Clean energy solutions provider FuelCell Energy (FCEL) has priced an upsized underwritten public offering of 10.71 million shares of its common stock at a public offering price of $21 per share. The $225 million in gross proceeds is expected to fund capital expenditures as the company tries to expand its manufacturing capacity to power data centers. Although the rationale was to support future growth, the market did not take kindly to the news, as the stock dropped 13.2% intraday on July 8.

About FuelCell Energy Stock

FuelCell Energy designs and builds large-scale fuel cell systems that generate continuous, ultra-clean power. Based in Danbury, Connecticut, the company deploys molten carbonate fuel cell technology to serve utilities, data centers, industrial sites, and municipal clients. Its solutions provide on-site electricity using natural gas, biogas, or hydrogen, while capturing carbon emissions.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

In addition, FuelCell offers hydrogen production and long-duration energy storage through electrolysis platforms. With installations across North America, Europe, and Asia, the firm supports the global shift toward low-carbon energy infrastructure. The company has a market capitalization of $1.52 billion.

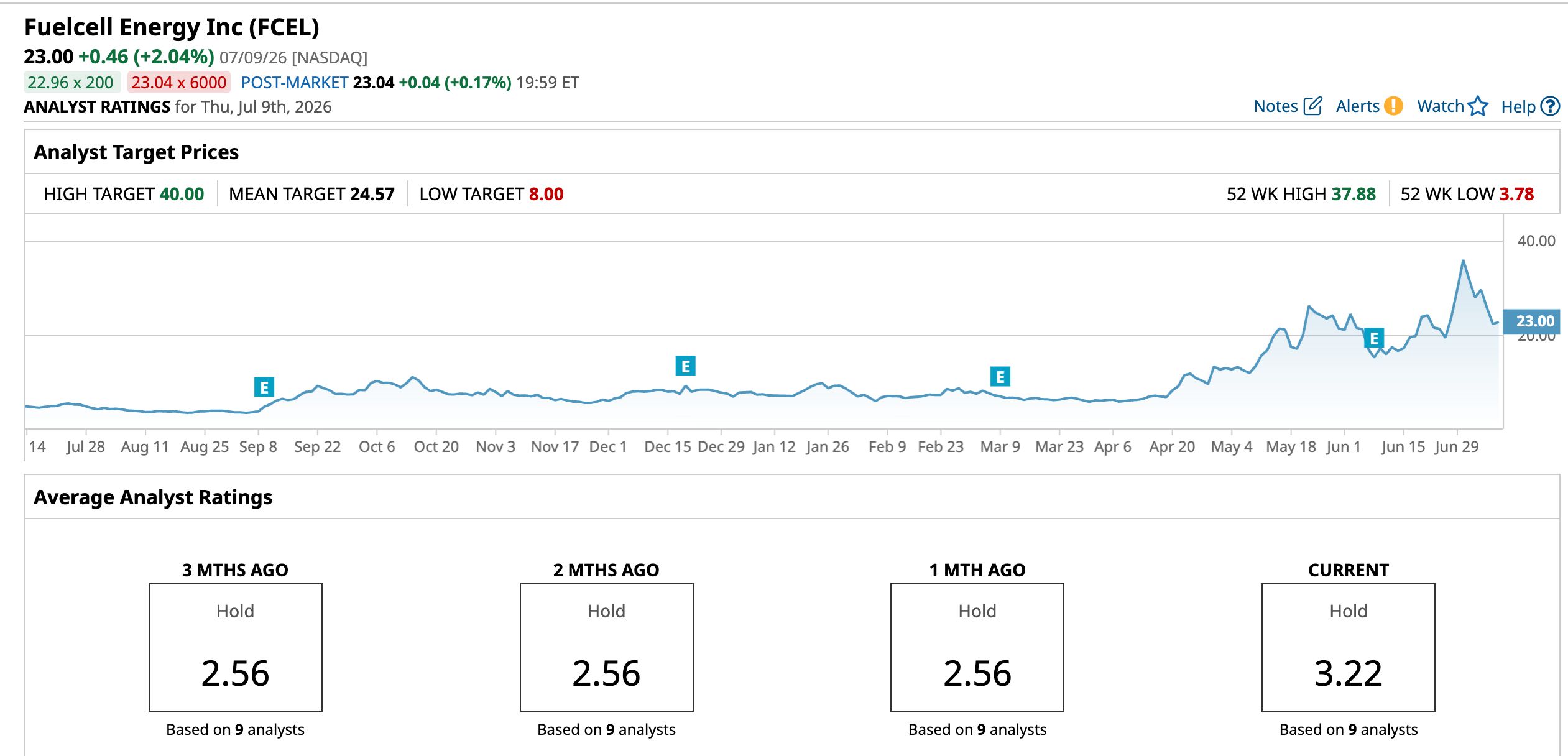

Driven by FuelCell’s strategic pivot to powering AI data centers. A key catalyst was a recent agreement with Fit Energy USA LP to supply up to 380 MW of clean, baseload on-site power for data centers, starting with an immediate 30 MW deployment. Over the past 52 weeks, FuelCell’s stock has gained a whopping 310.7%, while it is up 214.6% year-to-date (YTD). The company’s stock reached a 52-week high of $37.88 on June 30, but is down 39.3% from that level.

www.barchart.com

www.barchart.com On a forward-adjusted basis, FuelCell’s price-to-sales ratio of 9.83 times is significantly higher than the industry average of 1.86 times.

FuelCell Energy Reported Q2 Results Amid Strategic Push into Data Center Power

For the second quarter of fiscal 2026 (quarter ended April 30), FuelCell reported a 5% year-over-year (YOY) decrease in revenue to $35.59 million, below the $41.10 million expected by Wall Street analysts. The company’s backlog was also reduced by approximately 9.9% to $1.14 billion as of April 30. However, this reduction was primarily due to revenue recognized over the period from April 30, 2025 through April 30, 2026. FuelCell is still reporting losses. However, its adjusted net loss per share decreased from $1.53 in Q2 FY25 to $0.53 in Q2 FY26.

FuelCell’s operative expansion is well underway. The company is working on expanding the capacity of its Torrington manufacturing facility to support an annualized production rate of up to 500 MW. FuelCell estimates that the total cost of the expansion will range from $200 to $275 million, and the total cash and cash equivalents of approximately $441 million position the company well to achieve its goal.

Wall Street analysts expect FuelCell to reduce its bottom-line losses. For the current fiscal year, loss per share is projected to decrease 58.3% annually to $1.84, followed by a 15.2% improvement to a loss per share of $1.56 in the next fiscal year.

What Analysts Think About FuelCell’s Stock

Last month, analysts at B. Riley Securities upgraded FuelCell’s rating from “Neutral” to “Buy” and raised the price target from $13 to $32 after the company’s Fit Energy USA data center power deployment agreement.

Citing the same reason, analysts at Jefferies upgraded the stock from “Hold” to “Buy” and raised the price target from $16 to $24. At approximately $3,000/kW pre-ITC, it implies $90 million in near-term revenue, marking FuelCell’s first conversion of pipeline into backlog, per Jefferies analyst Julien Dumoulin Smith.

After the strategic agreement announcement, UBS analyst Manav Gupta more than tripled the price target for FuelCell to $22 from $7.25, while keeping a “Neutral” rating on the stock.

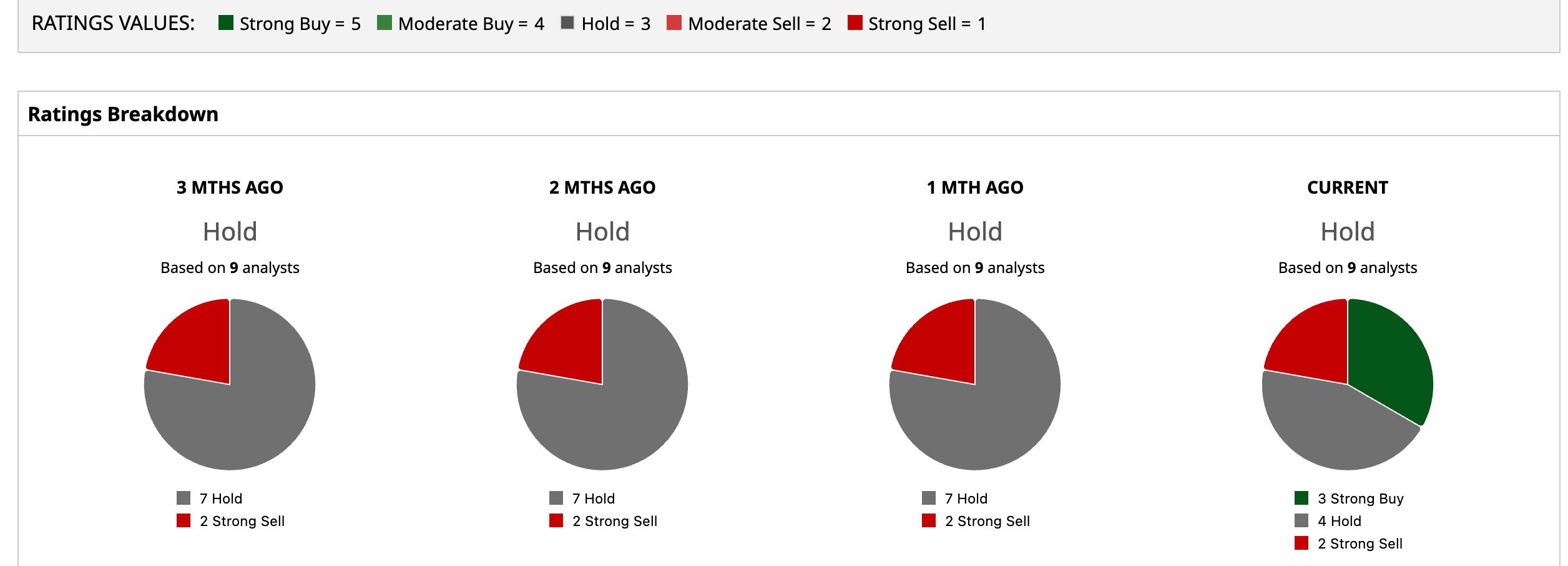

Wall Street analysts are taking a cautious stance on FuelCell’s stock now, with a consensus “Hold” rating overall. Of the nine analysts rating the stock, three analysts gave a “Strong Buy” rating, while four analysts are playing it safe with a “Hold” rating, and two analysts gave a “Strong Sell” rating. The consensus price target of $24.57 represents a 6.8% upside from current levels, while the Street-high price target of $40 implies a 73.9% upside.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A $225 Million Reason to Sell FuelCell Energy Stock Now Is it Time to Put Natural Gas on Your Radar? PLUG Stock Alert: Plug Power Just Scored a Major Green Hydrogen Win in Australia Beyond the War Premium: How Strategic Reserves Create a New Floor for Oil Prices