Microsoft (MSFT) stock looks like a buy right now. Shares of the tech behemoth have fallen 11% in 2026 and currently trade at an attractive multiple. But a fresh catalyst is taking shape, one that Wall Street is beginning to price in.

HSBC analyst Stephen Bersey argues that Microsoft's partnership with the artificial intelligence startup Anthropic could generate $43 billion in annual Azure revenue by 2030.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Comparatively, Microsoft reported sales of $282 billion in fiscal 2025 (ended in June).

Why the Anthropic Deal Could Be Microsoft's Next Big AI Win

Microsoft is among the largest investors in OpenAI, the parent company of ChatGPT. Microsoft has invested around $13 billion in OpenAI, making it the primary cloud partner.

In November 2025, Microsoft committed to invest up to $5 billion in Anthropic, the company behind the Claude family of AI models. In exchange, Anthropic agreed to purchase $30 billion of Azure compute capacity. A portion of that investment was deployed during Anthropic's Series G funding round in February. The Claude maker is reportedly on track to more than double its revenue to nearly $11 billion in Q2, according to a Wall Street Journal report. HSBC estimates Anthropic could reach $241 billion in revenue by 2030, up from less than $5 billion in 2025.That kind of growth trajectory has massive implications for Microsoft.

The Math Behind HSBC's $43 Billion Forecast

If Anthropic's compute spending reaches roughly 60% of its revenue by 2030, that would create a $144 billion cloud opportunity across all providers. If Microsoft Azure captures 30% of that spend, which aligns with HSBC's broader Azure market share estimates, the result is a $43 billion annual revenue opportunity.

Today, Anthropic represents just 5% of Microsoft's remaining performance obligations, which is the pool of future revenue already locked in under signed contracts. Compare that with OpenAI's 46% share, and it's clear how much room exists for Anthropic's footprint to expand.

Bersey called this partnership a potential source of major revenue upside, one currently valued at close to nothing.

Microsoft's Q3 Results Show the Demand Is Already There

In its fiscal third quarter, Microsoft reported Azure revenue growth of 40% year-over-year, ahead of expectations. Total cloud revenue crossed $54.5 billion, up 29%. The company's AI business surpassed $37 billion in annualized revenue, growing 123% year-over-year.

Microsoft 365 Copilot paid seats crossed 20 million, with seat additions up 250% year-over-year. Chief Executive Officer Satya Nadella described the pace of adoption as the fastest since the product launched.

The tech giant is investing heavily to keep up with demand. Capital expenditure guidance for calendar year 2026 was raised to roughly $190 billion, making investors nervous.

www.barchart.com

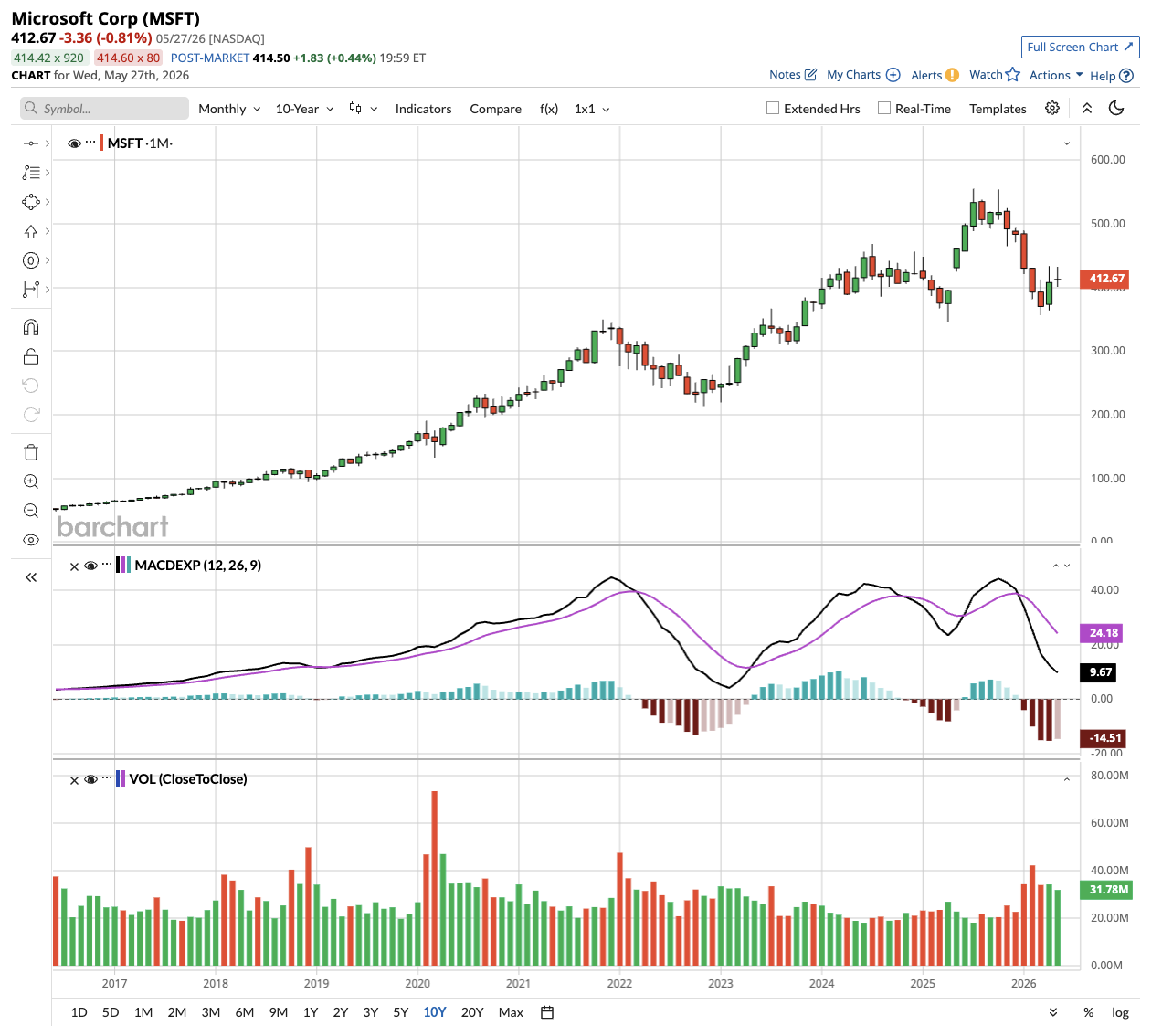

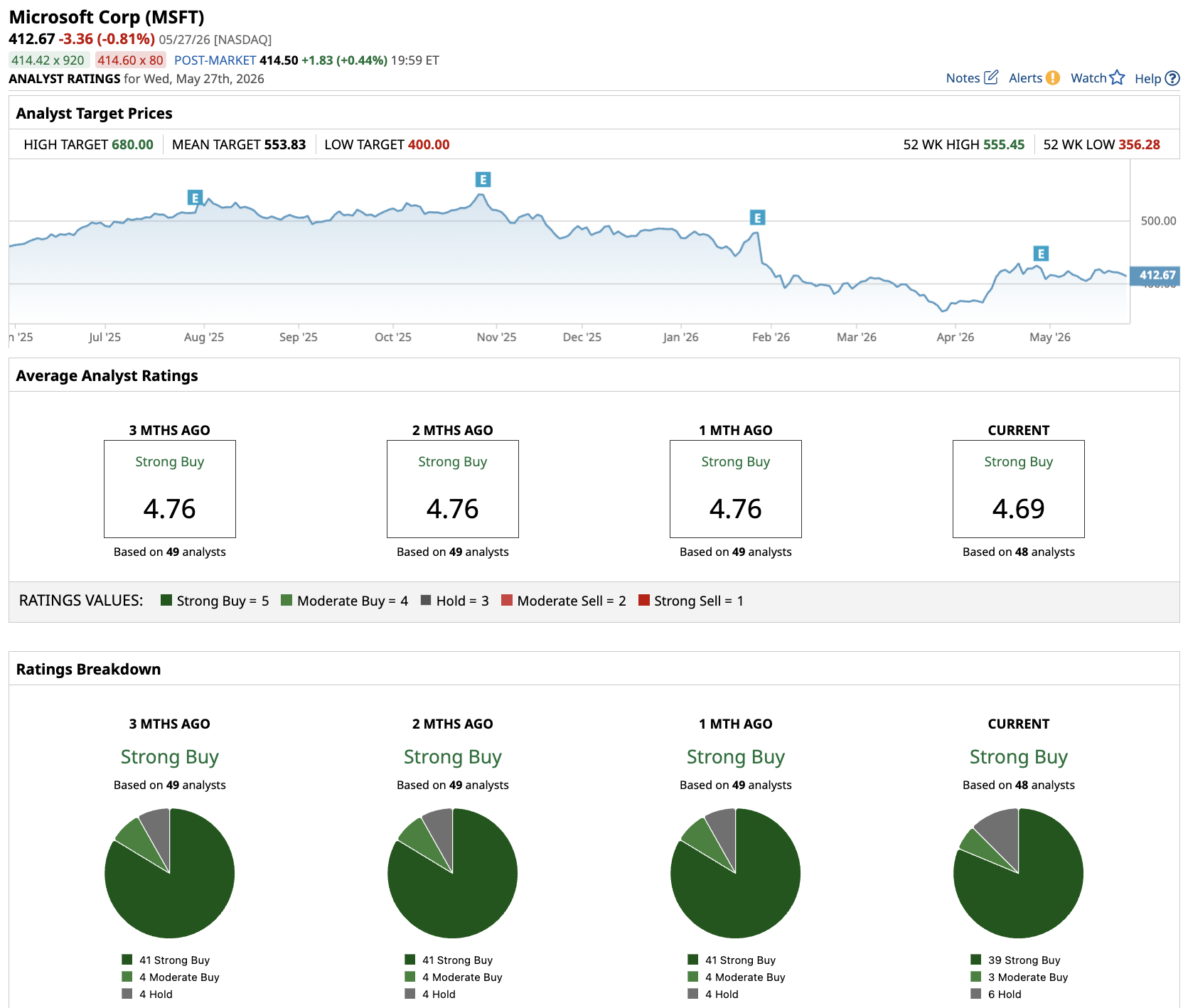

www.barchart.com Microsoft stock is down 11% in 2026 and trades at roughly 22.3x forward earnings, compared with its 10-year average of 28x. MSFT stock trades at a cheap valuation, given that Wall Street projects earnings to grow 18.6% annually through fiscal 2030. Bersey's price target sits at $571 per share, implying roughly 40% upside from current levels.

Out of 48 analysts covering MSFT stock, 39 recommend “Strong Buy,” three recommend “Moderate Buy,” and six recommend “Hold.” The average Microsoft stock price target is $554, above the current price of $423.

The Final Takeaway

Notably, Microsoft has more than $627 billion in remaining performance obligations, which provides visibility into future growth. Revenue tied to Azure is expected to accelerate into the back half of calendar 2026. And the Anthropic deal adds a large, under discussed revenue stream that has barely registered in analyst models.

Heavy spending on data centers today is a sign of confidence in future demand. For investors with a two- to three-year horizon, the stock's current discount appears to be an opportunity that may not last.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Aggressive Share Buybacks and Dominant Positioning Still Make Nvidia Stock a Top Buy Now The $43 Billion Reason to Buy Microsoft Stock Here 2 Reasons Why AMD Stock Is Guaranteed to Beat Nvidia Micron Stock Just Added 3X More Value in One Day Than the Entire Company Was Worth Last Year