Cisco Systems CSCO is benefiting from strong demand for its networking and infrastructure solutions, which continue to support growth across the business. In the third quarter of fiscal 2026, revenues rose 12% year over year to a record $15.8 billion, while product revenues increased 17%. Networking remained the key growth driver, with revenues climbing 25% year over year to $8.8 billion on healthy demand across enterprise, cloud and service provider markets.

The company’s networking portfolio continues to gain traction. Networking product orders surged more than 50% in the third quarter of fiscal 2026, marking the seventh consecutive quarter of double-digit growth. The increase was fueled by triple-digit growth in service provider routing and compute, and strong double-digit growth in data center switching, campus switching, wireless, enterprise routing and industrial IoT.

Cisco is also seeing robust demand from hyperscale customers. Orders tied to its high-performance infrastructure offerings reached $1.9 billion in the quarter, up significantly from $600 million a year earlier. Year-to-date orders totaled $5.3 billion, exceeding the company’s previous full-year target. Strong adoption of Silicon One systems and Acacia optical solutions continues to contribute meaningfully to this momentum.

Enterprise customers are increasingly upgrading its technology environments, creating additional growth opportunities. Its data center switching orders increased more than 40% year over year, while campus networking orders rose more than 25% to a record level. Wireless orders climbed more than 40%, supported by growing adoption of WiFi 7 products and continued network modernization efforts. Demand for Cisco’s next-generation switching, routing and wireless products remained robust during the quarter. Customer adoption continued to exceed that of earlier product cycles, while WiFi 7 orders posted strong double-digit sequential growth and accounted for approximately half of the company’s wireless orders.

Cisco’s management is confident about further upside. The company expects to recognize approximately $4 billion in AI infrastructure revenues from hyperscalers in fiscal 2026 and at least $6 billion in fiscal 2027. Its innovation pipeline, strong customer demand and strategic investments in silicon, optics, security and AI position Cisco to capitalize on the multiyear, multibillion-dollar opportunity presented by the AI networking boom.

CSCO Faces Tough Competition in the Networking Domain

Cisco is facing stiff competition from Arista Networks ANET and HPE HPE. Both Arista Networks and HPE are expanding their footprint in the networking domain.

Arista Networks is a leader in high-speed Ethernet switching, particularly 100G, and is benefiting from rising demand for 800G and faster networking. Growth is driven by large data center expansions supporting distributed computing and cloud infrastructure. Its software stack, including EOS, CloudVision and AVD, simplifies network management. Customers include cloud providers, enterprises and telecom companies expanding across industries like manufacturing, insurance and telecom.

HPE’s focuses on artificial intelligence, industrial IoT and distributed computing as the next major growth markets. The company sees these areas as key drivers of future infrastructure demand. The acquisition of Juniper Networks has strengthened HPE’s position in networking, expanding its capabilities across AI, cloud and hybrid environments. This has helped improve its competitive position in large-scale modern infrastructure deployments.

CSCO Share Price Performance, Valuation & Estimates

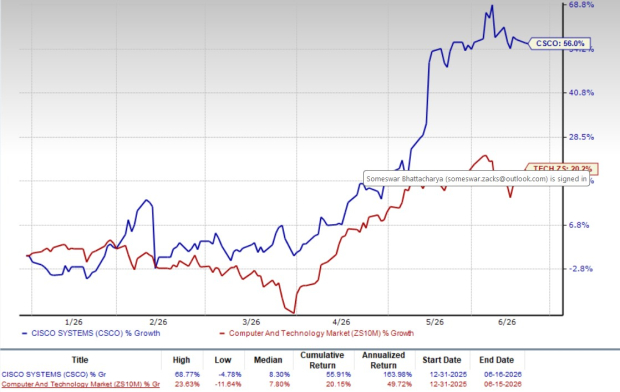

Cisco shares have gained 56% in the year-to-date period, outperforming the broader Zacks Computer and Technology sector’s return of 20.2%.

CSCO Stock Outperforms Sector

Image Source: Zacks Investment Research

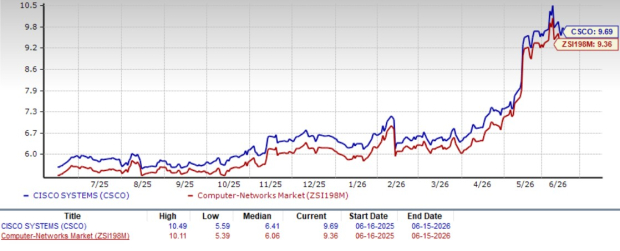

CSCO stock is trading at a premium, with a trailing 12-month price/book of 9.69X compared with the Zacks Computer Networking industry’s 9.36X. Cisco has a Value Score of F.

CSCO Stock Is Overvalued

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for fourth-quarter fiscal 2026 earnings is currently pegged at $1.17 per share, up 4 cents over the past 30 days, suggesting 18.18% growth from the figure reported in the year-ago quarter.

Cisco Systems, Inc. Price and Consensus

Cisco Systems, Inc. price-consensus-chart | Cisco Systems, Inc. Quote

Cisco currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Arista Networks, Inc. (ANET): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).