Berkshire Hathaway (BRK.A) (BRK.B) announced on May 31 that it will acquire Taylor Morrison Home Corporation (TMHC) in an all‑cash deal valued at about $6.8 billion. This is Greg Abel’s first major acquisition since he took over from Warren Buffett as CEO earlier in 2026.

The transaction lands at an important moment for the U.S. housing market. White House economists estimate a shortage of roughly 10 million homes in the U.S. They say regulatory changes could unlock more construction, which could help steady prices and make homeownership more attainable.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Taylor Morrison sits right in the middle of that story. The company is one of America’s leading homebuilders and has been named by Fortune as one of the World’s Most Admired Companies, ranking No. 2 among homebuilders. It operates in more than 350 communities across 21 markets, giving it wide exposure to key housing regions.

Berkshire’s decision to commit $6.8 billion to TMHC shows how appealing large, profitable builders with strong balance sheets look in a market that still lacks enough homes. So, what makes Taylor Morrison such an attractive target for Berkshire Hathaway?

Taylor Morrison’s Numbers Back the Bet

Taylor Morrison Home builds and sells single‑family and multifamily homes across the U.S. and is headquartered in Scottsdale, Arizona. The stock is up 21.43% year-to-date (YTD) and 27.99% over the past 52 weeks.

www.barchart.com

www.barchart.com The company’s equity is valued at $6.68 billion, and the stock still looks cheap at 10.13 times trailing price-to-earnings versus a sector median of 14.90 times, and 0.92 times price-to-sales equal to the sector median.

Its latest numbers help show why that offer came in, with their first-quarter 2026 results released on April 21. They posted adjusted earnings per share of $1.12, ahead of the $0.82 consensus estimate, for a 36.59% earnings surprise.

TMHC’s GAAP net income for the quarter came in at $99 million, or $1.01 per diluted share, while adjusted net income reached $109 million. That result was backed by $1.3 billion in home closings revenue from 2,268 closings at an average sales price of $578 thousand, showing the company was still selling homes at solid prices.

It also put $503 million into land and development, which adds to its future community pipeline, and spent $150 million to buy back about 2.5 million shares. That gave shareholders more value even before Berkshire stepped in.

The balance sheet of THMC remained solid, with total liquidity of about $1.6 billion, including $653 million in cash. TMHC’s operating cash flow for March 2026 showed an outflow of $10.43 million, while net cash flow came in at -$197.8 million, reflecting ongoing investment in the business rather than balance sheet strain.

Berkshire’s Big Bet On Taylor Morrison

Berkshire Hathaway’s agreement to acquire Taylor Morrison Home Corporation comes with clear, hard numbers. The deal puts the enterprise value at about $8.5 billion and prices the equity at $72.50 per share in cash, which is roughly a 24% premium to Taylor Morrison’s prior closing price of $58.50.

This transaction is an all‑cash offer and is expected to close in the second half of 2026, subject to shareholder approval and standard regulatory checks, providing existing TMHC holders with a clean cash exit and Berkshire with full control of the builder’s future cash flows.

Another piece of the puzzle is how the company keeps its brand visible. Taylor Morrison recently teamed up with Liquid Death for a campaign built around what they call “the ultimate home luxury.” This promotion offers one winner a new Taylor Morrison home in select markets where every water fixture is plumbed to deliver Liquid Death’s soda‑flavored sparkling water. This turns a basic utility into something that stands out with younger, brand‑aware consumers.

That level of detail in both the acquisition terms and the marketing playbook helps explain why a buyer like Berkshire is comfortable attaching a multibillion‑dollar value.

What Wall Street Still Sees in TMHC

Taylor Morrison’s next earnings release is scheduled for July 22, 2026, and its current estimate for the June 2026 quarter is $1.09 in earnings per share. The prior year’s figure for the same period was $2.02, which implies an estimated year‑over‑year decline of 46.04% in quarterly EPS.

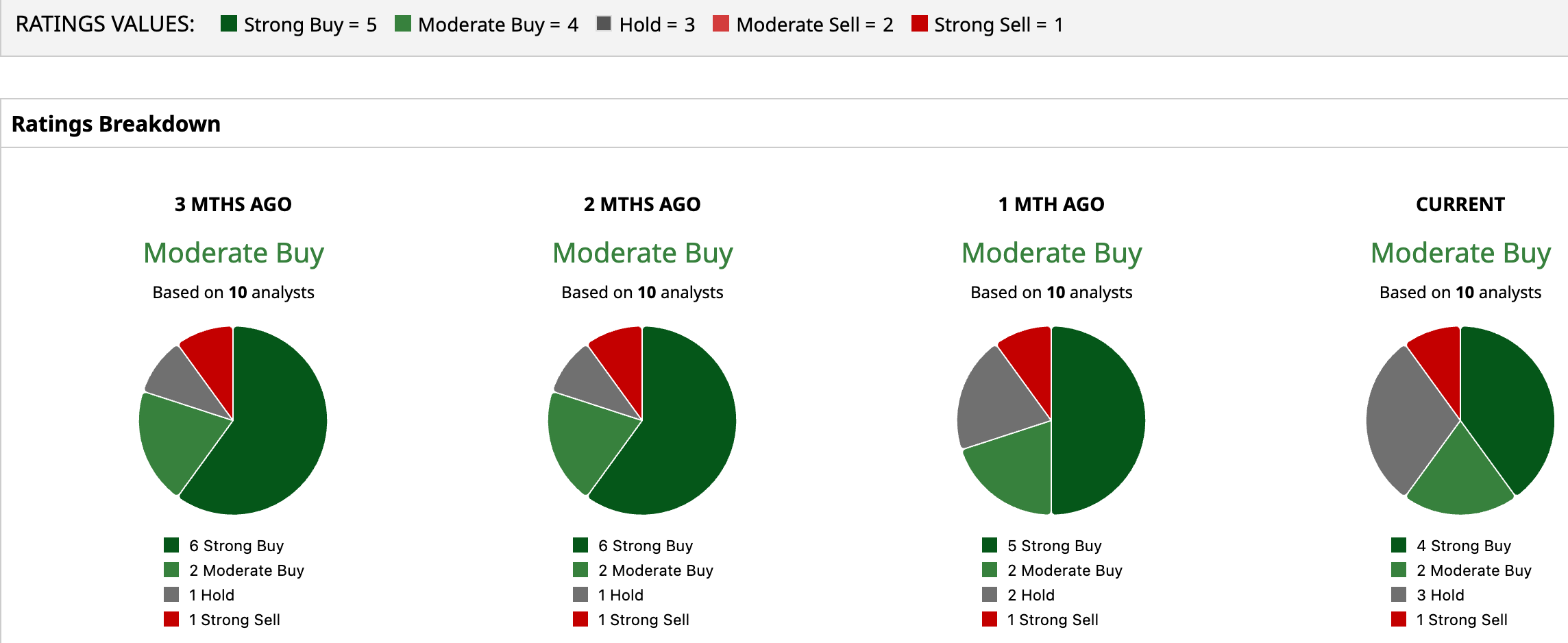

The broader analyst view helps put that drop in context. The consensus rating on TMHC is “Moderate Buy,” based on input from 10 analysts. The average price target is $66.19, which points to a 7.4% downside on a pure trading basis.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comConclusion

Berkshire’s $6.8 billion cash bid answers the main question around Taylor Morrison by putting a clear premium on its earnings, land base, and balance sheet in a tight housing market. The stock's most likely path is a slow move toward the deal price as closing nears, with only modest swings on news about approvals. In practical terms, most of the easy upside has already been locked in by Berkshire’s check.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Berkshire Hathaway Agrees to Buy Taylor Morrison for $6.8 Billion. What This Means for TMHC Shareholders. Intel Sets Sights on Nvidia and AMD With Upcoming AI Data Center Chip Launch by Year End Even If Eli Lilly Stock Continues to Shine, Stay Away from This Pharmaceutical ETF Micron Stock Could Still Have Nearly 70% Upside Potential Left in Its Tank