Dollar General Corporation DG is set to report first-quarter fiscal 2026 earnings results on June 2, before the opening bell. Investors will closely assess the discount retailer's ability to drive traffic and sales growth in a still-challenging consumer environment while also looking for signs of margin improvement and commentary on the company's outlook for the remainder of the year.

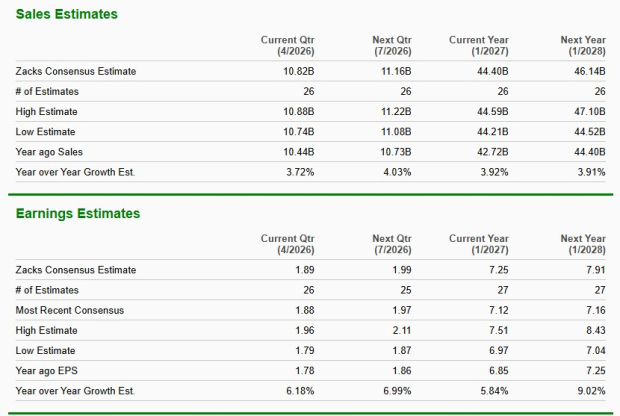

The Zacks Consensus Estimate for first-quarter revenues stands at $10.82 billion, indicating a 3.7% increase from the prior-year reported figure. On the earnings front, the consensus estimate has fallen by a penny to $1.89 per share over the past 30 days, but still implies a year-over-year jump of 6.2%.

Dollar General has a trailing four-quarter earnings surprise of 24.8%, on average. In the last reported quarter, DG surpassed the Zacks Consensus Estimate by 19.9%.

Image Source: Zacks Investment Research

What the Zacks Model Predicts for DG

As investors prepare for Dollar General's first-quarter announcement, the question looms regarding earnings beat or miss. Our proven model predicts that an earnings beat is likely for Dollar General this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Dollar General has an Earnings ESP of +0.82% and carries a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Dollar General Corporation Price, Consensus and EPS Surprise

Dollar General Corporation price-consensus-eps-surprise-chart | Dollar General Corporation Quote

Factors to Note Ahead of DG’s Q1 Earnings

Dollar General's first-quarter performance is likely to have been supported by continued customer demand for value and convenience against a challenging consumer backdrop. Management noted that customers across income levels remained focused on stretching household budgets, which has been driving traffic and market-share gains for the company. The retailer's broad assortment of value-oriented products, including its private-label offerings and everyday low-price strategy, is likely to have continued to resonate with shoppers seeking affordable alternatives. We expect same-store sales growth of 2.2% in the quarter under review.

Another likely tailwind is the ongoing strength in Dollar General's non-consumables business. Management highlighted sustained traction in discretionary categories, supported by brand partnerships, closeout merchandise opportunities and efforts to improve product relevance. The company has been working to expand customer choice while maintaining a strong value proposition, which has helped attract both existing and new shoppers. Digital initiatives, including delivery services and enhanced customer engagement through the myDG platform, may have supported sales growth.

Dollar General entered fiscal 2026 with better inventory positioning, improved in-stock levels and stronger store execution. Management emphasized ongoing benefits from inventory optimization, SKU rationalization and supply-chain efficiencies, all of which have helped simplify operations and improve the shopping experience. Remodel initiatives under Project Renovate and Project Elevate, which have been generating positive customer response and traffic benefits, may have further supported sales performance during the quarter. The company also continued to make progress on shrink reduction and damage-control efforts, which are expected to contribute to healthier merchandise margins.

On the flip side, consumers continued to face inflationary pressures and broader economic uncertainty, which may have kept purchasing behavior cautious. The quarter also began with severe winter storms that temporarily disrupted store operations and customer traffic in the first two weeks of February. Meanwhile, higher costs tied to store operations, maintenance and utilities may have added pressure on SG&A.

Dollar General Stock Price Performance

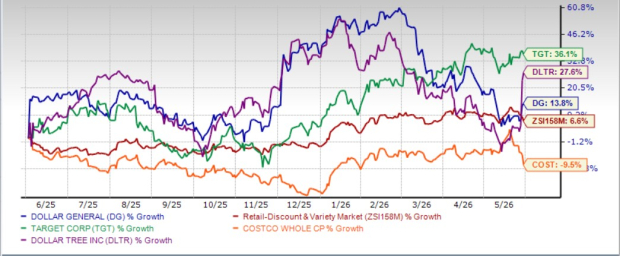

Dollar General, which competes with Target Corporation TGT, Costco Wholesale Corporation COST and Dollar Tree, Inc. DLTR, has seen its share gain 13.8% over the past year compared with the industry’s rise of 6.6%.

While shares of Target and Dollar Tree have advanced 36.1% and 27.6%, respectively, Costco has fallen 9.5%.

Image Source: Zacks Investment Research

Does DG Present a Strong Case for Value Investing?

Dollar General is currently trading at a forward 12-month price-to-earnings (P/E) ratio of 14.81. This valuation reflects a discount compared to the industry’s average of 31.13 and the S&P 500's P/E of 22.26. The stock also appears undervalued compared to its 12-month median P/E level of 17.83.

Dollar General is trading at a discount to Target (with a forward 12-month P/E ratio of 15.00), Dollar Tree (16.51) and Costco (43.66).

Image Source: Zacks Investment Research

Final Words Dollar General Stock

Dollar General heads into its first-quarter earnings release, supported by steady traffic trends, continued demand for value-focused merchandise and progress across its operational initiatives. The company has been executing on several growth drivers, including store remodels, digital expansion and merchandising enhancements, while also working to improve inventory productivity and profitability. Although macroeconomic uncertainty and weather-related disruptions may have tempered some of the quarter's gains, the overall backdrop remains constructive. With earnings indicators suggesting a favorable setup and the stock still trading at an attractive valuation relative to peers, current shareholders may consider staying invested, while prospective investors could view the upcoming report as an opportunity to gauge the sustainability of Dollar General's turnaround momentum.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Dollar General Corporation (DG): Free Stock Analysis Report

Dollar Tree, Inc. (DLTR): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).