McDonald's Corporation MCD is navigating a difficult cost environment as inflationary pressure continues to weigh on franchisee margins across major markets. Higher beef prices, rising energy expenses and supply-chain disruptions are increasing restaurant-level costs at a time when the company is also trying to maintain its value positioning.

The pressure appears more pronounced in Europe, where beef inflation has remained elevated. At the same time, McDonald’s expects food and paper inflation to stay in the low to mid-single-digit range in the United States and in the mid-single digits across international operated markets during 2026. These cost pressures are limiting margin flexibility for franchisees, especially as consumer spending remains uneven.

McDonald’s strategy currently relies on balancing affordability with restaurant economics. Aggressive pricing actions may hurt traffic, particularly among lower-income consumers already affected by inflation and higher gas prices. As a result, the company continues leaning on meal deals, value platforms and promotional offerings to protect guest counts and market share.

However, maintaining value while input costs rise creates additional strain on franchisees. Beef-heavy menu categories are becoming more expensive to operate, making product mix increasingly important. This partly explains why McDonald’s continues to focus on chicken innovation, as the category is growing faster globally and carries a relatively better cost structure compared with beef.

The company is also using scale advantages, supplier relationships and hedging strategies to manage near-term inflation. These measures may help reduce volatility, but management expects broader cost pressures and supply-chain uncertainty to remain a risk into late 2026 and 2027.

For McDonald’s, sustaining franchisee margins may depend less on pricing and more on traffic growth, menu mix optimization and operational efficiency. With inflation still elevated, protecting franchisee economics could remain one of the company’s key challenges over the next several quarters.

MCD’s Stock Price Performance, Valuation & Estimates

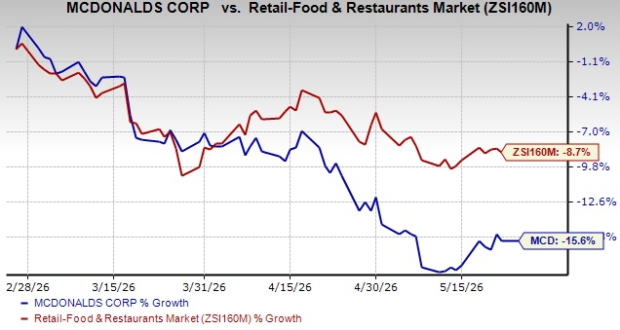

Shares of McDonald's have declined 15.6% in the past three months compared with the industry’s 8.7% fall. In the same time frame, other industry players like Chipotle Mexican Grill, Inc. CMG have declined 13.6%, while Sweetgreen, Inc. SG and Starbucks Corporation SBUX have gained 59.2% and 5.1%, respectively.

Image Source: Zacks Investment Research

From a valuation standpoint, MCD trades at a forward price-to-sales (P/S) multiple of 6.9, above the industry’s average of 3.34. Conversely, industry players, such as Starbucks, Sweetgreen and Chipotle, have P/S multiples of 2.98, 1.6 and 3.13, respectively.

MCD’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for MCD’s 2026 earnings per share has declined in the past 30 days.

EPS Trend of MCD Stock

Image Source: Zacks Investment Research

The company is likely to report strong earnings, with projections indicating a 6% rise in 2026. Conversely, industry players like Sweetgreen and Starbucks are likely to witness a rise of 107% and 12.7%, respectively, year over year, in 2026 earnings. Meanwhile, Chipotle’s 2026 earnings are likely to witness a fall of 3.4% year over year.

MCD's Zacks Rank

MCD stock has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Starbucks Corporation (SBUX): Free Stock Analysis Report

McDonald's Corporation (MCD): Free Stock Analysis Report

Chipotle Mexican Grill, Inc. (CMG): Free Stock Analysis Report

Sweetgreen, Inc. (SG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).