The property and casualty (P&C) insurance market is looking mixed in 2026. Commercial property pricing fell 7.1% in Q1, its weakest reading on record, according to the Baldwin Group's first-quarter Market Pulse Report. At the same time, casualty lines such as umbrella insurance picked up again, rising 8.2% as social inflation and large court awards kept pressure on the market.

That split is pushing insurers to be more selective, and the better-run names are standing out. Some are also showing confidence through shareholder payouts. Allstate (ALL) recently declared a $1.08 quarterly common dividend payable on July 1, 2026, while the Hanover Insurance Group (THG) declared $0.95 payable on June 26, 2026.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

That is the backdrop for W. R. Berkley (WRB). On June 2, 2026, the company declared a special cash dividend of $0.50 per share and raised its regular quarterly dividend to $0.10 per share, up 11.1% from $0.09. Both will be paid on July 2, 2026, to shareholders of record on June 23, 2026. W. R. Berkley also restored its share repurchase authorization to 25 million shares. Including dividends already paid this year and buybacks through March 31, 2026, total capital returned to shareholders in 2026 has reached about $558.8 million.

Even so, WRB stock is down more than 9% over the past year, while the S&P 500 ($SPX) is up roughly 24%. Does the dividend increase and $0.50 special payout make the stock worth buying here? Let’s take a closer look.

Inside W. R. Berkley’s Financial Performance

W. R. Berkley is a specialty commercial insurer that focuses on selected parts of the market where careful underwriting and smart pricing matter more than just writing as much business as possible. Shares of WRB stock are down 9.6% over the past 52 weeks and off by more than 4% so far this year.

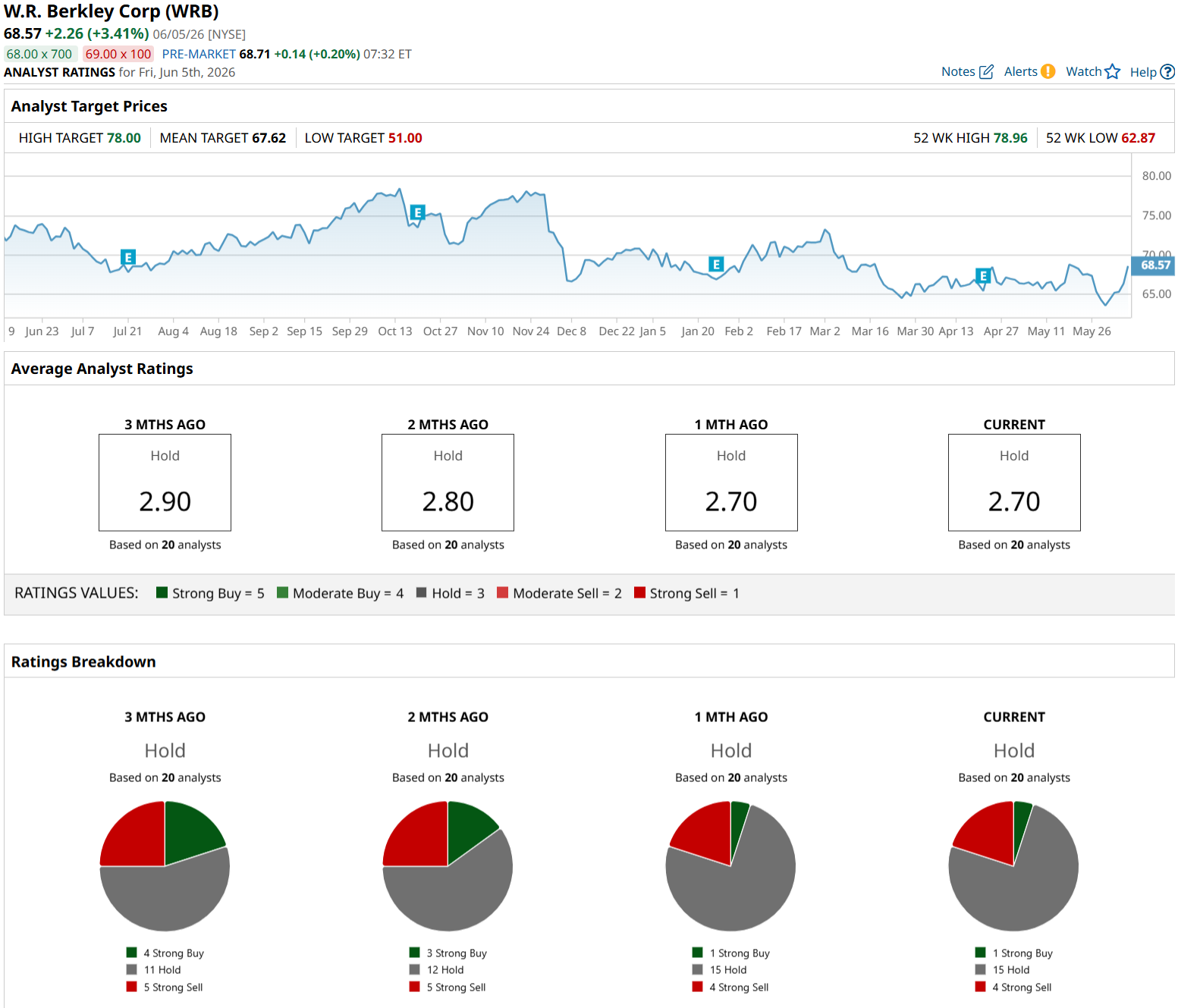

www.barchart.com

www.barchart.com Even so, W. R. Berkley still trades at a forward price-to-earnings (P/E) ratio of 14.2 times, above the sector average closer to 10 times.

W. R. Berkley offers a yield of 2.71%, and its forward payout ratio is just 38.68%. That leaves plenty of room for more dividend increases. The company has now raised its dividend for 25-straight years and pays shareholders quarterly. Before the latest increase, its most recent dividend was $0.09 per share.

In Q1 2026, revenue rose 4% year-over-year (YOY) to $3.69 billion, though that came in a bit below estimates. Adjusted EPS was stronger at $1.30, beating expectations by 14%. Operating margin improved to 16.7% from 15.2%, return on equity came in at 21.2%, and net income rose to $515.2 million. Net investment income climbed 12.2% to a record $404.3 million.

Underwriting also stayed solid, with a 90.7% combined ratio and an 88.3% accident-year combined ratio before catastrophe losses. Average rate increases excluding workers’ compensation were about 7.2%, and W. R. Berkley returned $336.1 million to shareholders during the quarter, mostly through buybacks.

Core Drivers Behind Continued Growth

One of the most structurally important developments for W. R. Berkley’s growth story is Mitsui Sumitomo Insurance’s completed acquisition of at least 12.5% beneficial ownership in Q1 2026. This was executed through prior agreements with Berkeley family-related entities, with no shares purchased directly from the company or family, making it a deliberate strategic stake rather than a liquidity-driven transaction.

The Berkley family retains effective voting control over those shares in most circumstances, removing governance overhang while introducing a long-term institutional partner. MSI’s position as a major global P&C insurer with deep underwriting expertise signals alignment on international commercial insurance opportunities, effectively anchoring WRB to a sophisticated balance sheet with global reach.

Capital allocation is reinforcing that growth setup. On June 2, 2026, the company restored its share repurchase authorization to 25 million shares, alongside announcing a $0.50 special dividend and an 11.1% increase in its regular quarterly dividend to $0.10 per share. This follows already active buybacks, with more than 4.47 million shares repurchased through March 31, 2026. By early June, total capital returned to shareholders for the year had reached approximately $558.8 million, combining repurchases, paid dividends, and newly announced distributions.

Analyst Sentiment and Price Outlook

W. R. Berkley is set to report its next earnings on July 20, 2026. For the current quarter, earnings are expected at $1.09 per share, up almost 4% from $1.05 a year ago. The next quarter is forecast at $1.11, marking a roughly 1% increase. For the full year, the estimate sits at $4.67 for 2026, up about 8% from $4.33 last year.

UBS kept a “Neutral” rating on WRB stock on April 27, 2026, and lowered its price target to $68, pointing to limited upside after the stock’s earlier run. Around the same time, BMO Capital Markets analyst Michael Zaremski upgraded the stock from “Underperform” to “Market Perform” and raised his price target from $64 to $68, reflecting better fundamentals but not enough to turn fully bullish.

Based on 20 analysts covering W. R. Berkley, WRB stock has a consensus “Hold" rating. The average price target is $67.62, which is roughly in line with the current price of shares.

www.barchart.com

www.barchart.com Conclusion

W. R. Berkley is doing a lot right operationally, and the 11% dividend hike plus special payout reinforce how strong its capital position is. But the market already seems to recognize that strength. With WRB stock trading slightly above the average analyst target and growth expected to stay steady rather than accelerate, the upside looks limited in the near term. The most likely path from here is continued sideways movement with modest gains tied to earnings execution and capital returns. For now, WRB stock looks more like a hold than a fresh buy unless the valuation pulls back.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

W. R. Berkley Raised Its Dividend by Over 11%, But Don’t Rush to Buy WRB Stock Here INTC Stock Jumps as Google Taps Intel to Make Chips As IBM Unlocks a ‘Multi-Billion-Dollar Opportunity’ With Google, The Stock Is a Buy ServiceTitan Stock Surged on Better-Than-Expected Results Powered by AI. What This Means for ServiceTitan Investors.