Nvidia Corporation (NVDA) is seeking to reassure investors after reports that its next-generation Kyber rack-scale AI infrastructure could be delayed until 2028 triggered fresh concerns about the company’s aggressive product roadmap. While the speculation briefly raised questions over whether manufacturing challenges might slow Nvidia’s artificial intelligence (AI) dominance, the chipmaker quickly pushed back, stating that its roadmap remains intact.

Nvidia’s Kyber is the company’s next-generation rack-scale AI infrastructure designed for its Rubin Ultra platform, representing a major step beyond simply shipping faster GPUs. Instead of treating servers as standalone systems, Kyber integrates compute, networking, power delivery, and cooling into a unified AI infrastructure platform capable of linking massive GPU clusters with reduced latency.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Kyber is expected to debut alongside Rubin Ultra in 2027, according to Nvidia’s roadmap unveiled at GTC 2026, where it was positioned as the foundation for the company’s next-generation of AI supercomputers.

Given that Kyber is central to Nvidia’s vision of building ever-larger AI factories for hyperscalers, cloud providers, and enterprise customers, any delay would be closely watched as a potential headwind to the company’s long-term AI infrastructure roadmap.

About Nvidia Stock

Nvidia is a global leader in accelerated computing and AI, renowned for pioneering the GPU that revolutionized gaming, data centers, and AI-driven computing. Headquartered in Santa Clara, California, Nvidia’s technology now powers everything from high-performance gaming and cloud computing to autonomous vehicles and generative AI applications. With a market cap of $4.8 trillion, Nvidia stands among the world’s most valuable companies, driven by its dominance in AI infrastructure and continued innovation in next-generation chip design.

Nvidia has been one of the stock market’s biggest long-term winners, transforming from a gaming GPU maker into the dominant supplier of AI infrastructure. Fueled by explosive demand for AI accelerators and data center hardware, the stock has delivered extraordinary gains of 984.4% over the past five years, significantly outperforming the broader market and becoming one of the world’s most valuable companies. The company’s leadership in AI chips and strong relationships with hyperscale cloud providers have underpinned investors’ confidence in its long-term growth story.

However, Nvidia’s momentum has moderated in recent months. While the company’s fundamentals remain robust, the stock has lagged many semiconductor peers in 2026, gaining only 9.5% year-to-date (YTD). It is up 27.6% over the past year, underperforming the broader technology sector.

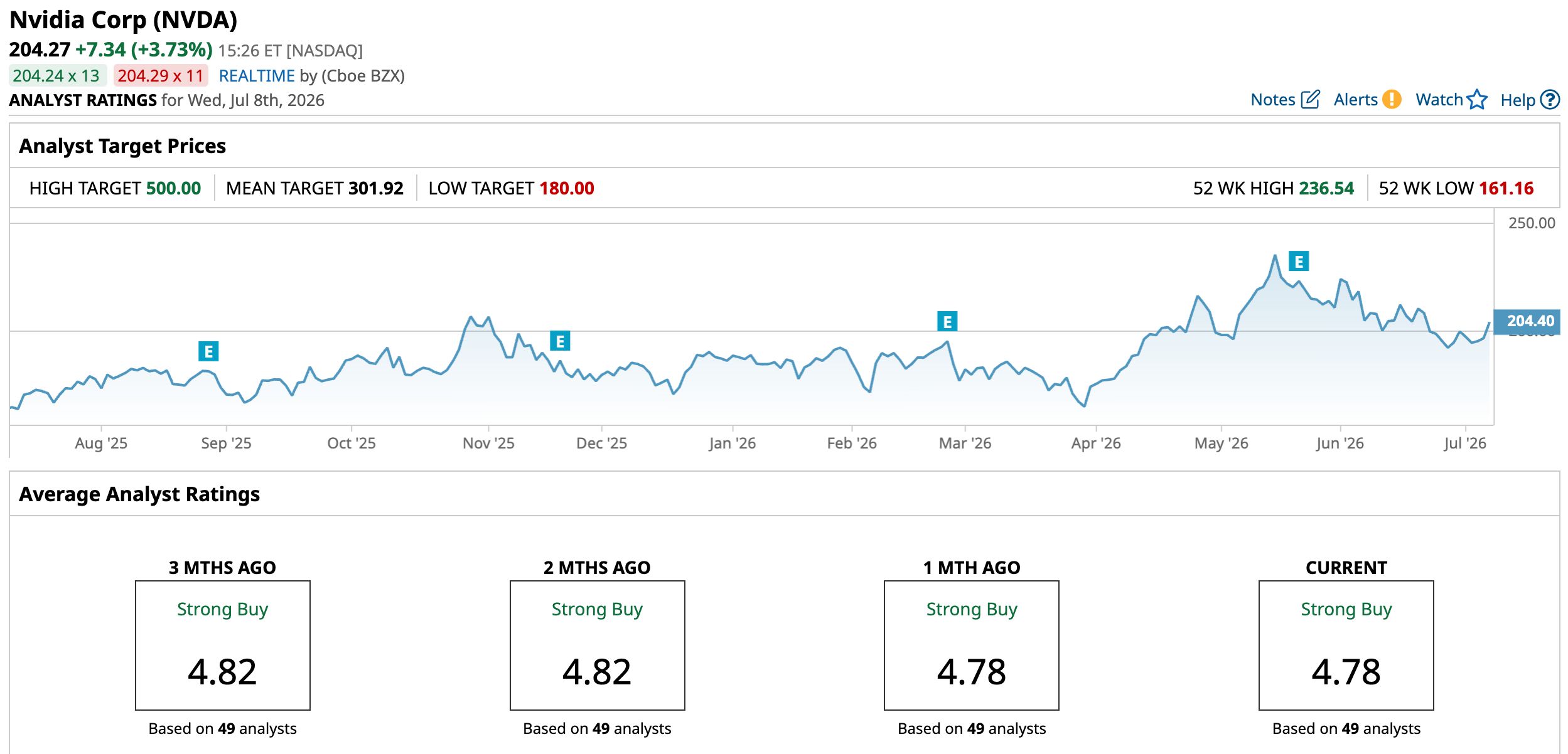

Shares have also experienced increased volatility and have declined 13.6% from its 52-week high of $236.54 reached on May 14, as concerns over AI spending sustainability, rising competition, export restrictions, and the timing of next-generation products such as Rubin and Kyber weighed on sentiment.

www.barchart.com

www.barchart.com Nvidia trades at 22.49 times forward earnings, which is currently a discount compared to industry peers and the historical average.

Robust Quarterly Performance

Nvidia delivered another blockbuster quarter with its most recent financial results for the first quarter of fiscal 2027 on May 20, reinforcing the company’s dominance in the rapidly expanding AI infrastructure market. Strong demand for AI accelerators, networking products, and next-generation Blackwell systems helped Nvidia post record revenue and earnings while continuing to outperform Wall Street expectations.

For the quarter ended April 26, Nvidia reported record revenue of $81.6 billion, up 85% year-over-year (YOY). Its net income surged 211% YOY to $58.3 billion. On a non-GAAP basis, earnings per share (EPS) increased 140% from the prior-year quarter to $1.87, ahead of expectations. Non-GAAP gross margin expanded sharply to 75%, compared to 60.8% in the same period last year, highlighting Nvidia’s continued pricing power and favorable AI product mix.

The Data Center business remained Nvidia’s primary growth engine. Data Center revenue climbed 92% YOY to a record $75.2 billion as hyperscalers, enterprises, and sovereign AI projects accelerated spending on AI factories and large-scale computing clusters. Nvidia also reported networking revenue of $14.8 billion, up 199% YOY. Meanwhile, Edge Computing revenue rose 29% YOY to $6.4 billion, supported by growth in gaming GPUs, autonomous driving platforms, robotics, and AI-enabled edge devices.

Management highlighted the rapid adoption of Blackwell systems and emphasized growing opportunities in agentic AI and enterprise AI infrastructure. CEO Jensen Huang described the current AI infrastructure buildout as “the largest infrastructure expansion in human history,” while also unveiling the new Vera Rubin platform and additional AI software and networking technologies aimed at expanding Nvidia’s ecosystem.

Furthermore, Nvidia provided extremely strong guidance for the second quarter of fiscal 2027. The company expects revenue of $91 billion, plus or minus 2%. Nvidia also guided for a non-GAAP gross margin of around 75%. Notably, management stated that the outlook assumes no contribution from China Data Center compute revenue, reflecting ongoing U.S. export restrictions.

Analysts tracking Nvidia project the company’s EPS to climb 90.2% YOY to $8.69 in fiscal 2027 and grow another 34.3% to $11.67 in fiscal 2028.

What Do Analysts Expect for Nvidia Stock?

Wall Street remains optimistic about Nvidia’s long-term prospects despite recent volatility. Last month, Morgan Stanley reaffirmed its “Overweight” rating on the stock and maintained its $288 price target, reiterating Nvidia as its top pick in the processor space.

Similarly, Truist Securities reiterated its “Buy” rating and $307 price target after Nvidia unveiled several next-generation AI products at GTC Taipei. The firm said the announcements reinforced its confidence in Nvidia’s technology leadership and strengthened the company’s position at the forefront of the rapidly expanding AI infrastructure market.

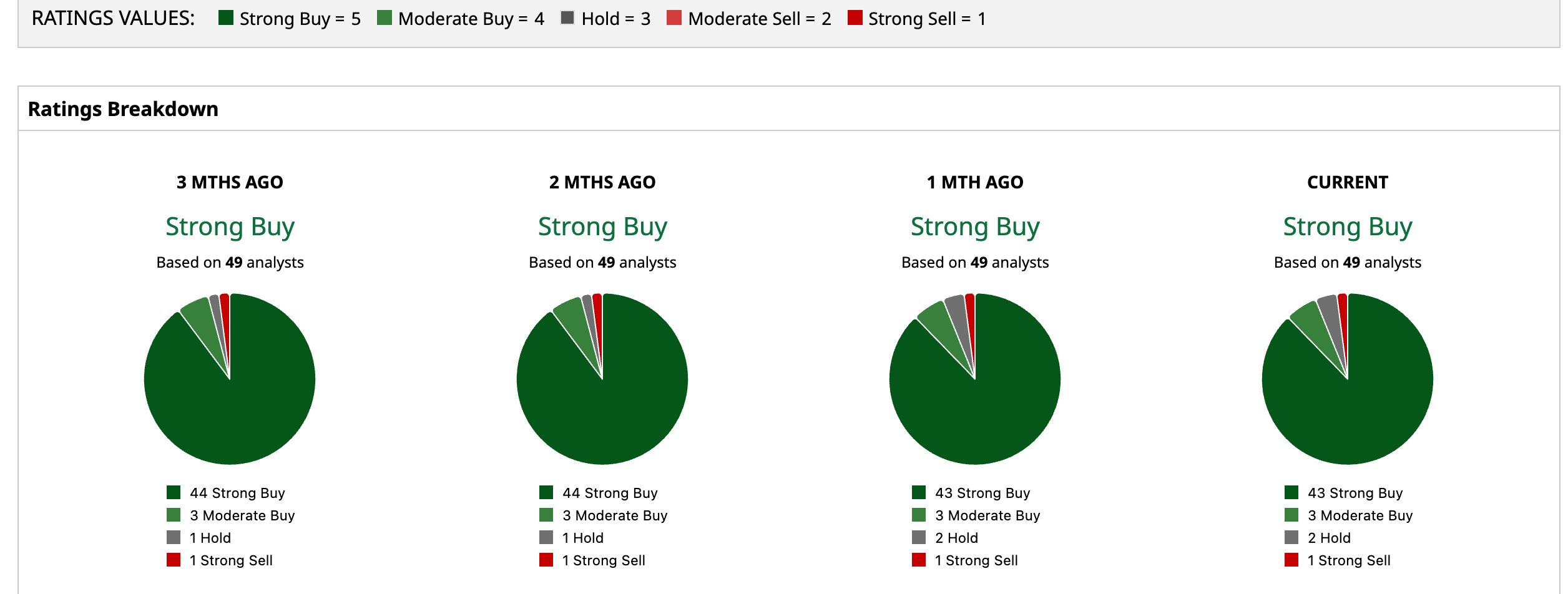

Wall Street’s bullishness is evident in NVDA having a consensus “Strong Buy” rating. Of the 49 analysts covering the stock, 43 advise a “Strong Buy,” three suggest a “Moderate Buy,” two analysts give it a “Hold” rating, and one offers a “Strong Sell” rating.

The average analyst price target for NVDA is $301.92, indicating a potential upside of 47.8%. Also, the Street-high target price of $500 suggests that the stock could rally as much as 144.8%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nvidia Says Kyber Is Still on Track. Why the Next-Gen Infrastructure Matters for NVDA Stock. Alibaba Shares Are Gaining on AI Optimism. Here's What to Know. NET Stock Alert: What to Know as Cloudflare Teams Up With OpenAI 2 Analysts Just Upgraded Dollar Tree Stock. Here's Why.