on the sidelines with “Hold” ratings. On the bearish side, one analyst issued a “Moderate Sell,” and two maintain “Strong Sell” calls.

Importantly, analysts still see meaningful upside ahead. The average price target of $115.58 suggests the stock could climb roughly 15.75% from current levels, while the Street-high target of $135 implies a potential rally of as much as 35.2%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Ignore the Amazon Trucking Noise and Buy UPS Stock for Its High Yield Near 7% The Amazon Most Investors Knew No Longer Exists Universal Logistics Stock Plunged on Amazon’s Trucking News. Its 3.4% Dividend Could Make the Dip Worth Buying. This Small-Cap Healthcare Stock Is Up 300% in a Year and Is Quickly Gaining a Following