Interestingly, the companies that supply the critical infrastructure that makes AI computing possible are becoming more valuable now than the chipmakers themselves. Vertiv (VRT) is one such supplier that has piqued investors’ interest with its outstanding growth. Plus, its inclusion in the S&P 500 Index ($SPX) earlier this year helped spark VRT stock’s year-to-date (YTD) rally of 81%, far better than the broader market's gain of roughly 8%.

Vertiv provides much of the power, cooling, and infrastructure required to run AI data centers efficiently and reliably. Its recent quarter showed that demand is accelerating faster than many investors expected.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Massive Investments to Strengthen Vertiv's Competitive Edge

Vertiv had a remarkably strong start to 2026. In the first quarter, organic sales increased 23% year-over-year (YOY), while net sales rose 30% YOY to $2.65 billion. The company's profitability numbers were even more impressive, with adjusted EPS jumping 83% YOY to $1.17. The Americas served as the main growth driver with a 53% increase in revenue to $1.8 billion, while the Asia-Pacific (APAC) region is slowly building momentum. Organic sales increased 12% in the APAC region, lower than management’s expectations. However, the reason was project timing rather than weakness in demand. While Europe, the Middle East, and Africa (EMEA) remained the company's weakest region in the quarter, management sees market sentiment improving.

Management believes that AI infrastructure is still in the early stages, meaning demand will grow even higher as AI data centers become more complex. As AI deployments become more demanding, it is also raising barriers to entry amid challenges such as tariffs, supply-chain constraints, labor shortages, and operational complexity. Only companies like Vertiv, which have already proven their ability to supply integrated systems, solutions, and services at scale, will have a competitive advantage.

Investors may not fully appreciate how much Vertiv is currently investing to support long-term growth. It is building more factories, services, and products to capture a bigger share of the rapidly growing AI data-center market. The firm is also investing in strategic acquisitions to boost its technological capabilities. For example, the acquisition of Thermal Key is expected to strengthen the company's thermal management portfolio, while the acquisition of BMarko Structures adds custom-engineered structural fabrication capabilities.

Vertiv also generated adjusted free cash flow of $653 million in Q1, which will help pay off debts and invest in future projects. At the end of the quarter, Vertiv’s balance sheet remained healthy with $2.5 billion in cash and investments and a low debt-to-equity ratio of 0.69. Management’s upbeat guidance for the year also reflects confidence in growing demand for AI infrastructure. Revenue and earnings could increase by 34% and 51%, respectively, compared to 2025. Regionally, Vertiv anticipates organic growth in the high-30% range in the Americas, mid-20% growth in APAC, and flat performance in EMEA.

Why Vertiv Could Be Worth More Than Investors Realize

The AI boom is often measured by the growth of semiconductor companies. But AI data centers can’t function efficiently without power systems, cooling infrastructure, thermal management, services, testing capabilities, and operational support. This is why infrastructure companies like Vertiv, which support the data centers, are becoming increasingly valuable. This trend may be helping Vertiv emerge as one of the most valuable suppliers of the AI revolution.

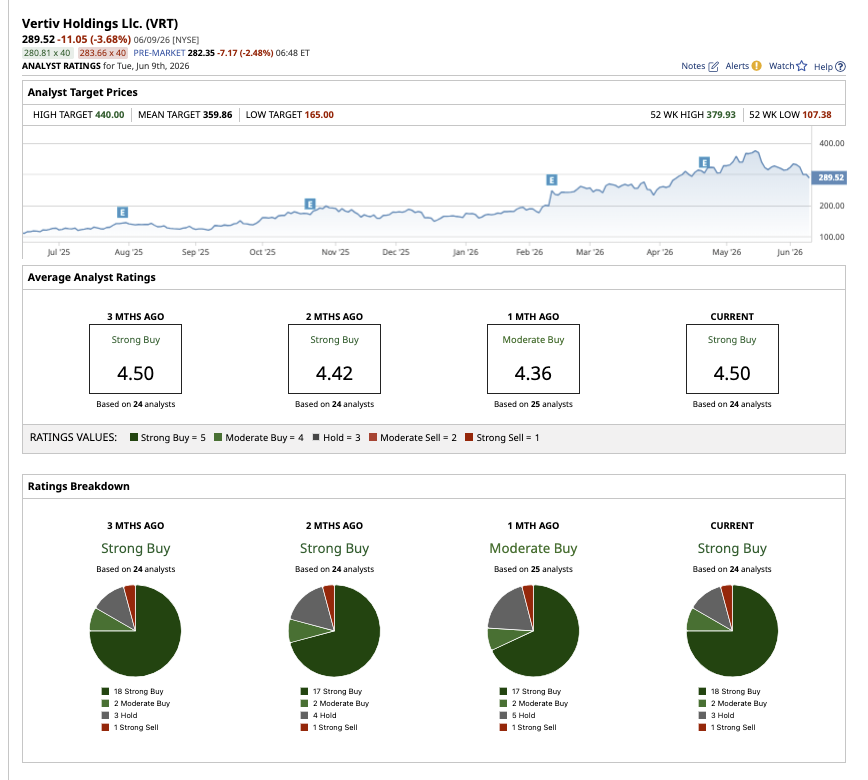

On Wall Street, VRT stock is now a consensus “Strong Buy” versus its consensus "Moderate Buy" rating a month ago. Of the 25 analysts covering the stock, 19 rate it as a "Strong Buy," two call it a "Moderate Buy," three recommend a "Hold," and one analyst has a "Strong Sell" rating. The average price target of $359.86 implies potential upside of 21% from current levels. Furthermore, Loop Capital has assigned a “Buy” rating and a Street-high price estimate of $500, which implies 68% potential upside over the next 12 months. At one point last month, VRT stock also reached a new all-time high of $379.93. With the stock down roughly 22% from that high, now appears to be a good time to buy shares on the dip.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

This AI Supplier Could Become More Valuable Than Investors Expect Evercore Reiterates Amphenol as a Top Pick Thanks to Its Key Role in AI Data Center Infrastructure SPCX Stock Alert: Here's What Analysts Are Saying Ahead of the SpaceX IPO How to Play PBLS Stock After the Parabilis IPO