Shares of Palantir Technologies (PLTR) are down about 23% year-to-date, significantly underperforming the benchmark index, which has gained over 9% during the same period. Moreover, Palantir stock is down 34% from its 52-week high of $207.52.

The selloff comes after mounting concerns over valuation. For months, Palantir traded at a premium far above most software peers and even above mega-cap tech companies. At the same time, investors began reassessing the competitive landscape from artificial intelligence (AI) companies, putting pressure on software stocks, including Palantir.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

But despite the pullback, the company’s underlying business appears stronger than ever. Demand for Palantir’s Artificial Intelligence Platform (AIP) continues to accelerate as enterprises ramp up AI spending. The company is also expanding margins, winning more contracts, and increasing customer spending across its platform ecosystem.

Further, the recent correction has also cooled some of the valuation concerns that previously kept many investors on the sidelines.

So, after the steep decline, is this an opportunity to buy one of the fastest-growing enterprise AI software companies’ stock? Let’s take a closer look.

www.barchart.com

www.barchart.comPalantir’s Explosive Growth Strengthens the Bull Case

The momentum in Palantir’s business continued in 2026 with the company delivering a solid Q1 performance. Its top line surged 85% year-over-year and 16% sequentially to $1.63 billion, marking the 11th consecutive quarter of accelerating growth. The continued acceleration in growth rate signals that the demand for Palantir’s AI platform is expanding rapidly.

Palantir’s customer metrics were impressive. Total customer count climbed 31% year-over-year to 1,007, while spending from its largest clients continued to increase. Trailing 12-month revenue from Palantir’s top 20 customers rose 55% year-over-year to $108 million per customer.

The strongest momentum continues to come from the U.S., where Palantir’s business crossed into triple-digit growth for the first time. U.S. revenue jumped 104% year-over-year to $1.28 billion, driven by the accelerating adoption of its AI platform across both commercial enterprises and government agencies.

Its U.S. commercial business was particularly strong, growing 133% year-over-year. Meanwhile, its U.S. government business expanded 84% year-over-year, benefitting from continued execution across existing programs alongside new contract awards.

Underlying demand indicators continued to strengthen across the board. Total contract value bookings grew 135% year-over-year, while net dollar retention reached 150%, showing that current customers are rapidly expanding their use of Palantir’s platform and newer customers are increasing spending faster than before.

The company exited the quarter with $11.8 billion in total remaining deal value, up 98% year-over-year and 6% sequentially. Remaining performance obligations rose 134% year-over-year to $4.5 billion, providing strong visibility into future revenue growth.

Given the strength of the quarter, management raised its outlook for the remainder of 2026. Palantir now expects full-year revenue of about $7.66 billion, representing approximately 71% annual growth and a meaningful increase from prior guidance of roughly $7.19 billion issued last quarter.

The company also raised expectations for U.S. commercial revenue growth, adjusted operating income, and adjusted free cash flow, signaling growing confidence that demand trends remain exceptionally strong.

Is Palantir Stock a Buy?

Palantir has evolved into a profitable, cash-generating enterprise AI software platform with expanding relevance across both enterprise and government markets. Its accelerating revenue growth, surging customer spending, and expanding contract value indicate that Palantir is solidifying its position as a leading enterprise AI platform.

The company’s ability to achieve triple-digit growth in its U.S. business, maintain strong retention rates, upbeat guidance, and growing remaining deal value indicates solid revenue growth ahead.

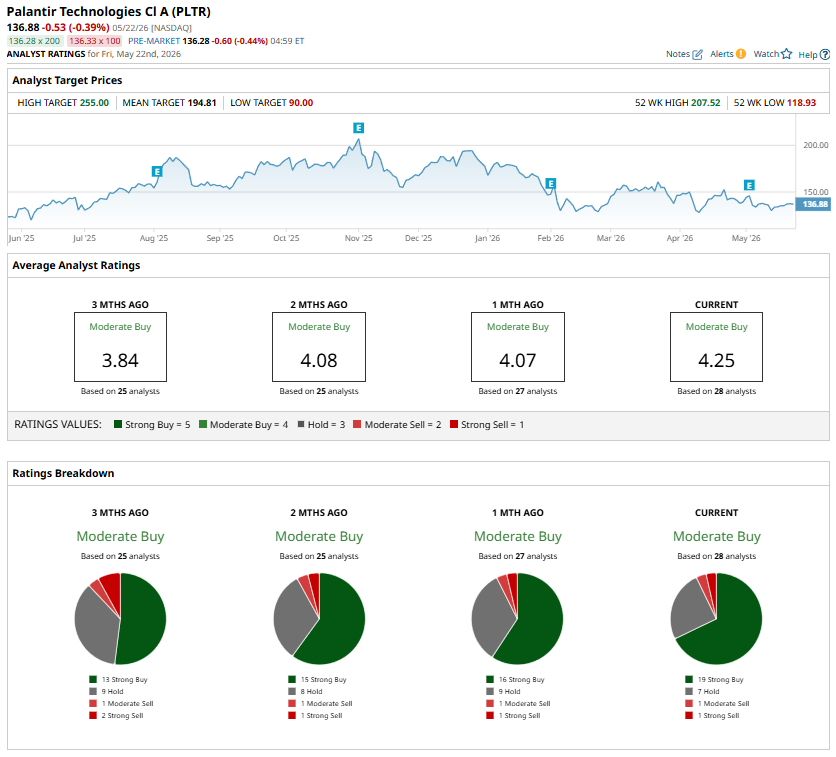

After the pullback, PLTR stock is trading at a price-to-sales ratio of 73.6x. Although the valuation remains expensive, the company’s rapid business growth helps justify the premium, making the stock appealing for growth-focused investors. Wall Street analysts currently rate PLTR a “Moderate Buy.”

www.barchart.com

www.barchart.com On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.