Applied Materials (AMAT) is forcing investors to revisit a familiar question from tech history. The company now trades at a valuation above its late 1990s peak, when internet enthusiasm drove many technology stocks to unsustainable levels before the “Dot Com” bubble finally burst.

This time, though, the setup is more grounded in real demand. Their Chief Executive Officer, Gary Dickerson, says Artificial Intelligence (AI) is fueling a multi-year expansion in chip manufacturing, and the broader semiconductor market is moving in the same direction.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Industry forecasts now point to global semiconductor revenue surpassing $1 trillion in 2026, helped by strong growth in memory and logic chips as AI spending accelerates. That helps explain the reason that investors are willing to pay such a rich premium for AMAT today.

Still, the setup raises an obvious but uncomfortable question. Has the market once again pushed a powerful story to a price that leaves little room for disappointment, or does Applied Materials truly deserve to trade above its dot-com era high?

Applied Materials Stretched Valuation

Based in Santa Clara, California, Applied Materials is a semiconductor equipment company that designs and sells tools, services, and software used to make chips, displays, and other electronics across steps like deposition, etch, inspection, and advanced packaging.

Their stock has a year-to-date (YTD) gain of 144% and a 52-week jump of 262.76%.

www.barchart.com

www.barchart.com The market is clearly paying up for that performance. The shares now trade at 59.95 times price-to-earnings Non-GAAP (TTM) and 16.25 times sales (TTM), while the sector’s median sits at 25.16 times earnings and 3.63 times sales.

This rich multiple is not coming out of nowhere. Applied Materials reported results for the quarter ended April 26, that help explain why investors are comfortable with a higher price than in past cycles. Their non-GAAP earnings per share came in at $2.86, beating the $2.68 consensus and delivering a 6.72% upside surprise.

The same quarter delivered record revenue of $7.91 billion. GAAP gross margin was 49.9%, and operating income reached $2.52 billion, or 31.9% of sales, which is well above what the company produced during the original internet boom.

There was also a record non-GAAP gross margin of 50.0% and non-GAAP operating income of $2.54 billion, or 32.1% of revenue. The company generated $845 million in cash from operations in that quarter. It returned $765 million to shareholders through $400 million of buybacks and $365 million in dividends. That capital return sits inside a bigger cash flow picture. Their operating cash flow for the April 2026 period totaled $2.53 billion, up 50.12% year-over-year (YOY), while net cash flow was a negative $953 million because management leaned into heavier investment and capital allocation moves.

Applied Materials’ AI Partnerships and Manufacturing Push

Applied Materials has been busy building out its growth pillars. On May 11, the company announced an innovation partnership with Taiwan Semiconductor (TSM) at its EPIC Center in Silicon Valley, extending a relationship that already spans more than 30 years. This work focuses on materials engineering, equipment, and process technologies needed to scale the next generation of AI-focused chips, including advanced logic nodes and more complex 3D transistor and interconnect structures.

Another key area is process purity. Applied Materials has brought SCREEN Semiconductor Solutions into the EPIC Center as an innovation partner, pairing SCREEN’s wafer cleaning and surface prep knowledge with its own materials engineering platform. This partnership aims at co-optimized cleaning and etch solutions for cutting-edge devices, where dense 3D logic, DRAM, and high bandwidth memory all demand tighter tolerances and more intricate surfaces.

The manufacturing base is growing in step with these research efforts. Applied Materials opened a new $500 million manufacturing and R&D facility in Singapore’s Tampines district to serve the rising demand for tools used in AI chips, more than doubling its advanced cleanroom capacity there. It uses autonomous robots, AI-assisted inspection, and closed-loop water systems as part of a broader Singapore 2030 plan that locks the city-state in as a major hub for the company.

Taken together, these moves show AMAT's attempt to sit at the center of AI-driven chip manufacturing rather than just cycling the sidelines.

Analyst Expectations for Applied Materials

Their next earnings release is set for August 13, and that date carries a lot of weight because most of the bullish forecasts are pinned to that report. The current consensus for the July 2026 quarter calls for earnings of $3.35 per share, up from $2.48 a year earlier, which works out to roughly 35.08% YOY growth.

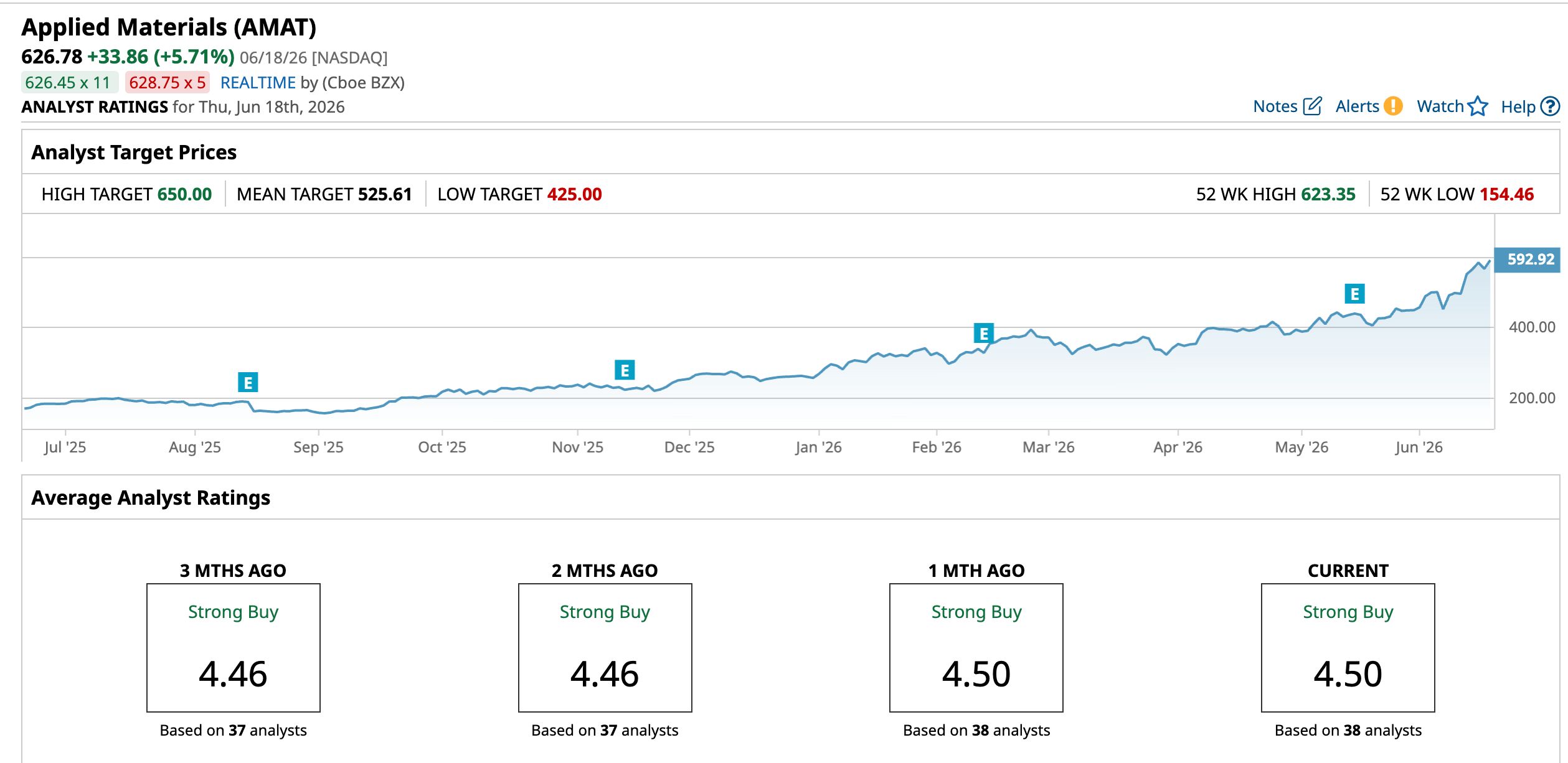

Wells Fargo is leaning into that trend. Their analyst Joe Quatrochi provided an “Overweight” rating and a $435 target, after lifting that target from $350 earlier in the year. Though this is lower than AMAT’s current stock price.

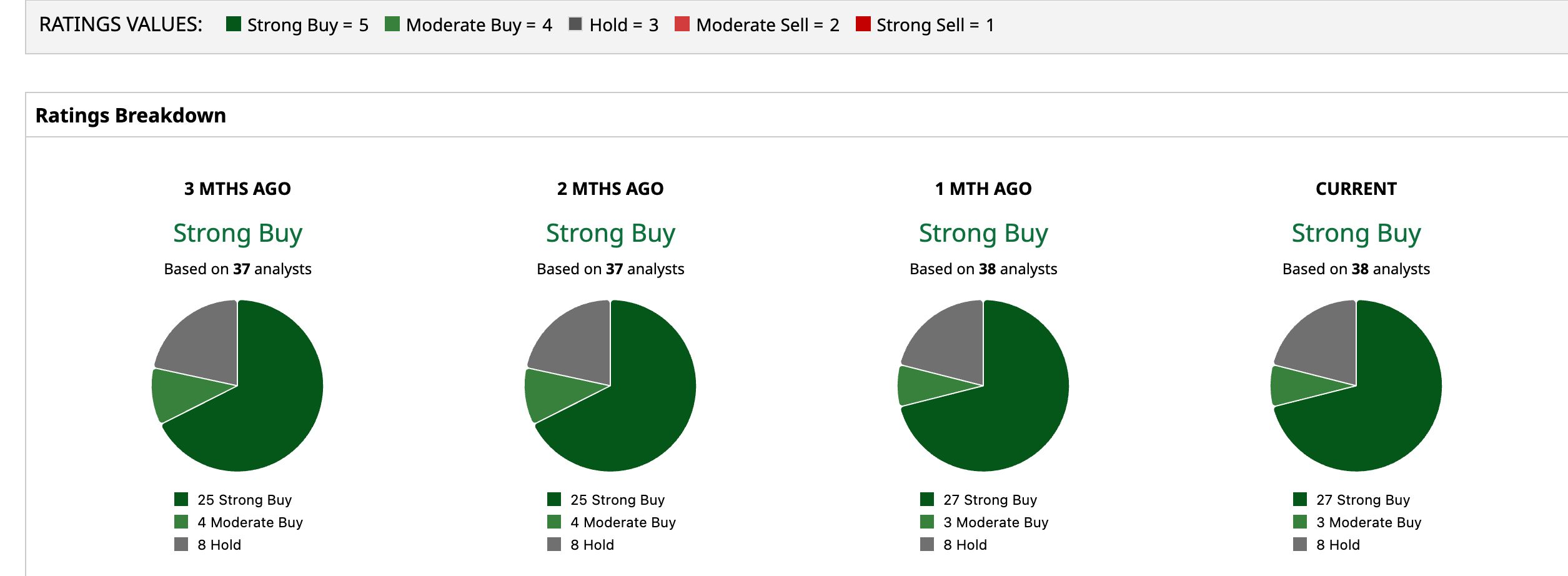

The broader analyst group remains firmly constructive, with 38 covering analysts giving a “Strong Buy” rating. Their average 12-month price target of $525.61 which exhibits 16.14 downside. The Street-high price target of $650 indicates 3.7% upside from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

Applied Materials is no longer running on old dot com nostalgia. The business now sits firmly in the AI hardware stack, and the recent results back that up. But the valuation still leans on optimism. AMAT trades more like a rich growth name than a typical cyclical equipment maker, so the upside from here looks steady rather than explosive. Over the next year, the most likely path is modest gains, with sudden drops whenever AI spending cools or margins show even a small crack.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Applied Materials Is Now More Expensive Than Its Dot-Com Era Peak. AI Demand Justifies the AMAT Stock Valuation. Microsoft vs. Nvidia: Which AI Giant Is the Better Dividend Stock for the Long Haul? Apple Is Betting That Its Next Big Product Could Be AirPods with Cameras 500 Million Reasons to Buy Meta Platforms Stock