Globus Medical GMED is changing how it monetizes surgical robotics. Management is steering enabling technologies toward leases and rentals instead of outright sales. That can lower upfront revenue recognition and make quarterly results less predictable. The aim is to widen the installed base and grow recurring revenue tied to implants, disposables, service and case coverage.

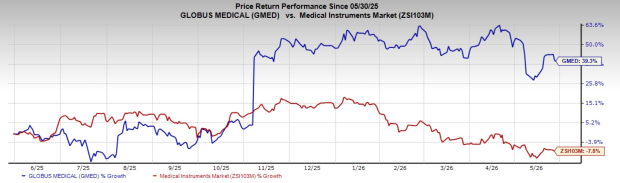

GMED sports a Zacks Rank #1 (Strong Buy). In the past year, the stock has climbed 39.3%, outperforming its industry’s 7.8% fall.

Image Source: Zacks Investment Research

GMED’s Shift to Leases and Rentals Changes the Model

The shift is happening alongside strong top-line momentum. In the first quarter of 2026, revenue rose 27% year over year to $759.9 million, while base business sales excluding Nevro increased 13.2%. Those results suggest the company can push a new commercialization model without losing demand.

Management described continued deal activity in enabling technologies, but with a pipeline shifting toward leases and rentals. A sale recognizes more revenue upfront, while a lease spreads it over time. That is why capital revenue timing can become less linear even when demand is healthy.

Strategically, the company is trading cleaner quarterly optics for a larger footprint. More systems in the field can support recurring streams tied to implants, disposables, service and case coverage, turning placements into a gateway for downstream pull-through.

Globus Medical Builds a Workflow Around Excelsius GPS

The commercial logic centers on Excelsius GPS. Management said the platform supports implant pull-through and cross-selling as surgeons adopt a more integrated workflow. The objective is to make the company’s tools part of repeatable steps that favor the broader portfolio.

In the first quarter of 2026, Enabling Technologies revenue increased 21.1% year over year, a near-term indicator that adoption is building. If the installed base expands through leases and rentals, the workflow linkage to ongoing procedures becomes the value driver.

GMED Patient-Specific Implants Add a New Differentiator

Two early second-quarter Food and Drug Administration 510(k) clearances add to the platform thesis. The company received clearance for a patient-specific lumbar interbody spacer system and for patient-specific rods, both designed to integrate with the Excelsius suite and surgeon planning software.

That integration reinforces the roadmap of linking planning, enabling technology and implants into a single workflow. Patient-specific products can deepen account relationships and lift procedure-level pull-through over time.

Globus Medical Synergies Aim to Lift Margins Over Time

NuVasive integration is positioned to provide operating leverage through common systems and more in-house production. As of Dec. 31, 2025, the company reported $200 million of NuVasive synergies, nearly a year ahead of schedule. Additional benefits are expected as international integrations are finalized in the back half of 2026.

Profitability is already moving in that direction. Adjusted gross margin was 69.2%, and adjusted EBITDA margin was 32.3% in the first quarter of 2026. Management reiterated a long-term adjusted gross margin target in the mid-70s and expects 69% to 70% for full-year 2026. It also raised full-year 2026 adjusted earnings per share guidance to $4.70-$4.80 while reaffirming revenue guidance of $3.18-$3.22 billion.

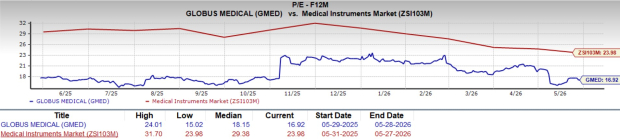

In terms of valuation, GMED trades at a forward, 12-month price/earnings (P/E) of 16.92x, lower than its median and industry average.

Image Source: Zacks Investment Research

GMED Nevro Rebuild Is a Wild Card for 2026 Results

Nevro remains the largest swing factor. In the first quarter of 2026, Nevro contributed $82.7 million of revenue, down $17.1 million from the prior quarter. Management expects lumpiness in the first 24 months while recruiting and retraining the sales organization, targeting a return to a more historical run-rate late in the second half of 2026.

Until that rebuild stabilizes, consolidated growth can look uneven even if the core musculoskeletal franchise is performing well. Investors will want to see sales coverage rebuild without disrupting customer behavior as trading protocols tighten.

Globus Medical Watchlist for Risks and Timing Lumps

The practical watchlist starts with quarterly variability tied to the enabling-technology mix shift. Leases and rentals can broaden adoption, but they reduce upfront recognition versus outright sales and can make comparisons less predictable.

Competition is the second risk. Management noted that new and enhanced robotic competitors are entering the market, which could drive discounting on enabling technology and related implants to protect account access. Stryker Corporation SYK and Teleflex Incorporated TFX both hold a Zacks Rank #3 (Hold), underscoring how quickly pricing pressure can rise when peers stay aggressive. You can see the complete list of today's Zacks #1 Rank stocks here.

Margin sensitivity and foreign exchange volatility round out the list. The long-term gross margin objective in the mid-70s leaves a limited cushion if cost inflation rises faster than pricing. International net sales were $155.0 million in the first quarter of 2026, and a $2.1 million foreign currency transaction loss affected other income and expenses, showing how currency can move reported results.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Stryker Corporation (SYK): Free Stock Analysis Report

Teleflex Incorporated (TFX): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).