Artificial intelligence (AI) has been the predominant investing theme for the last couple of years. While chipmakers, particularly Nvidia (NVDA), and hyperscalers are the obvious and much sought-after AI plays, we also have ancillary plays like utilities.

Hyperscalers are doubling down on building AI infrastructure. While the upcoming data centers would need a load of chips, they would also require a lot of electricity. They have been signing massive power purchase agreements to ensure their power-guzzling data centers have sufficient energy. American Electric Power (AEP) is among the utility companies that are plays on the burgeoning AI power demand. And, the company pays a healthy dividend, with the current yield just under 3%. Let's analyze whether the stock would fit into portfolios of dividend investors.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

www.barchart.com

www.barchart.comAEP Has Paid Quarterly Dividends for Over a Century

To begin with, let’s look at American Electric's dividend policy. Like fellow utility companies, AEP is quite generous with dividends and has paid dividends since July 1910. Last year, it increased its quarterly dividend by $0.02 to $0.95. The annual dividend growth in the coming years should be in high single digits, which is in line with the earnings growth that the company is projecting.

AEP is among the largest electricity producers in the U.S., with a diverse generating capacity of 32,000 megawatts, and it boasts the largest transmission network, owning and operating nearly 90% of the 765 kV infrastructure in the country. It is present in 11 states and serves 5.6 million customers.

What Would Drive American Electric’s Growth?

Utilities are known for anemic growth, but the sprawling data centers are a generational opportunity for power companies in the U.S. During their Q1 2026 earnings call, American Electric said that it has contracted 63 gigawatts of additional load, with the number rising by 7 gigawatts since the previous update in February. Of these 63 gigawatts, 90% is from data centers, including from hyperscalers, while the remaining is mainly from industrial companies. The company expects its long-term annualized earnings growth to be over 9% after completion of these projects.

The growth would, however, need capital and a lot of it, actually. AEP raised its base capex plan between 2026 and 2030 to $78 billion, which is $6 billion higher than the previous forecast. The funds for the projected capex would come from a mix of internal accruals, along with debt and equity issuance. However, the company is committed to maintaining its investment grade credit ratings and targets a funds from operations (FFO) to debt multiple between 14%-15%. Apart from the base plan, the company has an additional $10 billion of projects that it could consider. These include the Piketon transmission project and the Wyoming fuel cell project, among others.

AEP Stock Forecast

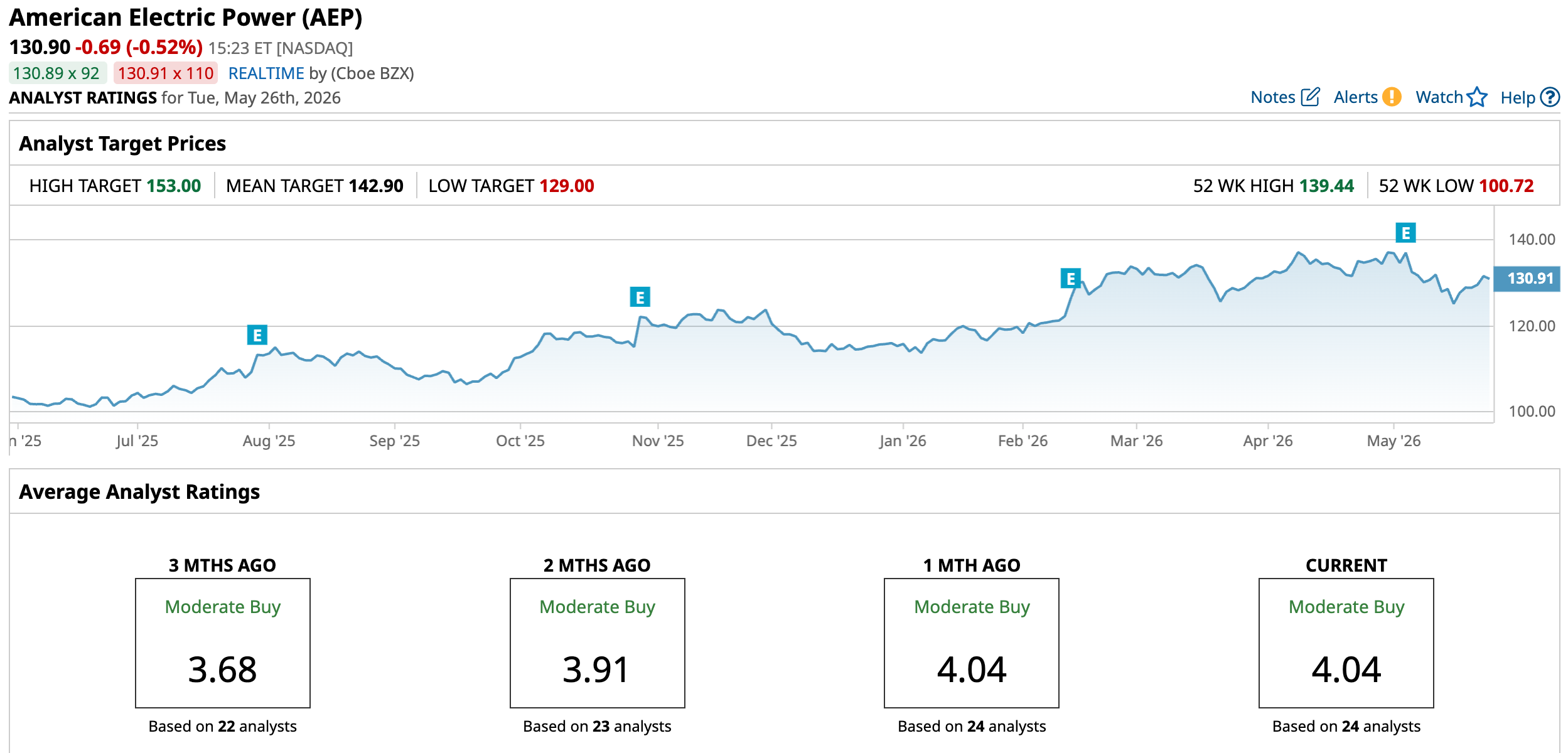

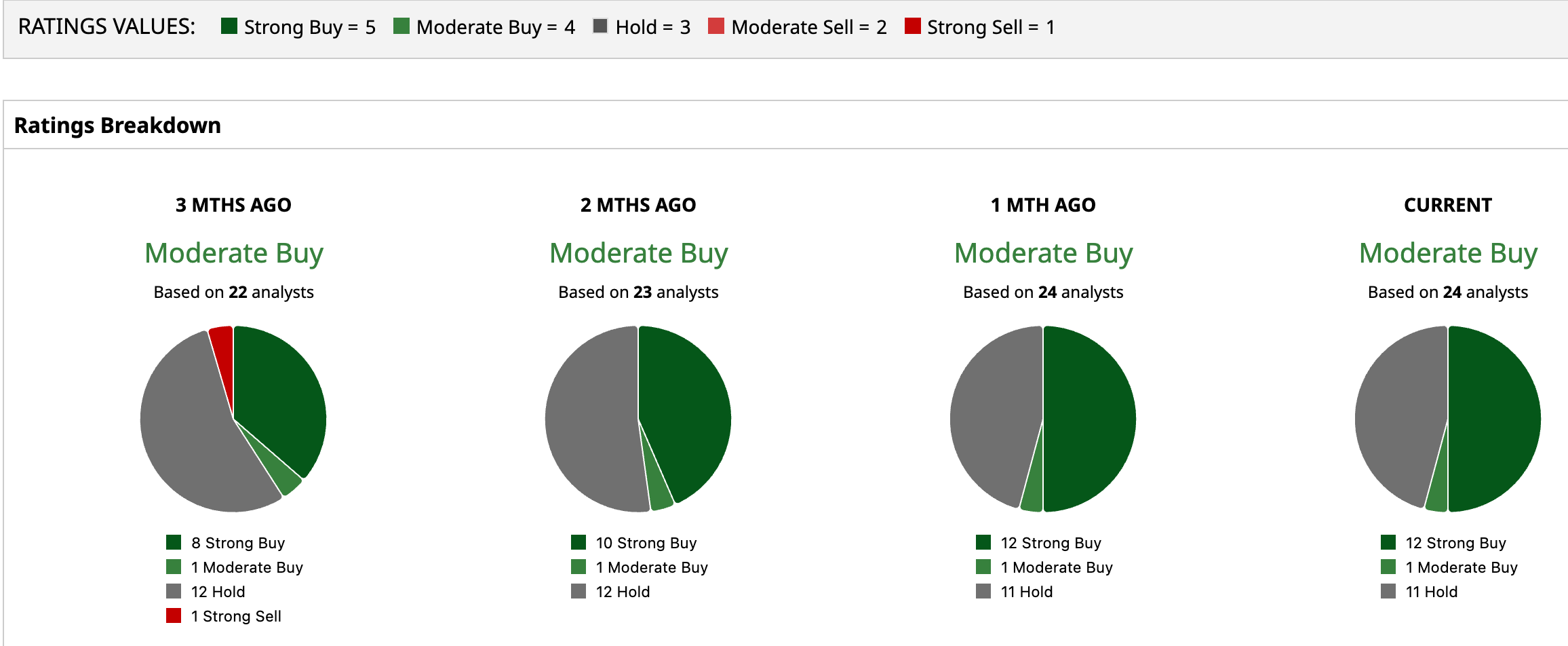

AEP has a consensus rating of “Moderate Buy” from the 24 analysts polled. Its mean target price is $142.90, which is 9.17% higher than current levels. The recent analyst action has been subdued at best, and there were only cursory target price adjustments following the Q1 2026 earnings earlier this month.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comShould You Buy AEP Stock?

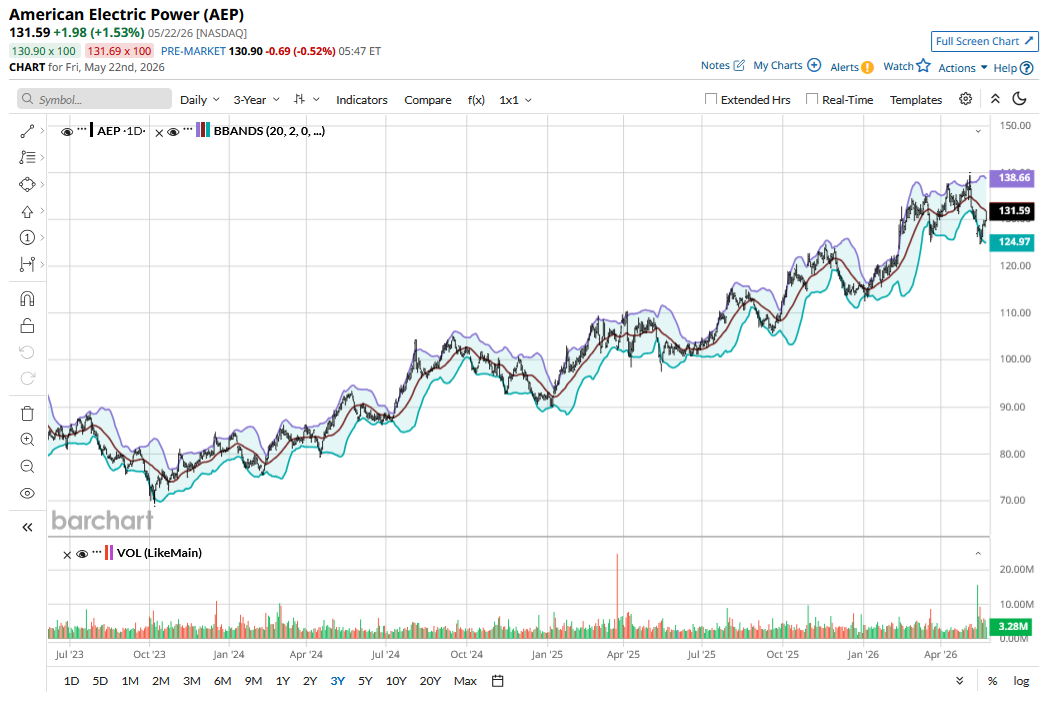

In a previous article, I noted that the near-term upside for AEP looked capped given the stretched valuations. The stock has been trading at similar levels since March, when I last covered the company, even though the broader markets have risen to record highs.

My view about American Electric hasn’t changed, as the forward price-to-earnings multiple of 20.73x leaves little on the table for short-term upside. I won't harp much on the multiples being higher than historical averages, as utilities like AEP have seen a structural rerating amid the soaring power demand from AI. However, the risk-reward does not look too favorable at these levels, and I would give the stock a pass for now.

On the date of publication, Mohit Oberoi had a position in: NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Jefferies Just Upgraded Generac Stock. Here’s Why. Billionaire Dan Loeb’s Third Point Just Took a New Position in Hut 8. What This Means for HUT Stock. Wall Street Is Only Just Beginning to Recognize Advanced Micro Devices’ Agentic AI Upside Potential Why You Should Buy Marvell Technology Stock Before May 27