NVIDIA Corporation NVDA and Marvell Technology, Inc. MRVL are among the biggest winners of the ongoing artificial intelligence (AI) infrastructure boom. Both companies are benefiting from rising investments in AI data centers, networking, accelerated computing and cloud infrastructure.

NVIDIA dominates the AI graphics processing unit (GPU) market with its full-stack AI platform, while Marvell Technology is rapidly expanding its presence in AI networking, optical connectivity and custom AI chips for hyperscalers.

As AI spending continues to surge globally, investors must be wondering which stock offers the better mix of growth, profitability and valuation support right now.

NVIDIA Dominates AI Infrastructure Market

NVIDIA remains the clear leader in AI computing as demand for its Blackwell systems, networking products and AI software ecosystem continues to accelerate. In the first quarter of fiscal 2027, NVIDIA reported record revenues of $81.6 billion, up 85% year over year, while non-GAAP earnings per share EPS jumped 140% to $1.87.

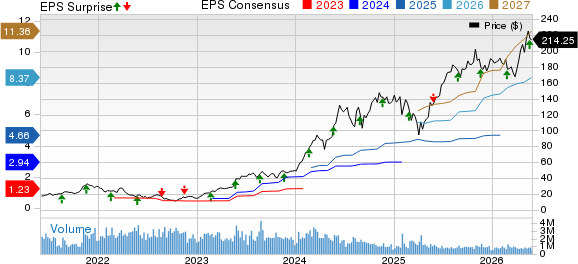

NVIDIA Corporation Price, Consensus and EPS Surprise

NVIDIA Corporation price-consensus-eps-surprise-chart | NVIDIA Corporation Quote

The data center market platform remained the major growth driver, with revenues rising 92% year over year to $75.2 billion. The company’s networking revenues nearly tripled year over year to $14.8 billion, highlighting strong adoption of Spectrum-X Ethernet and InfiniBand technologies across hyperscalers and AI cloud providers.

NVIDIA is benefiting from broad AI adoption across cloud providers, enterprises, sovereign AI projects, and model developers like OpenAI and Anthropic. The company also expects AI infrastructure spending to eventually reach $3 trillion to $4 trillion annually by the end of the decade.

NVIDIA’s CUDA software ecosystem, full-stack AI platform and rapid product launch cycle continue to give the company a major competitive advantage. During the first-quarter earnings call, management also highlighted that its Vera CPUs (central processing units) could open a new $200 billion market opportunity for the company.

Another positive is NVIDIA’s strong profitability and cash generation. The company’s non-GAAP gross margin improved from 60.8% in the year-ago quarter to 75% and generated record free cash flow of $48.6 billion in the quarter. In the first quarter, the company returned $243 million to its shareholders through dividend payouts and repurchased stocks worth $19.3 billion. NVIDIA also increased its dividend rate by 2,400% and expanded its share repurchase authorization by $80 billion, reflecting confidence in long-term growth.

Marvell Emerges as a Key AI Networking Player

Marvell Technology is becoming an increasingly important player in AI infrastructure, particularly in networking, optical connectivity and custom AI silicon. In the first quarter of fiscal 2027, Marvell Technology’s revenues soared 28% year over year to a record level of $2.4 billion, while non-GAAP EPS surged 29% to 80 cents.

Marvell Technology, Inc. Price, Consensus and EPS Surprise

Marvell Technology, Inc. price-consensus-eps-surprise-chart | Marvell Technology, Inc. Quote

Marvell Technology’s data center end market remained the major contributor to the outstanding first-quarter performance. The data center revenues climbed 27% year over year to $1.8 billion. The company expects fiscal 2027 revenues to grow approximately 40% year over year to nearly $11.5 billion, driven mainly by booming AI demand.

Marvell Technology’s biggest strength is its growing exposure to AI networking and optical interconnect markets. The company expects its interconnect business to grow more than 70% in fiscal 2027 as hyperscalers build larger AI clusters that require faster data movement and low-latency connectivity. Demand for 800G and 1.6T optical products is ramping up quickly, while Marvell Technology is also benefiting from increasing adoption of scale-up and scale-across AI networking architectures.

The company is also expanding through acquisitions and partnerships. Its collaboration with NVIDIA around NVLink Fusion, optics and AI-RAN creates new growth opportunities in AI infrastructure. Marvell Technology’s recent acquisition of Polariton Technologies is likely to strengthen its silicon photonics capabilities and improve high-speed optical performance.

Another growth driver is Marvell Technology’s custom AI chip business. During the first-quarter earnings call, management forecasted that custom revenues would more than double in fiscal 2028 as multiple hyperscaler programs ramp up into production. This positions Marvell Technology to benefit from the growing interest in custom AI accelerators among cloud companies.

Nonetheless, MRVL’s profitability remains sensitive to product mix as the company ramps up newer data center platforms. In the first quarter of fiscal 2027, non-GAAP gross margin was 58.9%, down 90 basis points (bps) from the year-ago quarter and 10 bps sequentially. The midpoint of the second-quarter non-GAAP gross margin indicates further contraction. The recent trend suggests that scaling into newer interconnect and custom ramps does not automatically expand gross margin. If mix tilts further toward lower-margin programs or pricing tightens as competition increases, it could hurt the company’s overall profitability.

NVDA vs. MRVL: Which Has the Stronger Growth Outlook?

Both companies will benefit from the surging demand for AI chips, but NVIDIA’s growth profile appears stronger in the near term.

The Zacks Consensus Estimate for NVDA’s current fiscal 2027 revenues and EPS indicates a year-over-year surge of 75.9% and 75.5%, respectively. By contrast, estimates for Marvell Technology’s fiscal 2027 point to more modest 32.3% revenue growth and a 34.5% EPS increase.

The long-term (three to five years) expected earnings growth rate for NVIDIA is also significantly higher than that of Marvell Technology. Currently, NVDA’s long-term expected earnings growth rate is pegged at 51.7%, higher than MRVL’s 39.4%.

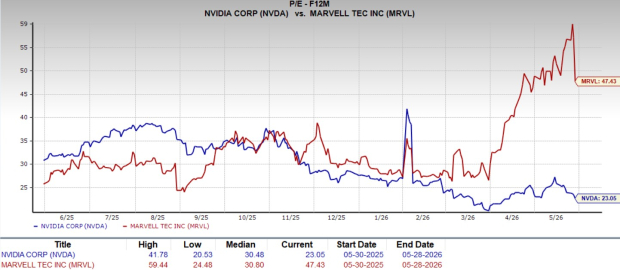

Valuation Comparison: NVIDIA Looks Far More Attractive

Despite its market leadership and stronger financial performance, NVIDIA currently trades at a lower forward P/E multiple of 23.05X compared with Marvell Technology’s much higher multiple of 47.43X. This valuation gap is notable because NVIDIA is growing revenues faster, generating significantly higher margins and producing substantially stronger cash flow.

Image Source: Zacks Investment Research

Marvell Technology certainly offers strong long-term AI growth potential, especially in optical networking and custom silicon. However, much of that optimism already appears reflected in its premium valuation. Investors are paying a significantly higher multiple for a company that is encountering margin contraction.

Meanwhile, NVIDIA combines dominant market share, broad AI exposure, strong pricing power and unmatched software advantages with a more reasonable valuation. This combination gives NVIDIA a stronger risk-reward profile at current levels.

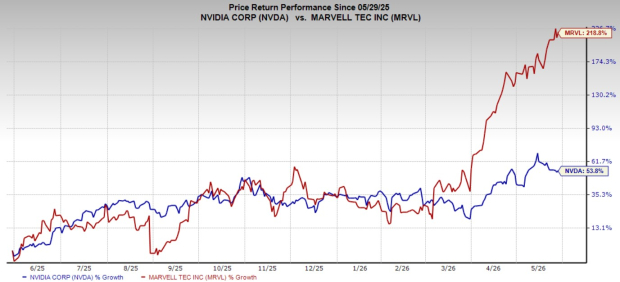

Over the past year, shares of NVIDIA and Marvell Technology have surged 53.8% and 218.8%, respectively.

Image Source: Zacks Investment Research

Conclusion: NVDA Seems to Have an Edge Over MRVL

Currently, NVIDIA and Marvell Technology each carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Both NVIDIA and Marvell Technology are well-positioned to benefit from the massive AI infrastructure buildout happening across hyperscalers, enterprises and sovereign AI projects. MRVL is building strong momentum in AI networking, optical connectivity and custom AI chips, making it an attractive long-term AI growth story.

However, NVDA has an edge over MRVL from an investment perspective. The company continues to dominate AI computing with industry-leading GPUs, networking platforms, software ecosystems and rapidly expanding AI infrastructure solutions. NVIDIA is also delivering superior revenue growth, profitability, free cash flow generation and shareholder returns while trading at a lower valuation multiple than Marvell Technology.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Marvell Technology, Inc. (MRVL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).