The artificial intelligence boom has created a bottleneck few investors anticipated. GPUs get the headlines, but memory has become the fuel powering the entire AI ecosystem. Every new AI server requires dramatically more high-bandwidth memory (HBM), DRAM, and advanced storage than previous generations. At the same time, supply remains constrained because these products take years to bring online.

That dynamic has transformed the memory industry from a cyclical commodity business into something much more strategic. Few companies are better positioned to benefit than Micron Technology (MU). A $2,100 share price by 2028 appears achievable if current demand trends continue and management executes on its expansion plans.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

AI Is Reshaping the Memory Market

The key change is that memory is no longer an afterthought in AI systems. Industry forecasts now project the HBM market alone could reach roughly $100 billion by 2028, a figure that would have seemed impossible just a few years ago. Meanwhile, analysts expect memory revenue across the broader industry to continue expanding as hyperscalers build out AI infrastructure. Demand is growing faster than supply, and manufacturers are struggling to add capacity quickly enough.

Micron has emerged as one of the biggest beneficiaries. The company is currently the only major U.S.-based memory manufacturer and has secured design wins across leading AI platforms. Management has stated that HBM capacity is effectively sold out through 2026, while long-term customer agreements are becoming more common across the industry.

Here's what the numbers tell us:

| Metric | Current |

| Trailing Revenue | $58.1 billion |

| Net Income | $24.1 billion |

| EPS | $21.28 |

| Forward P/E | 16.81 |

| Market Cap | $1.10 trillion |

MU Stock's Path to $2,100

Micron should continue benefiting from its leading position in the AI-driven memory market through 2028. If revenue rises from approximately $58 billion today to $110 billion to $120 billion by 2028, that would represent annualized growth of roughly 38% to 44%. Given the industry's supply constraints and pricing power, that is aggressive but not unreasonable.

Management forecasts Q3 revenue of $33.5 billion, a 40% sequential increase and 260% year-over-year (YoY). That sort of acceleration should let Micron double revenue in less than two years, even if it doesn't maintain that same pace.

More importantly, margins are expanding. Micron's high-value AI products already generate higher profitability than traditional memory products. As HBM becomes a larger portion of sales, earnings growth could outpace revenue growth. Management has previously guided toward gross margins above 50%, and analysts expect further improvement as AI memory scales.

Under a reasonable bull-case scenario:

| 2028 Estimate | Value |

| Revenue | $115 billion |

| Net Margin | 35% |

| Net Income | $40 billion |

| EPS | $35 to $40 |

MU stock is not as discounted as it was even two months ago. The market finally woke up to its potential, but applying a valuation multiple of 45 to 60 times earnings—a premium but not unusual for dominant AI infrastructure companies—produces a share price range of roughly $1,575 to $2,400.

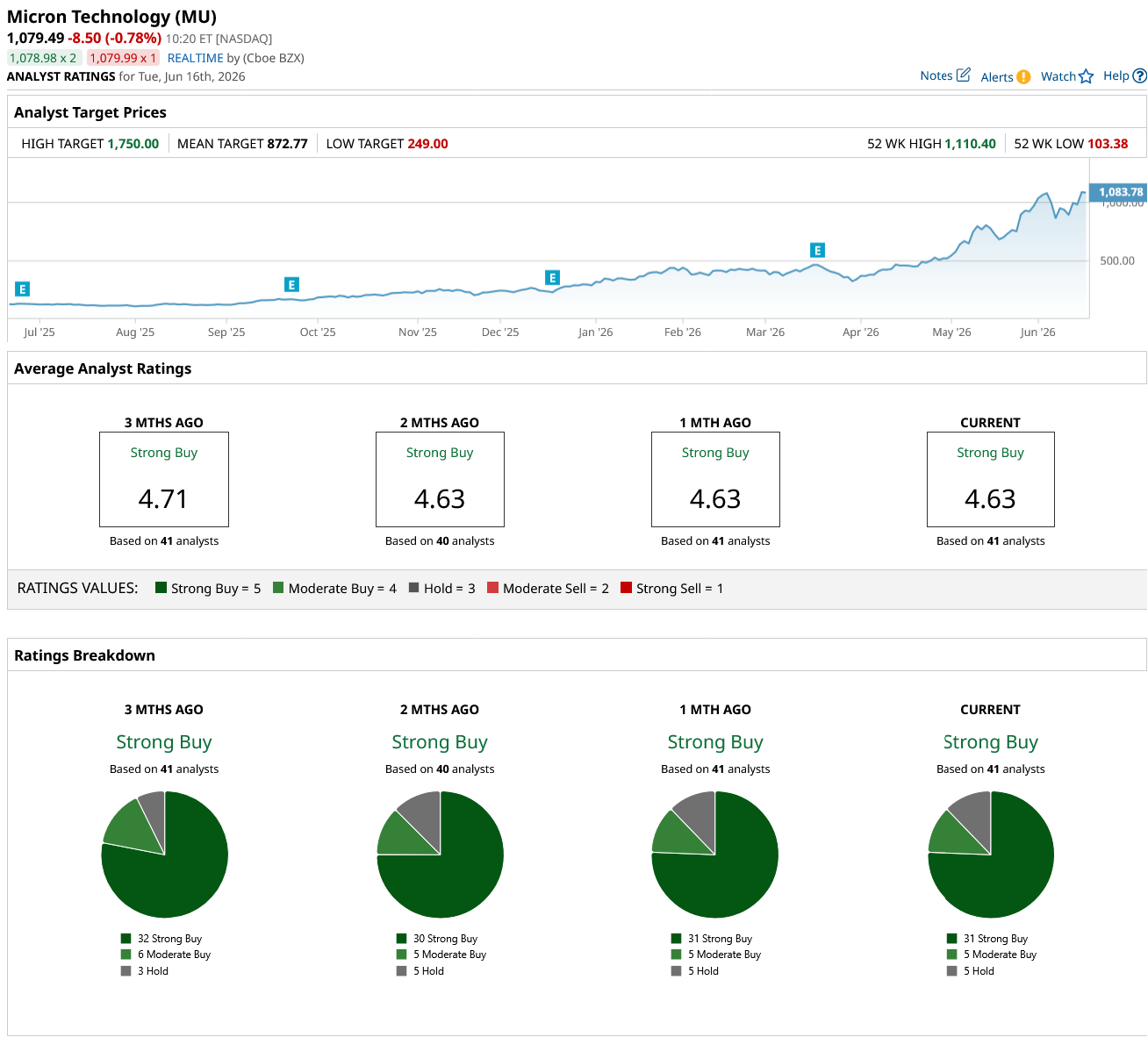

A $2,100 price is not out of the realm of possibility, as Wall Street is already at $1,750 within the next year at the high end of their range. More analysts are raising their targets regularly. In the next 18 months, with solid execution, expect even the mean price target to see a sharp rise.

Granted, the stock traded at much lower multiples during previous memory cycles. The difference today is that investors are increasingly viewing AI memory as a strategic growth market rather than a commodity business.

Wall Street Still Likes the Story

MU stock has already delivered a remarkable run this year, up 285% year-to-date (YTD) and briefly touching $1,089 per share before pulling back to its current $1,079 price. And Wall Street remains overwhelmingly bullish with a “Strong Buy” consensus rating, based on 41 analysts.

Key Takeaway

In short, a $2,100 Micron share price by 2028 does not require fantasy-level assumptions.

It requires continued AI infrastructure spending, successful capacity expansion, and sustained leadership in HBM memory. The company already has much of its future production committed, hyperscalers continue signing long-term agreements, and industry supply remains constrained.

That said, memory remains a cyclical business, and investors should expect volatility along the way. Regardless, if Micron can grow revenue toward $115 billion while expanding margins through higher-value AI products, a $2,100 share price looks less like speculation and more like a plausible outcome.

www.barchart.com

www.barchart.com On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

This Lesser-Known Stock Is a ‘Bunker’ for Your Capital Thanks to Technical Strength The Battle of the Musks: Why Cathie Wood Sold Tesla Stock to Buy SpaceX The Dell Story Is No Longer Just About PCs. Here’s Why the Stock Still Looks Undervalued. CVNA Stock Alert: What to Know as Carvana Expands Into New Vehicles