The options market gives us an inkling of the sentiments surrounding a stock. The one for AI chipmaker Broadcom (AVGO), before its Q2 print, signaled a bullish overtone. However, straddles on the company's stock were also trading heavily. Straddles are basically a hedge against a volatile price movement, either on the upside or downside.

These straddle owners must be relatively happy after shares of Broadcom plummeted 14% in after-hours and early Thursday trading, as investors were not enthused about the company's software sales for the quarter, which came in below estimates. This, I reckon, could be one of the best opportunities to buy the stock cheaply.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Broadcom

With its roots tracing back to 1961, Broadcom is the leader in the custom ASICs market. Broadcom operates two primary business segments currently: Semiconductor Solutions and Infrastructure Software. While the former is predominantly focused on custom silicon for data centers, the latter is geared towards enterprise software.

Valued at a market cap of $2.28 trillion, AVGO stock is up 19% on a year-to-date (YTD) basis. Further, the stock offers a dividend yield of 0.57%, having raised its dividends consecutively over the past 16 years.

www.barchart.com

www.barchart.com Panic-Free Q2

The share price decline was exaggerated. A look at the company's Q2 results will prove it.

Broadcom's net revenues for the second quarter came in at $22.2 billion, up 48% from the previous year. Within this, revenues from the semiconductor solutions segment, which is the company's flagship chip business, made a leap of 79% in the same period to $15 billion. The management expects the segment to generate revenues of $16 billion in Q3, which would imply an even sharper jump of 200%. Sales from the much-in-focus software segment rose by a modest 9% on a year-over-year (YoY) basis to $7.2 billion, contrary to Street expectations of $7.3 billion.

Meanwhile, earnings rose by 54% from the prior year to $2.44 per share, surpassing the consensus estimate of $2.40 per share, making this the ninth consecutive quarter of earnings beat from the company.

Notably, the cash generation capabilities of the company also remained robust. Cash flow from operations rose by 60% on a YoY basis to $10.5 billion. Overall, Broadcom exited Q2 with a cash balance of $19.6 billion, which was much higher than its short-term debt levels of $2.3 billion.

However, AVGO's valuation remains at heightened levels when compared to the sector median. Its forward P/E, P/S, and P/CF at 42.38, 22.12, and 41.19 are all much above the sector medians of 26.65, 3.73, and 21.22, respectively.

Be With Broadcom

In my last analysis of Broadcom, I had deemed the company to be unstoppable and cited the reasons for the same. Since then, the stock has lived up to the moniker, rising by 35%, handily outperforming the S&P 500 ($SPX).

Not much has changed since then on a fundamental basis, with the company's varied involvement across AI infrastructure combined with its highly profitable software operations creating substantial potential for continued expansion over an extended period. Moreover, the CEO has emphasized that relationships with key customers continue to grow stronger. For example, Google (GOOG) (GOOGL) TPU installations dedicated to Anthropic are forecasted to approach one gigawatt in 2026 and move past three gigawatts by 2027. OpenAI plans to deploy over one gigawatt of its initial generation chips by 2027 as well. Even amid doubts expressed by analysts, the Meta (META) MTIA initiative is believed to be aiming for several gigawatts of capacity by 2027 and in the years that follow.

Coming to the software segment, the apparent softness in the latest results should not overshadow the strong contributions from the VMware-led division or its promising future value for Broadcom. VMware Cloud Foundation continues to establish itself as a central software foundation for organizations developing private AI infrastructure by integrating CPUs, GPUs, storage, and networking into one cohesive system. This represents an attractive story that many investors have yet to fully recognize.

Notably, the platform is transitioning from primarily a tool for margin improvement into a core strategic enterprise AI offering and a major long-term growth driver for the company. In the first quarter of 2026, VMware bookings surpassed $9.2 billion while annual recurring revenue grew 19% compared with the prior year.

Taking a closer look at VMware Cloud Foundation (VCF), the company recently introduced version 9.1, an advanced private cloud solution built for AI and Kubernetes environments. It provides comprehensive security features along with support for mixed computing setups that deliver full-stack compatibility across AMD (AMD), Intel (INTC), and Nvidia (NVDA) GPUs as well as other accelerators. The platform also accommodates Broadcom's own accelerators and its partner Google's tensor processing units. As a result, version 9.1 allows businesses to roll out inference and agent-based AI applications at much lower costs while offering the freedom to select top-performing GPUs, accelerators, and central processing units together with the high level of security only possible in an on-premises private cloud setting.

In summary, no other firm matches this unique position of designing compute engines and high-speed networking solutions while combining them with highly optimized virtualization software. This provides complete stack support for GPUs and accelerators from Nvidia, AMD, Intel, Google, and Broadcom, along with the ability for customers to freely combine these components in their on-premises hybrid data centers.

Analyst Opinion on AVGO Stock

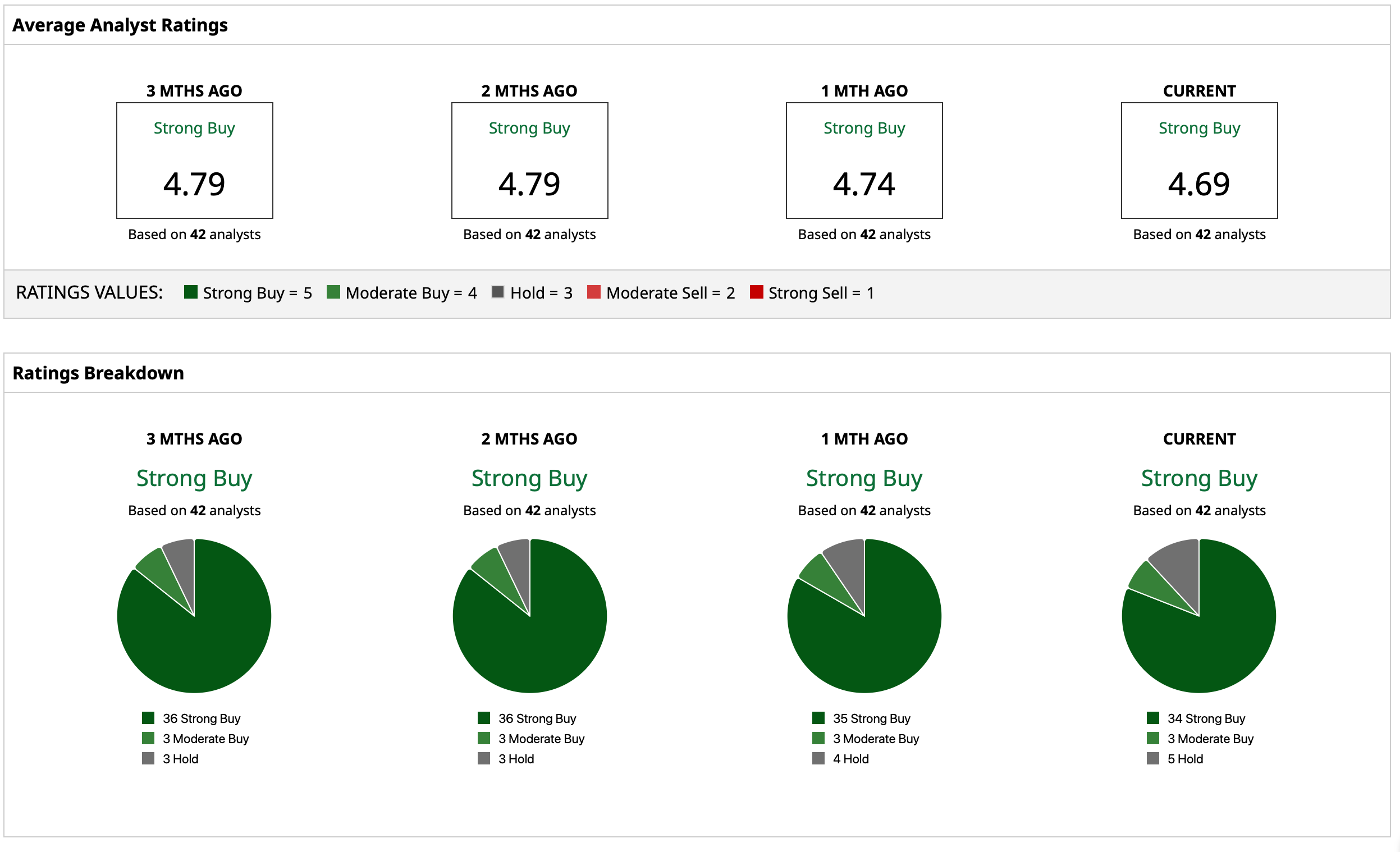

Thus, unsurprisingly, analysts have earmarked an overall rating of “Strong Buy” for AVGO stock, with a mean target price of $484.54. This indicates an upside potential of about 18% from current levels. However, despite today's dip, this will still likely be revised upwards soon. Out of 42 analysts covering the stock, 34 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and five have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

ASML Stock Is Hot, But Please Don’t Go Too Overweight on Chip Stocks Broadcom’s Q2 Results Brings Fails to Bring Optimism to AVGO Stock. Options Data Predicted It. Trump Just Gave Caterpillar Stock a Boost. What to Know. Broadcom Stock Drops After Earnings. Buy the AVGO Dip.