ON Semiconductor Corporation ON continued to make progress on profitability in the first quarter of 2026, delivering its third consecutive quarter of sequential gross margin expansion despite a still-recovering demand environment. The company reported a gross margin of 38.5%, up from 38.2% in the fourth quarter of 2025, supported by manufacturing optimization under its Fab Right strategy, higher utilization and a richer product mix tied to AI data centers, automotive electrification and intelligent power.

AI data center revenues were a standout, more than doubling year over year and rising over 30% sequentially, reflecting broader adoption across the power tree with XPU vendors, power supply providers and leading hyperscalers. Management now expects AI data center revenues to double in 2026, strengthening the case for margin-accretive growth.

The company also highlighted several levers that could support its long-term gross margin target of more than 50%. Each point of factory utilization improvement could add 25-30 basis points to gross margin, while Fab Right initiatives and favorable mix could each contribute roughly 200 basis points over time. Treo, ON Semiconductor’s analog mixed-signal platform, is another important driver, given its expected 60-70% gross margin profile.

EliteSiC remains central to the margin story as EV makers shift toward 900V architectures. Expanded collaborations with Geely and NIO reinforce ON Semiconductor’s position in higher-voltage EV systems, where silicon carbide products typically offer stronger profitability. The company’s China automotive revenues grew year over year in the first quarter despite weakness in the broader China passenger vehicle market, underscoring content gains and share opportunities.

Overall, ON’s margin expansion story is gaining credibility. While the 50% gross margin target remains a multi-year objective rather than a near-term milestone, the latest results suggest that the company’s transformation strategy is moving in the right direction.

Key Competitors to Watch in the Power Semiconductor Market

Two important competitors to monitor in the broader analog, industrial and power semiconductor landscape are Texas Instruments Incorporated TXN and STMicroelectronics N.V. STM.

Texas Instruments remains one of the strongest competitors in analog and embedded processing chips, particularly across industrial automation, automotive electronics and data center power management. TXN has spent the past several years aggressively expanding internal manufacturing capacity and 300-millimeter wafer production, positioning itself to support customers during the current semiconductor recovery cycle. Management recently highlighted growing market-share gains driven by improved supply availability, competitive pricing and stable lead times.

STMicroelectronics, meanwhile, continues strengthening its position in automotive power semiconductors, silicon carbide solutions and AI infrastructure applications. The company reported strong momentum in electric vehicle power systems, industrial automation and AI-related data center programs, including collaborations tied to NVIDIA and Amazon Web Services. STMicroelectronics is also expanding its silicon carbide and optical interconnect capabilities to support next-generation AI compute infrastructure and higher-voltage EV architectures.

ON’s Price Performance, Valuation & Estimates

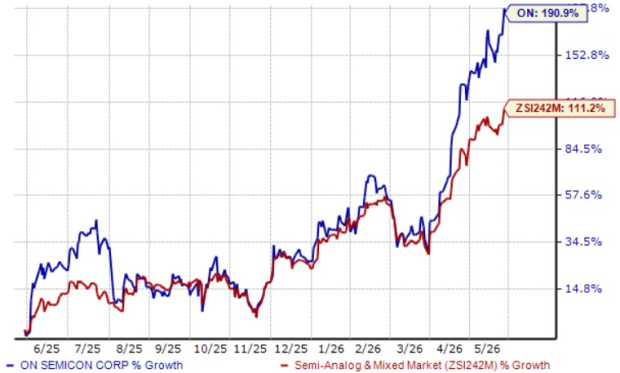

Shares of ON Semiconductor surged 190.9% over the past year compared with the industry’s 111.2% rise.

ON’s One-Year Price Performance

Image Source: Zacks Investment Research

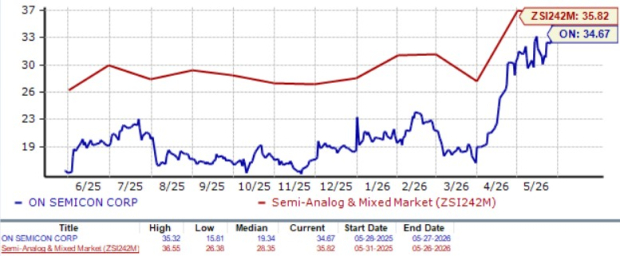

From a valuation standpoint, ON trades at a forward price-to-earnings (P/E) multiple of 34.67, down from the industry’s average of 35.82.

ON’s P/E Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for ON’s 2026 earnings per share has increased in the past 30 days. The company is likely to report strong earnings, with projections indicating a 31.5% year-over-year rise in 2026.

Image Source: Zacks Investment Research

ON Semiconductor currently holds a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

STMicroelectronics N.V. (STM): Free Stock Analysis Report

ON Semiconductor Corporation (ON): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).