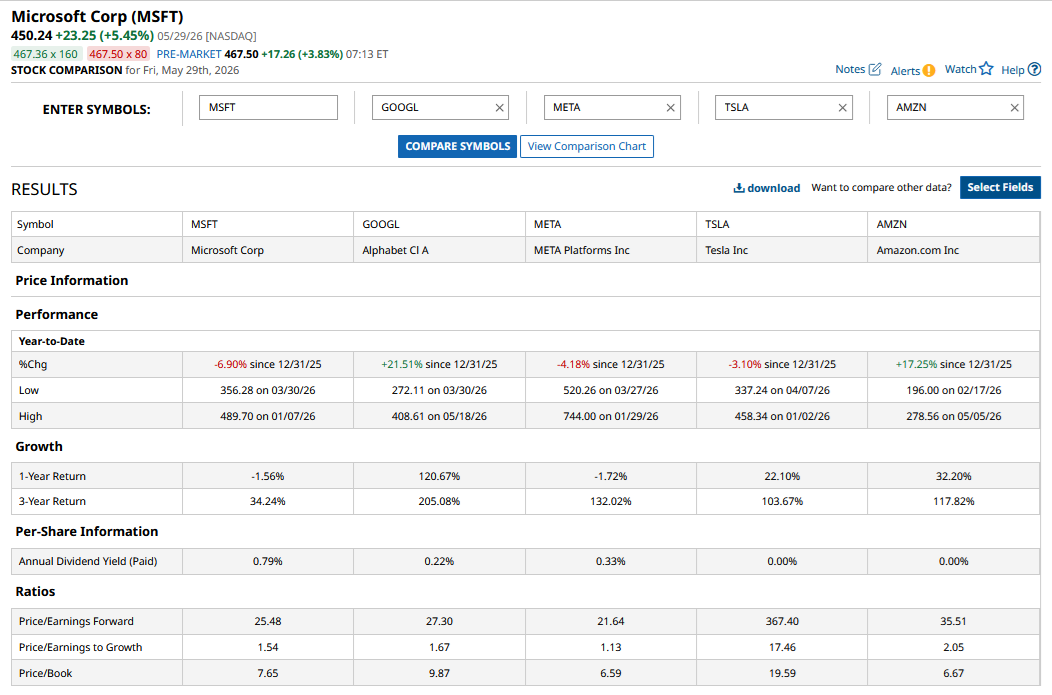

Microsoft stock (MSFT) is up a cool 30% from the 2026 lows that it hit in late March. The rally has helped it bridge its 2026 losses to 7% even though it is still the worst-performing Magnificent 7 so far. Meta Platforms (META) and Tesla (TSLA) are the other two Mag 7 stocks in the red this year and underperforming the S&P 500 Index ($SPX).

Notably, Microsoft’s underperformance is not a 2026 thing; it underperformed the S&P 500 Index in 2024, barely outpaced it in 2025, and was the worst-performing Mag 7 stock in 2024. With Microsoft stock showing some signs of recovery, it would be prudent to examine whether there is still heat left in the rally or whether investors would be better off selling the stock instead.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Why Has Microsoft Stock Rebounded?

To begin with, let’s analyze the key factors behind Microsoft’s recovery. First, there has been a broad-based market rally that supported MSFT’s price action. Secondly, "SaaSpocalypse” fears have subsided, and other software names have also rebounded. On a more company-specific note, Microsoft’s relations with OpenAI seem to have stabilized and the ChatGPT parent’s imminent IPO would be a positive event for MSFT.

Microsoft’s financial performance has also been reasonably good, and it beat on both the topline and the bottomline in the March quarter. The company’s consolidated guidance did fall short of estimates, but its outlook for Azure was better than expected.

Microsoft’s valuation had become too cheap to ignore at the trough. No wonder Michael Burry of “The Big Short” fame and Pershing Square’s Bill Ackman loaded up on the stock this year. Ackman — a self-described “Warren Buffett devotee” — trimmed Alphabet (GOOG) (GOOGL) stake and hinted that he finds the Google-parent overvalued and MSFT undervalued.

Most recently, Nvidia (NVDA) unveiled a new N1X processor that it made with Microsoft and would power new PCs from Microsoft and other OEMs. Commenting on the new chip, Nvidia CEO Jensen Huang said at Taiwan’s Computex conference that “Microsoft and Nvidia are going to reinvent the PC.” He added, “This is the first completely re-engineered, reinvented line of PCs that has happened in 40 years.” AI PCs would drive sales of Microsoft's suite of products as they could fuel a refresh supercycle.

MSFT Stock Forecast

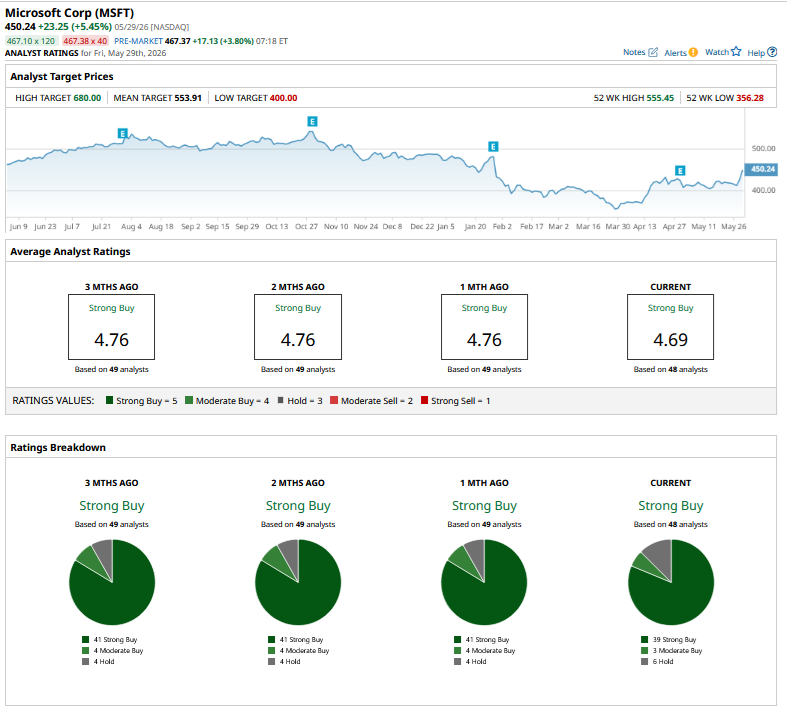

While the sell-side analyst community’s action has been somewhat mixed, most have had a negative bias toward MSFT stock this year and have lowered the stock’s target prices, particularly after the company’s earnings calls. MSFT still has a consensus rating of “Strong Buy” from the 48 analysts polled by Barchart, and its mean target price of $553.91 is 20% higher than the current level.

www.barchart.com

www.barchart.com Can Microsoft Stock Continue Its Good Run?

Microsoft’s valuations have recovered from the trough we saw earlier this year, and the forward price-to-earnings (P/E) multiple has expanded to 25.5x. The multiples are still lower than the average multiples over the last three years, but since the company’s aggressive AI spending is taking a toll on its once enviable free cash flows, I won’t focus much on the historical multiples, which were set in a different epoch altogether for Microsoft.

To be sure, there are similar concerns about other tech giants, as Microsoft is not the only hyperscaler out there that has opened its purse strings in the AI arms race. However, in Microsoft’s case, markets are still not fully convinced about the company’s ability to monetize its burgeoning AI capex. Incidentally, previously Microsoft had said that its capex growth in the fiscal year 2026 would be lower than the previous year, but it subsequently raised its guidance and expects to spend $190 billion this year, which is 61% higher than what it spent in 2025.

Markets have, in general, been wary of tech companies’ ever-rising AI capex, with Alphabet being a notable exception. The company has managed to shed the impression of being an “AI laggard” and has not only protected its turf from the likes of OpenAI but also its cloud business is growing significantly faster than both Microsoft and Amazon (AMZN) in percentage terms.

All said, I believe that while Microsoft’s risk-reward equation is not as mouthwatering as it was a couple of months back, the valuations still look reasonable and the stock has the potential to rise from these levels. Some of the concerns related to Microsoft look overblown, and if the company can come up with a stellar AI success story on the lines of Alphabet, the stock should see considerable upside in the coming months.

On the date of publication, Mohit Oberoi had a position in: MSFT , GOOG , AMZN , TSLA , META , NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A $5 Billion Reason to Buy Salesforce Stock Now Nvidia CEO Jensen Huang Is Building the Future Faster Than Infrastructure Can Support It Dell Stock Is the New Nvidia of AI Infrastructure Why Okta Is One of the Hottest AI-Driven Stocks to Buy Now