Amazon (AMZN) stock hasn’t moved much so far in 2026. Much of the hesitation surrounding the stock stems from investor concerns about the company’s significant capital expenditures, particularly its aggressive spending on artificial intelligence (AI) infrastructure and data centers. Despite these concerns, however, Wall Street remains optimistic about AMZN stock.

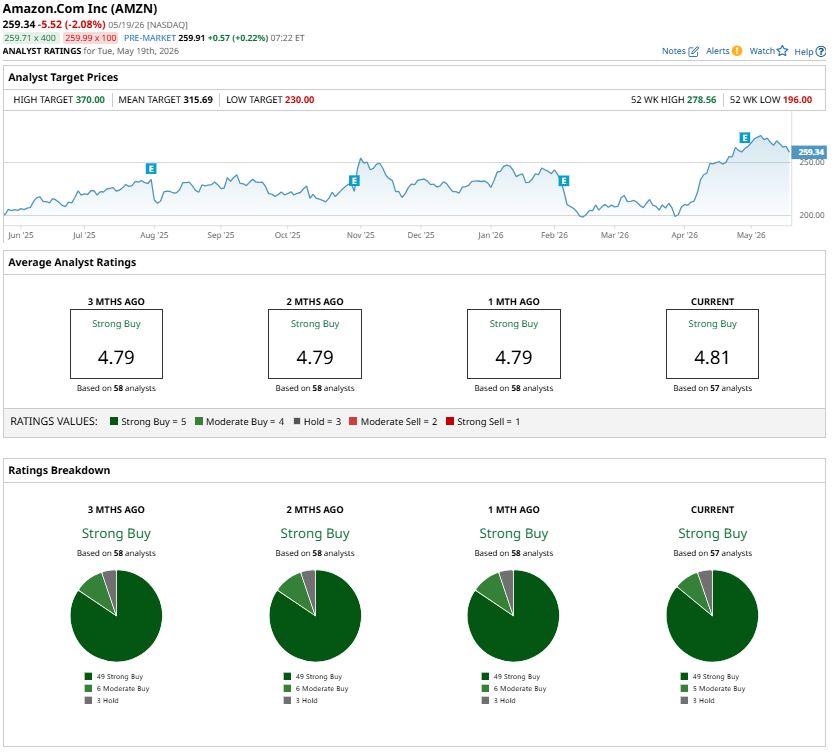

Analysts continue to maintain a “Strong Buy” consensus rating on Amazon. Furthermore, the highest price target for AMZN stock is $370, indicating roughly 40% potential upside from its recent May 20 closing price of $265.01. With businesses like its Amazon Web Services (AWS) cloud division, AI, and advertising firing on all cylinders, AMZN stock could surge higher.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com AWS Positions Amazon for Solid Growth

Amazon delivered a strong first quarter, led by accelerating growth in AWS. The cloud segment generated $37.6 billion in revenue, up 28% year-over-year (YOY). Moreover, the growth rate accelerated from 24% in the previous quarter.

Growth was driven by increasing demand for both traditional cloud infrastructure and AI services. More enterprises are shifting workloads to the cloud while expanding their use of AWS’s computing and storage capabilities.

At the same time, companies investing heavily in AI are turning to AWS to power and scale those applications. Management highlighted that higher AI spending is also boosting demand for AWS’s core cloud services, creating a positive cycle of growth across the platform.

Amazon noted that many AI deployments are still in their early stages. As customers move these projects into full-scale production, AWS is expected to see even stronger demand. The company added that its AI-related revenue is currently growing at a triple-digit YOY rate, reflecting rapid adoption of its AI infrastructure and tools.

AWS’s long-term outlook is also supported by its growing backlog of contracted business. At the end of the quarter, AWS reported a backlog of $364 billion, providing strong visibility into future revenue. Management said this figure does not yet include the recently announced $100 billion-plus deal with Anthropic.

Further, Amazon is aggressively expanding its infrastructure capacity, particularly for AI and data centers. The company plans to double its power capacity by 2027, strengthening AWS’s ability to benefit from the continued growth of cloud computing and AI. Overall, the strength of this pipeline and the expansion of capacity suggest that the growth trajectory of AWS will continue to accelerate in the coming years.

Amazon’s AI Chip Business Is Becoming a Monster Growth Engine

Amazon’s AI chip business is rapidly turning into one of the company’s most important growth drivers. In Q1 alone, Amazon’s custom AI silicon division grew nearly 40% quarter-over-quarter. The business is now generating revenue at an annualized run rate of more than $20 billion, with triple-digit YOY growth.

Notably, OpenAI and Anthropic have signed massive multiyear commitments with Amazon. Meanwhile, Amazon’s Trainium chips are witnessing solid demand, with the company securing more than $225 billion in revenue commitments.

Its Trainium2 chips are already largely sold out. Demand for the newer Trainium3 platform, which only began shipping this year, is so strong that capacity is almost fully subscribed. Moreover, customers are already reserving Trainium4 capacity despite the chips still being roughly 18 months away from release.

This solid demand suggests Amazon's AI chip business is turning into a significant growth driver for the company.

Advertising Continues to Print High-Margin Revenue

Amazon’s advertising revenue was $17.2 billion in the first quarter, up 22% YOY. The advertising segment remains a high-margin engine that continues to diversify Amazon's total revenue mix.

The business is evolving beyond traditional sponsored listings into a broader full-funnel advertising ecosystem powered by AI, streaming partnerships, and advanced commerce data. Amazon is also pushing deeper into conversational and agentic AI advertising formats. That move could unlock entirely new monetization opportunities over time.

Is AMZN Stock Heading to $370?

Amazon appears well-positioned to sustain its growth trajectory despite ongoing concerns about elevated AI and infrastructure spending. AWS continues to benefit from accelerating enterprise cloud adoption and surging AI demand, while the company’s rapidly expanding AI chip business is emerging as a powerful new revenue engine with massive customer commitments already secured.

At the same time, Amazon’s high-margin advertising segment continues to scale, diversifying revenue and supporting overall profitability.

With multiple growth drivers and Wall Street’s bullish outlook, AMZN stock has substantial room to run higher and hit the Street-high $370 price target over the next 12 months.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Astera Labs Just Got a Boost From Evercore ISI. What to Know. SoftBank Dumps Uber Stock, But Uber’s Growth Is Accelerating Why Wall Street Thinks Amazon Stock Can Rally 40% to $370 Tesla Stock Continues to Be Dramatically Overvalued Amid Company Struggles