Founded in 1928, Georgia-based Genuine Parts Company (GPC) operates as a global distributor of automotive and industrial replacement parts, serving customers across multiple regions through an extensive supply and service network. The company’s automotive business spans North America, Europe, and Australasia, while its industrial segment primarily focuses on North America and Australasia. With more than 10,800 locations across 17 countries and a workforce of over 65,000 employees, Genuine Parts has built a broad international presence in the replacement parts and industrial solutions market.

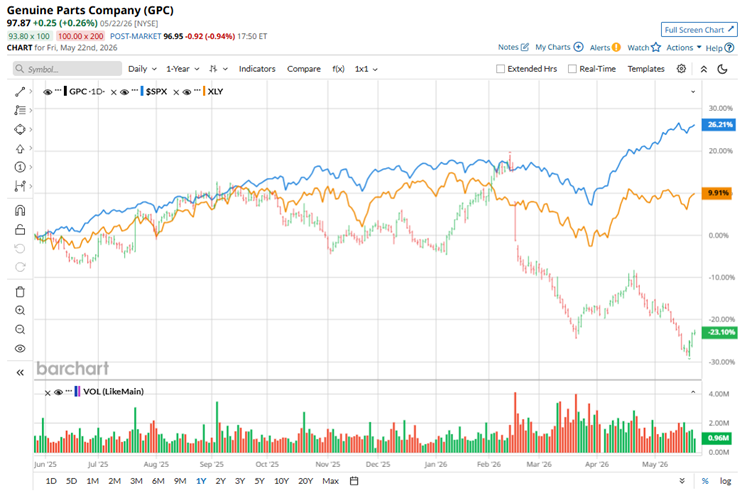

But despite its longstanding presence in the automotive and industrial parts market, Genuine Parts Company has struggled to keep investors on its side. The company, currently valued at a market capitalization of roughly $13.61 billion, has seen its shares tumble 22.9% over the past year and another 20.4% so far in 2026, reflecting growing pressure on the stock.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

That performance stands in sharp contrast to the broader S&P 500 Index ($SPX), which has rallied 28% over the past 12 months and gained another 9.2% year-to-date (YTD). The weakness becomes even more noticeable against sector peers. The State Street Consumer Discretionary Select Sector SPDR ETF (XLY) has climbed roughly 12.1% over the last year and is only marginally lower in 2026, underscoring how significantly Genuine Parts has lagged both the broader market and the consumer discretionary sector.

www.barchart.com

www.barchart.com Genuine Parts delivered a solid revenue beat for the first quarter of 2026 on Apr. 21, reporting quarterly sales of $6.26 billion. That marked a 6.8% year-over-year increase and came in ahead of Wall Street expectations of $6.17 billion. The growth was supported by a 2.4% increase in comparable store sales, contributions from strategic acquisitions, and a favorable 3.1% boost from foreign currency translation.

Despite the stronger top-line performance, profitability remained under pressure. GAAP net income slipped slightly to $189 million, or $1.37 per diluted share, compared to $1.40 per share in the year-ago quarter. Results were weighed down by upfront costs tied to the company’s global restructuring efforts and corporate separation planning ahead of its anticipated business split in early 2027.

On an adjusted basis, earnings came in at $1.77 per share, up modestly from $1.75 a year earlier, but still below Wall Street’s consensus estimate of $1.81. Even with the mixed earnings report, investors appeared encouraged by the company’s resilient sales growth, sending the stock modestly higher by the close of the Apr. 21 trading session.

Looking ahead, Wall Street expects Genuine Parts to post stronger profitability in fiscal 2026, with analysts forecasting earnings to rise 3.8% year over year to $7.65 per share. Even so, the company’s earnings track record has remained inconsistent. Genuine Parts has missed consensus EPS estimates in three of the past four quarters, managing to outperform expectations on only one occasion during that stretch.

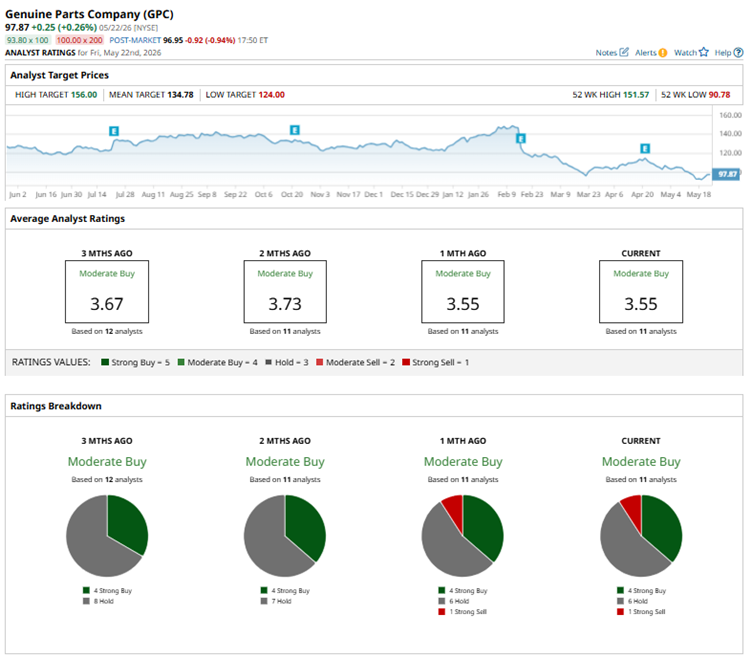

Wall Street remains cautiously optimistic on Genuine Parts, with the stock currently carrying a consensus “Moderate Buy” rating among 11 analysts. The breakdown includes four “Strong Buy” ratings, six “Holds,” and one “Strong Sell.” However, the current setup is slightly less bullish than it was two months ago, when the stock carried no sell ratings at all.

www.barchart.com

www.barchart.com In mid-April, UBS reiterated its “Neutral” rating on Genuine Parts and maintained a $135 price target, pointing to several challenges facing the company and the broader industry. The firm highlighted concerns that rising energy prices could weaken demand across the automotive parts market, while also noting uncertainty surrounding the next phase of Genuine Parts’ planned separation process, which has left investors looking for greater clarity on the company’s future direction.

Even so, Wall Street’s broader outlook suggests analysts still see meaningful recovery potential ahead. The average price target of $134.78 implies roughly 38% upside from current levels, while the Street-high target of $156 points to a potential rally of nearly 59.4%.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nvidia Had Another ‘Usual’ Quarter: How to Play NVDA Stock After Q1 Earnings Nvidia Hikes Its Dividend and Buybacks Based on Surging FCF - Is NVDA Too Cheap? Applied Digital Signed a Major Lease With a Hyperscaler for Its New Polaris Forge 3 Campus. What This Means for APLD Stock. Nvidia Just Raised Its Dividend by 2,400%. NVDA Stock Is Still a Bet on Growth, Not Income.