Qualcomm (QCOM), known primarily for making smartphone processors, is slowly gaining traction in three new markets: Data Centers, Automotive, and IoT. This has led J.P. Morgan’s analyst, Samik Chatterjee, to put the semiconductor company on a positive catalyst watch. He expects Qualcomm to announce revenue targets of over $3 billion by 2027 and $35 billion by 2031 through data centers alone. The data center market is currently dominated by tech giants such as Nvidia (NVDA), Advanced Micro Devices (AMD), and Intel (INTC), so Qualcomm is stepping into a fairly competitive market. In addition, he believes that by 2031, the company will be generating a revenue of $17 billion each from its automotive and IoT sectors.

In the last fiscal quarter, more than 66% of Qualcomm CDMA Technologies (QCT) revenue came from handsets, with the automotive and IoT sectors constituting the remainder. Chatterjee expects this to transform significantly, as he predicts 70% of the firm’s revenue to be through the non-handset market by 2031, with data centers accounting for 35% of it. With the analyst expecting the non-handset revenue to grow by over 40% per year, he’s raised his price target from $160 to $265 while maintaining a “Neutral” rating. This prediction has come just weeks ahead of the firm’s investor day on June 24, where the Qualcomm management will discuss its long-term goals with the Wall Street analysts.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Qualcomm Stock

Qualcomm focuses on the development and commercialization of core technologies and products for mobile devices and other wireless products. The company operates through Qualcomm Technology Licensing (QTL), Qualcomm CDMA Technologies (QCT), and Qualcomm Strategic Initiatives (QSI) segments. It was founded in 1985 and is based in San Diego, California.

QCOM stock posted around a 33% gain over the past year, but its performance fell short of the broader semiconductor sector. The iShares Semiconductor ETF (SOXX) more than doubled during the same period, significantly outperforming the stock. A similar pattern has continued this year. Qualcomm is up approximately 23% on a year-to-date (YTD) basis, whereas the ETF has surged around 97%. Investors continue to pay the short-term price in hopes that the firm can successfully execute its strategy of benefitting from the AI boom.

www.barchart.com

www.barchart.com Qualcomm’s near-term prospects do not look so attractive, with negative earnings growth this year as well as the next. That is mainly because AI data centers are hogging the supply of DRAM memory chips. Smartphone makers are finding it increasingly difficult to get hold of the memory chips to go with Qualcomm’s processors, thus causing phone chipset growth to suffer at least until 2027. This is also why the stock is trading at a forward P/E of just 15.1x, 11% below its five-year average. The stock has priced in most of the positive analyst sentiment and is clearly overvalued here. The company’s objective of taking on the big players in the data center arena continues to hurt the stock’s prospects in the short term.

Qualcomm Posts Strong Earnings

The company reported its second-quarter fiscal 2026 earnings on April 29. It generated $10.6 billion in revenue during the quarter. Non-GAAP earnings came in at $2.65 per share, reaching the upper end of the guidance range. QCT revenue reached $9.1 billion, supported by $6 billion in handset sales and $1.7 billion in IoT revenue, which grew 9% year-over-year (YoY). The Licensing business contributed $1.4 billion.

For the third quarter, Qualcomm expects revenue to range from $9.2 billion to $10 billion. On the earnings side, non-GAAP earnings are projected to range between $2.10 and $2.30 per share. QCT handset revenue is estimated at $4.9 billion. QCT Automotive is forecasted to post around 50% YoY revenue growth.

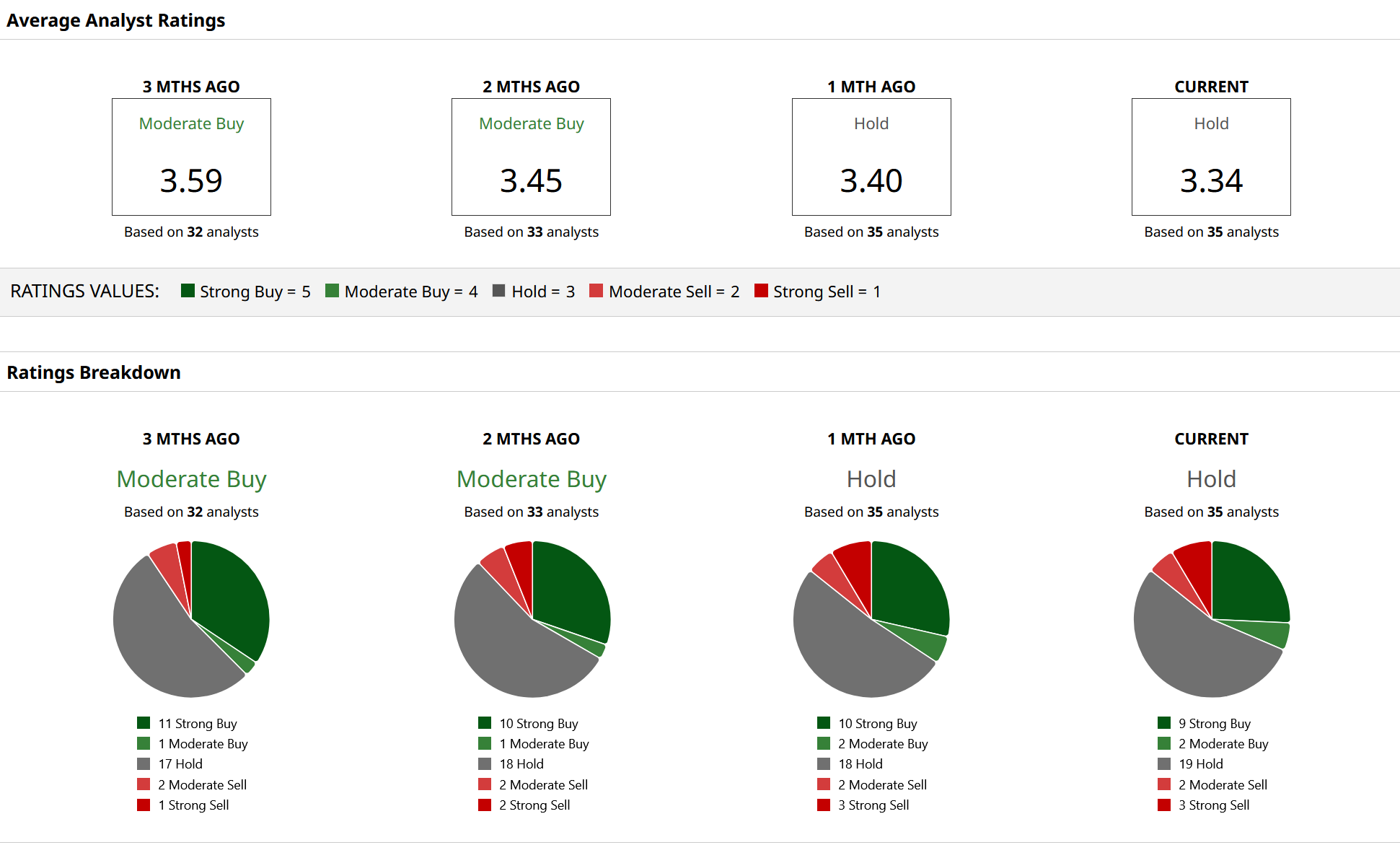

What Are Analysts Saying About QCOM Stock?

Melius Research recently raised its price target on QCOM stock from $170 to $220 while maintaining a “Hold” rating. Earlier, DZ BANK AG downgraded the stock to “Hold” and kept its price target at $195. This highlights that analysts remain on the stock’s outlook.

The stock currently carries a consensus “Hold” rating from 35 Wall Street analysts, suggesting a neutral and balanced outlook. The average analyst price target stands at $184.83, which the stock has already surpassed. However, the highest price target of $300 still reflects 44% upside from the current levels.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Qualcomm Is Striving for a Bigger Piece of AI Infrastructure. Here’s What That Means for QCOM Stock. Options Action: Naked Put Trade Ideas for June 15th Stocks Set to Open Sharply Higher as Oil Sinks on U.S.-Iran Deal, Fed Meeting Awaited Dear Future SK Hynix Stock Investors, Mark Your Calendars for June 22