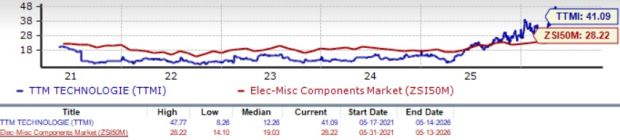

TTM Technologies TTMI shares are overvalued, as suggested by a Value Score of D. The stock is trading at a premium with a forward 12-month Price/Earnings (P/E) of 41.09X compared with the Zacks Electronics - Miscellaneous Components industry’s 28.22 and Zacks Computer and Technology sector's 25.87X. TTMI is valued above its peers, Amphenol Corporation APH, Sanmina Corporation SANM and TE Connectivity TEL, which trade at 25.45X, 19.63X and 17.04X, respectively.

The premium is supported by accelerating data center and networking revenue, record backlog levels and expanding manufacturing capacity tied to rising AI compute demand, though a meaningful portion of the near-term growth narrative already appears priced in.

TTMI’s P/E F12M Ratio

Image Source: Zacks Investment Research

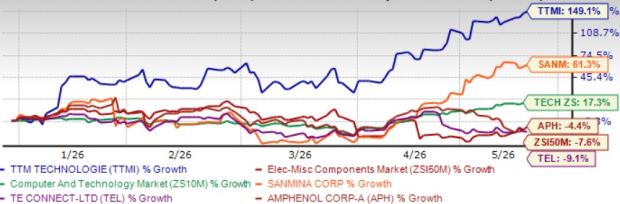

On a year-to-date basis, TTMI shares have surged 149.1%, outpacing the Zacks sub-industry's 7.6% decline and the broader sector's 17.3% advance. Among peers, Sanmina Corporation has gained 61.3% while TE Connectivity and Amphenol Corporation have declined 9.1% and 4.4%, respectively, year to date.

TTMI's outperformance reflects growing market recognition of its differentiated positioning in high-complexity printed circuit boards serving AI data center buildouts and defense modernization programs.

TTMI’s YTD Performance

Image Source: Zacks Investment Research

So how should investors approach TTMI at this stage? Let's take a closer look.

TTMI Benefits From AI Buildout and Defense Modernization

TTM Technologies is well-positioned within two of the most structurally supported demand cycles in electronics manufacturing, namely AI data center infrastructure and defense modernization. The company's advanced printed circuit boards, capable of reaching layer counts up to 140, are becoming central to next-generation AI system architectures as hyperscalers scale compute capacity. With 80% of revenues tied to these two verticals, TTMI's revenue mix is structurally aligned with where capital deployment is accelerating most visibly.

On the defense side, recent program bookings spanning advanced radar systems and a confirmed order tied to the Golden Dome initiative reflect deepening program alignment that extends well beyond near-term budget cycles. The commercial book-to-bill of 1.65 in the first quarter of 2026 indicates demand is running well ahead of current shipments, with the 90-day backlog expanding 52% year over year to $787 million, providing concrete near-term revenue support.

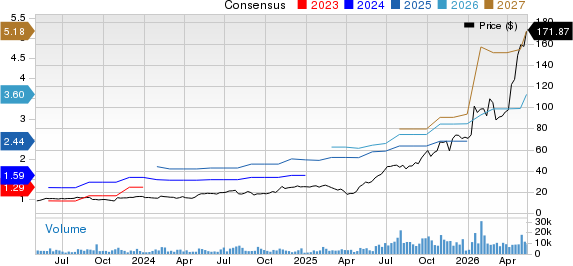

The Zacks Consensus Estimate for 2026 revenues is pegged at $3.83 billion, up 31.65% year over year. The consensus mark for EPS is pegged at $3.60 and has been revised 11.11% upward over the past 30 days, indicating 46.34% growth year over year, suggesting the earnings trajectory remains firmly positive as the company's stated goal to grow revenues 15% to 20% annually over the next three years and double earnings from 2025 to 2027 continues to track ahead of plan.

TTM Technologies, Inc. Price and Consensus

TTM Technologies, Inc. price-consensus-chart | TTM Technologies, Inc. Quote

Expanding Capacity Expected to Drive TTMI Margins

TTM Technologies is in the midst of an aggressive capacity expansion cycle that is beginning to translate into tangible margin improvement. The Penang facility in Malaysia, the company's anchor for data center and networking production in Asia, has seen yields improve toward 70% to 80%, approaching a breakeven threshold expected to reduce the current drag on consolidated margins through the second half of 2026.

The Eau Claire facility in Wisconsin follows the same anchor customer model that drove Penang's ramp. With 750,000 square feet across three flexible modules serving both commercial and defense end markets, it has the potential to become a meaningful domestic revenue contributor as onshore manufacturing demand grows, though its margin impact is expected to be more visible in 2027 and beyond.

Capital expenditure guidance for 2026 has been raised to $300 to $320 million from $240 to $260 million, indicating accelerated equipment procurement ahead of anticipated demand. This investment is showing early returns, with operating margins expanding 230 basis points year over year to 12.8% in the first quarter of 2026, driven by higher volumes and a favorable mix shift toward higher complexity boards. As Penang moves toward breakeven and the broader capacity base scales, operating leverage on a higher revenue base is expected to drive further margin expansion through 2027.

TTMI's Cash Outflow Warrants Caution

With a free cash flow of negative $85 million recorded in the first quarter of 2026, reflecting capital expenditures of $107 million, cash consumption is expected to remain elevated through the near term as the global capacity build progresses. CapEx guidance has been raised to $300 to $320 million for 2026, and with the Penang facility yet to reach breakeven, further pressure on cash generation is anticipated before new facilities approach productive capacity.

Should demand moderate or facility ramps take longer than anticipated, incremental demand could be absorbed by established peers, Amphenol Corporation, Sanmina Corporation and TE Connectivity, potentially weighing on TTMI's ability to sustain its current growth trajectory.

Conclusion

TTM Technologies remains well-positioned within AI infrastructure and defense modernization, supported by a record backlog and a capacity expansion program aligned with durable demand tailwinds. However, elevated cash consumption, Penang's below-breakeven status and execution risks tied to accelerated CapEx limit near-term upside visibility following the stock's sharp year-to-date rally.

TTMI currently carries a Zacks Rank #3 (Hold) and a Growth Score of A, suggesting that existing investors may benefit from maintaining their positions, while new investors could benefit from waiting for a more favorable entry point. You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amphenol Corporation (APH): Free Stock Analysis Report

TE Connectivity Ltd. (TEL): Free Stock Analysis Report

TTM Technologies, Inc. (TTMI): Free Stock Analysis Report

Sanmina Corporation (SANM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).