Broadcom (AVGO) has seen a slowdown in its momentum in the past few months, and Alphabet's (GOOG) (GOOGL) Google is partly to blame. Google is diversifying away from the big-name AI chip companies to avoid paying high margins and also to increase its own self-sufficiency.

Thus, Google’s next data center inference chip, TPUv9 "Triggerfish," will likely be co-designed with MediaTek instead of Broadcom. Per Wedbush, Broadcom's share of Google's TPU silicon could slide from 95% this year to 65% in just two years. This will have major implications for Broadcom, since less and less of Google's AI spending will reach downstream into Broadcom's income statement.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

In fact, Google is Broadcom's single largest AI customer today. Google accounts for "over 80%" of Broadcom's AI compute sales.

www.barchart.com

www.barchart.com Why Google Is Shifting to MediaTek

Large AI hardware companies are increasing their margins at an unprecedented rate. Meta Platforms (META) CEO Mark Zuckerberg acknowledged this earlier in the year by saying that most of the AI spending increases weren't really about data center expansion. He said "most" of it came from higher component costs.

Broadcom is one of the companies responsible for higher component costs, and it will hurt Google's bottom line if it leans too much into Broadcom.

Google's bill of materials is expected to fall 30-50% if it outsources the inference die to MediaTek, which would save the company billions. MediaTek is likelier to accept much lower margins than Broadcom. Not only that, MediaTek might even be a better choice in the long run. This company has significantly more experience with ARM chips, which are far more power-efficient. After all, MediaTek has been one of the top chip suppliers for mobile phones.

What This Means for Broadcom

Google is a massive customer for Broadcom, but I would not expect AVGO stock to plunge significantly from this news. The company has plenty of demand from other giants to offset Google pulling back. Moreover, Google's pullback is very gradual. Broadcom is still expected to keep the training die, with MediaTek taking the inference die. As AI workload shifts to inference, Broadcom is naturally going to lose orders anyway. This won't translate to lower sales if margins keep rising.

It can get worse for Broadcom if other companies mirror what Google is doing or even shift training dies to companies like MediaTek. However, that's several years away. No company is going to risk a sudden total hardware shift in this environment, especially after DeepSeek fell behind once it switched to Huawei's chips.

Should You Buy AVGO Stock Now?

AVGO stock is down 24% from its 52-week high, and this is a good entry point compared to historical levels. You're now paying less than 20 times forward earnings for a major AI hardware company with rising margins. It did miss revenue expectations by a hair in June, but a 48% year-over-year (YoY) jump in revenue is well into hypergrowth territory, and you're paying low prices for it.

Analysts expect future revenue growth at a 55% annual clip through the latter half of this decade. Companies are increasingly adopting custom AI chips, and the pie is growing so fast that even if Broadcom somehow loses some market share, it can still grow at a tremendous clip.

Debt is a problem at $64.9 billion against just $19.6 billion in cash. Broadcom is an odd one out among large AI hardware companies as it still does not have positive net cash on its balance sheet, but this is no longer a huge problem.

Nvidia (NVDA) spent just $243 million in dividends despite posting $48.58 billion in free cash flow for the most recent quarter. Broadcom spent almost $3.1 billion in cash for dividends during the same quarter, with a free cash flow of $10.26 billion. The company clearly has the firepower to start rapidly paying off debt when it needs to, but it is prioritizing dividends now.

I'd tag AVGO as a buy, but I'll be ready to take profits when the AI rally does sour.

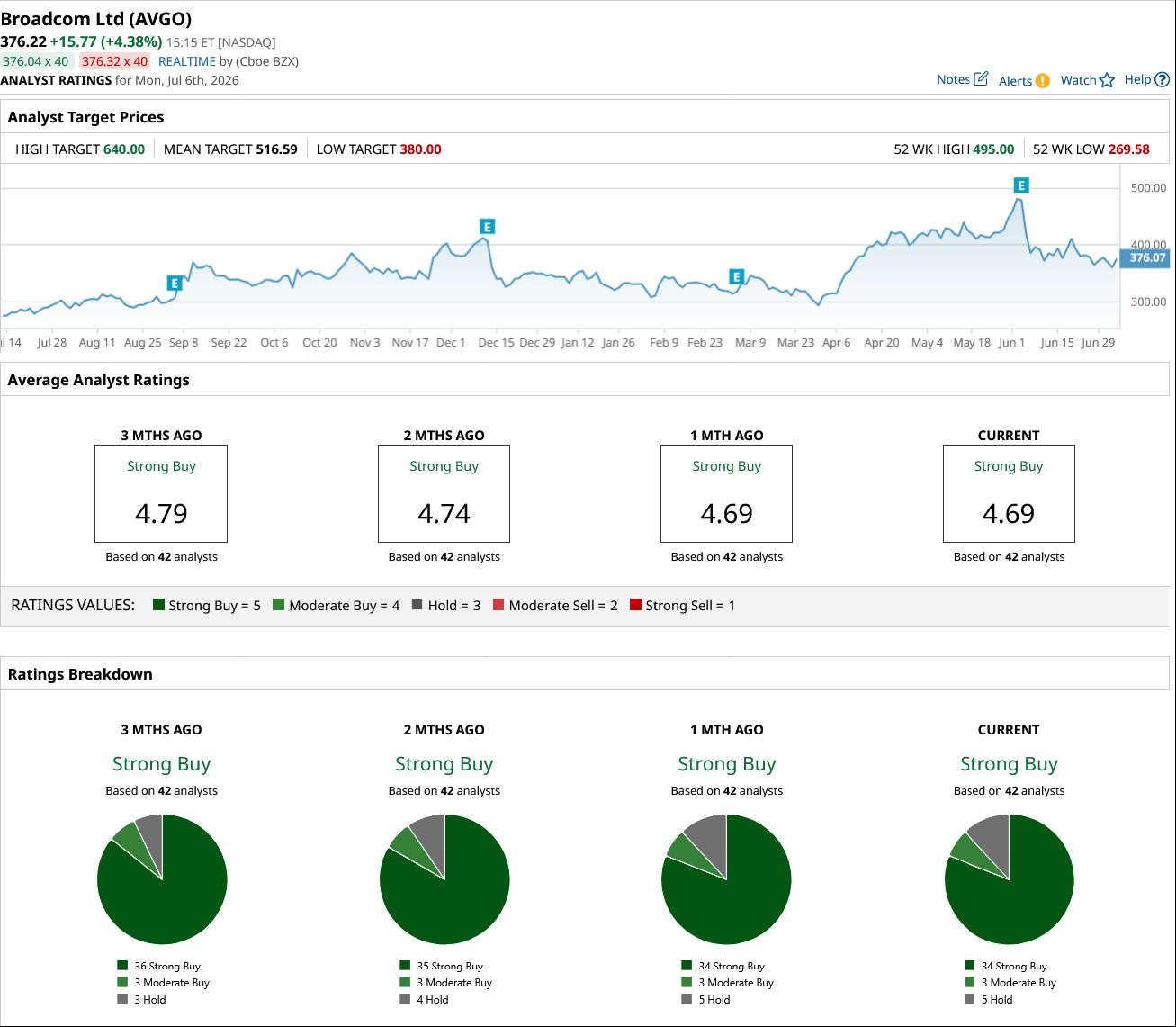

The average price target implies about a 37% upside from here for AVGO stock.

www.barchart.com

www.barchart.com On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

MSFT Stock Layoffs: What to Know as Microsoft Cuts Jobs in Xbox Unit Broadcom’s Largest AI Customer Is Fleeing to MediaTek. AVGO Stock Is Still a Buy. Here's Yet Another Reason Why Investors Should Be Bullish on Meta Platforms SpaceX Just Unveiled a New AI Growth Engine. What This Means for SPCX Stock.