The SpaceX (SPCX) IPO has reignited investors’ enthusiasm for the space industry. Amid this excitement, smaller players like Rocket Lab (RKLB) are attracting attention, with growing ambitions in rockets, satellites, and space systems. Until now, the company relied heavily on launch services and spacecraft manufacturing, businesses that can be cyclical and project-based, which left some investors skeptical about its long-term prospects. But now with its newly announced $8 billion acquisition of Iridium Communications (IRDM), one of the world's most established satellite communications companies, Rocket Lab’s growth story has taken a dramatic turn.

Rocket Lab shares have surged 38% year-to-date (YTD), while Iridium shares have surged an impressive 206% so far. Let’s take a closer look at why this deal makes RKLB stock a good buy now.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com The $8 Billion Deal That Changes Everything

On June 29, Rocket Lab announced that it is acquiring Iridium Communications in a cash-and-stock transaction totaling roughly $8 billion. According to the agreement, Iridium shareholders will receive $54 per share, a 24% premium over the company's pre-announcement share price. The deal is on track to close in mid-2027, assuming it clears shareholder and regulatory approvals. Iridium operates one of the world's most established low Earth orbit (LEO) satellite constellations, serving customers across government, defense, aviation, maritime, industrial IoT, emergency services, and commercial communications. The company also controls valuable global L-band spectrum, an increasingly scarce strategic asset.

Essentially, Rocket Lab generates revenue from launch services through its Electron rocket, space systems, including satellite manufacturing and components, and the development of its larger Neutron launch vehicle, a medium-lift rocket. In the first quarter, it generated $200 million in revenue, along with a backlog of $2.2 billion. Now, the Iridium acquisition will add a new growth pillar: global satellite communications with millions of paying customers and highly predictable recurring revenue. Analysts forecast Rocket Lab’s 2026 revenue to increase by 52% to $914 million, followed by another 41.7% in 2027. These numbers do not yet include the impact of the acquisition.

According to CEO Peter Beck, by “marrying Iridium's deep heritage, trusted infrastructure, and highly sought-after spectrum with Rocket Lab's extensive and proven launch and manufacturing capabilities,” the company will have the ability to “unlock entirely new markets.”

Rocket Lab's Stronger Competitive Position Against SpaceX

No company currently dominates commercial space like SpaceX. Its leadership spans launch services, reusable rockets, Starlink broadband, government missions, and human spaceflight. It’s quite challenging to replace SpaceX’s market position overnight but not impossible over time. Rocket Lab has been building its position step by step. Now with the Iridium acquisition, the case has become stronger. By combining launch vehicles, satellite manufacturing, spacecraft components, and a global communications network under one roof, Rocket Lab is building one of the most vertically integrated companies in the commercial space industry. This deal strengthens Rocket Lab's competitive position by bringing it closer to the model that has helped SpaceX dominate the commercial space industry.

In fact, Rocket Lab's upcoming Neutron, which was already viewed as one of the company's biggest long-term growth opportunities, would become even more valuable with this acquisition. The company can now use Neutron to launch its own future communications satellite, instead of relying on third-party launch providers. This will help lower deployment costs. According to Reuters, management even highlighted opportunities to expand Iridium's next-generation direct-to-device services and future satellite constellations using Rocket Lab's internal launch capabilities.

The Risks Investors Should Watch

No acquisition is risk-free even if it has strategic advantages. First, the transaction won’t close until it gains regulatory and shareholders' approval. Second, $8 billion is a massive deal, which will require significant financing. While the company has secured $3.6 billion in bridge financing from Deutsche Bank and Wells Fargo, integrating a business of Iridium’s size will be far more complex and time-taking.

Finally, Rocket Lab has been investing heavily in Neutron, which is a heavy burden on its balance sheet and cash flows over the next several years. If the deal closes and the integration is successful, the long-term rewards could be substantial. But in the short term, investors should be prepared to see some stock volatility.

Is RKLB Stock a Good Buy Now?

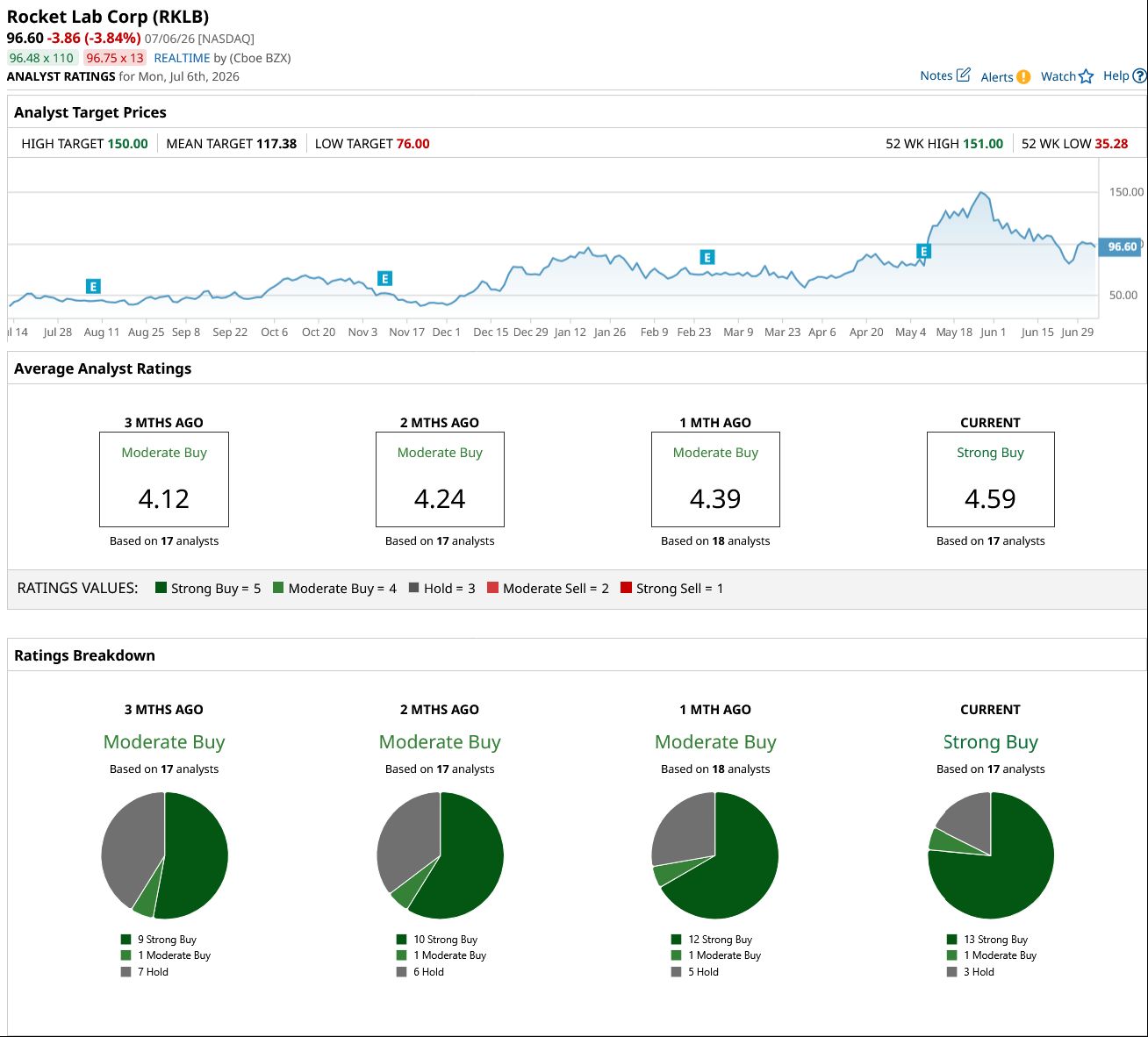

For long-term investors who believe the commercial space economy is still in its early stages, the Iridium acquisition makes Rocket Lab a far more compelling investment than it was just a few weeks ago. Overall, Wall Street rates RKLB stock a consensus “Strong Buy.” Of the 17 analysts covering the stock, 13 rate it as a “Strong Buy,” one has a “Moderate Buy,” and three analysts have a “Hold” rating. The average target price of $117.38 implies a potential upside of 22% from current levels, while the high target of $150 suggests a potential upside of 55% from here.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Rocket Lab Just Changed Its Growth Story With One Bold $8B Deal Amazon Ratio Spread Targets A Profit Zone Between 210 and 230 Nasdaq Futures Plunge as Samsung Sparks Chip Selloff The 3 Best Buy-and-Hold Dividend Stocks to Load Up on for Lifetime Income