Leading financial services firm Wells Fargo has raised the price target on Western Digital (WDC), the pure-play hard disk drive (HDD) company. Highlighting strong demand visibility as the core rationale of its bullish thesis for the stock, the firm has raised its price target on the same to $730 from $575, while reiterating its “Overweight” rating. This implies a potential upside of about 31% from current levels.

The latest price target increase comes just about a month later, when on June 1, the firm had upped the price target to $575.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Western Digital

Founded in 1970, Western Digital is focused almost entirely on HDDs and related storage platforms following the Sandisk (SNDK) separation. Its primary products include high-capacity enterprise drives for cloud data centers, hyperscalers, and large-scale storage systems, as well as NAS, surveillance, and selected consumer HDDs.

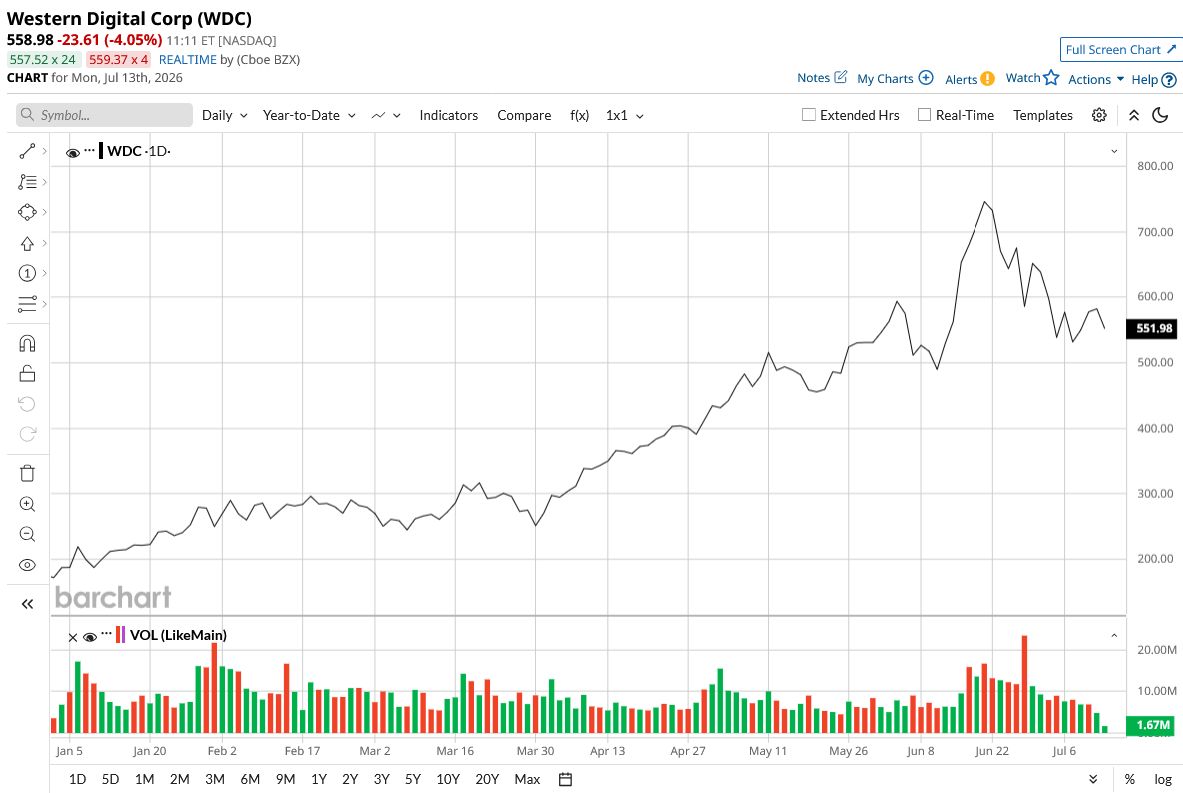

The company's market cap currently stands at $200.8 billion. Notably, WDC stock has jumped by 219% on a year-to-date (YTD) basis, while offering a modest dividend yield of 0.10%.

Having said that, is WDC still a “Buy” after such a searing rally and following Wells Fargo's vote of confidence? Let's find out.

www.barchart.com

www.barchart.com Dual Weapons to Drive Growth

My last analysis on Western Digital had harped on the virtues of HDD and why the company, being the market leader, is poised to benefit from the same. The stock is up more than 25% since then. Yet, in this piece, I want to delve more into specifics.

Western Digital has already sold out its entire HDD production for the year, with CEO Irving Tan confirming that the company had firm purchase orders from its top seven customers. It had also established long-term agreements with two customers for calendar 2027 and one for 2028, with those agreements covering both committed exabyte volumes and pricing.

The AI buildout is central to this fundamental strength in demand. However, Western Digital is not the market leader by chance, and its two proprietary technologies are its secret weapons.

First is ePMR, or energy-assisted perpendicular magnetic recording. Perpendicular magnetic recording is the conventional way drives have written data for years, standing the magnetic bits upright on the platter. What Western Digital does with ePMR is apply a small extra electrical bias to the write head that steadies and strengthens the magnetic field at the moment of writing. That cleaner, more controlled write lets tracks sit closer together without corrupting one another, which pushes areal density and capacity higher on a proven, reliable foundation.

The second differentiator is UltraSMR. Standard shingled magnetic recording overlaps data tracks like roof shingles, so more of them fit in the same space, but the trade-off is that writes must happen sequentially. UltraSMR takes that base and layers on a decade of proprietary work, blending 2D magnetic recording, advanced error correction, distributed sector coding, and OptiNAND, which stashes metadata in embedded flash. Together, these let WD encode data over much larger blocks with far more powerful error correction. The payoff is roughly a 10% capacity bump over plain SMR and about a 20% gain over conventional CMR. That is the edge Seagate cannot easily match, since OptiNAND draws on WD’s legacy flash integration.

Western Digital's Robust Q3

Western Digital posted strong financial results in the third quarter of 2026, delivering beats on both revenue and earnings.

Revenue climbed 45% year-over-year (YoY) to $3.34 billion. Gross margins reached the 50% level for the first time, coming in at 50.2% and representing a 1040 basis point improvement from 39.8% in the year-ago period. Earnings per share nearly doubled to $2.72, comfortably exceeding the consensus estimate of $2.40 and marking the fifth consecutive quarter of beating profit forecasts.

For the fourth quarter of 2026, the company guided for revenue of $3.65 billion and earnings per share of $3.25. This implies YoY growth of 39.8% and 95.6%, respectively. Both figures came in slightly below current analyst projections of $3.68 billion in revenue and $3.27 per share.

Net cash from operating activities rose to $1.1 billion from $508 million in the prior year quarter. Western Digital ended the period with $2.05 billion in cash and short-term debt of $1.58 billion on its balance sheet.

However, the recent share price appreciation has brought with it overvaluation for the stock. The forward P/E ratio of 58.55 times, P/S multiple of 15.60 times, and P/CF multiple of 63.24 times all sit above the respective sector medians by some distance.

Analyst Opinion on WDC Stock

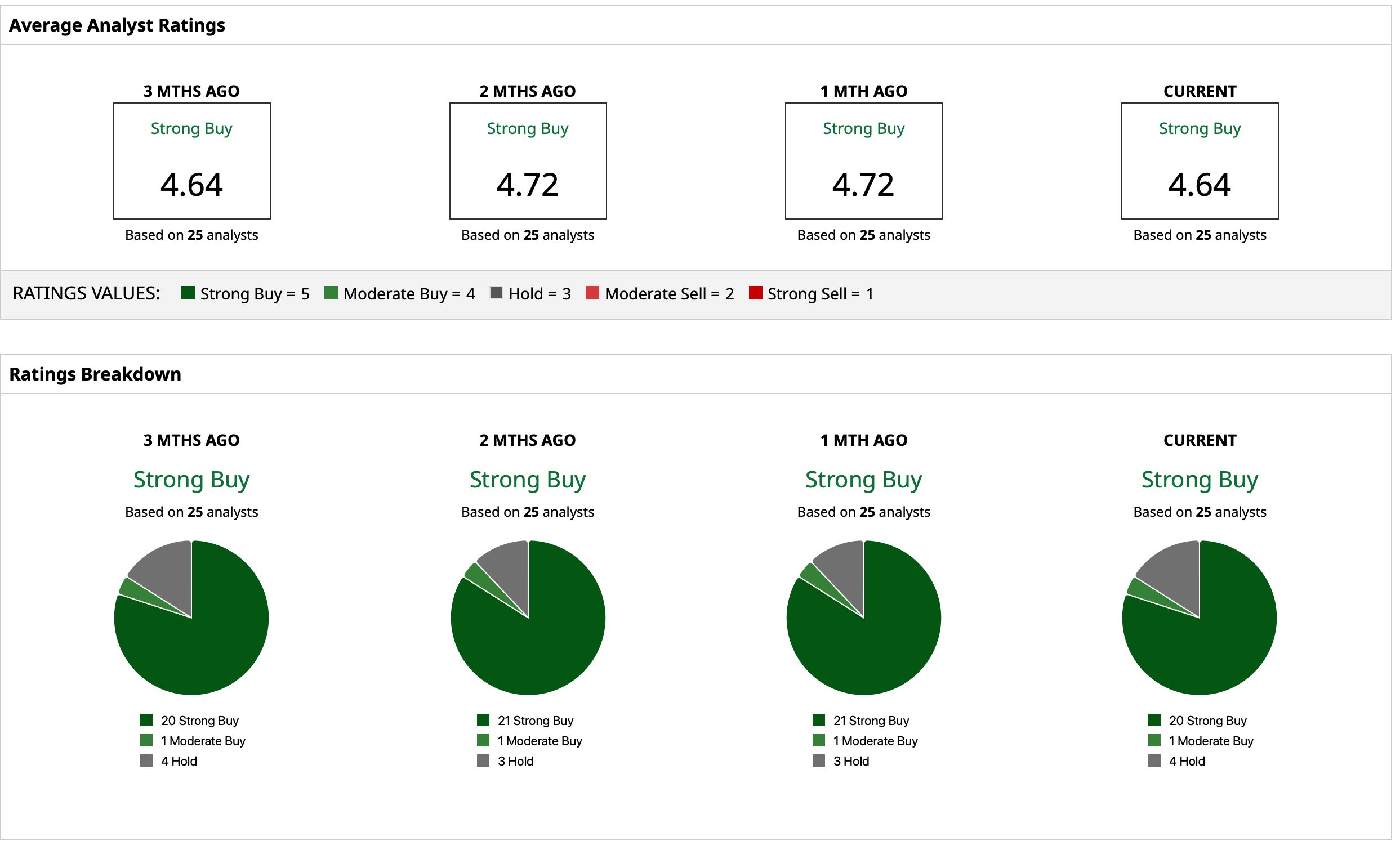

Considering this, analysts are optimistic about WDC stock, assigning to it a consensus “Strong Buy” rating. The mean target price is $620.61. Although this denotes only an upside of 11% from current levels, the Street high of $1,050 indicates an upside potential of about 88%. Out of 25 analysts covering the stock, 20 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and four have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Delta Air Lines Could Be a Top Stock to Buy for the Rest of 2026 Why Analysts Are Betting Western Digital Stock Can Gain Another 30% from Here COIN Stock Alert: 3 Reasons Why Coinbase Shares Are In Focus A New Report Says Meta Platforms Could Overtake Google AI. How to Play META Stock Here.