Keurig Dr Pepper KDP is well-positioned for growth, supported by its strong brand portfolio, continuous innovation and strategic initiatives. The company maintains a leading position in the single-serve coffee market, benefiting from a loyal consumer base, a broad portfolio of owned and licensed coffee brands and the recurring demand for K-Cup pods. Its expanding ecosystem of brewers and beverages continues to strengthen customer engagement and support long-term sales growth.

KDP remains focused on product innovation by introducing new brewers, premium coffee offerings and specialty beverages that cater to evolving consumer preferences. Keurig Dr Pepper is also leveraging strategic partnerships with leading coffee brands to expand consumer choice and reinforce the appeal of its brewing system. At the same time, the company is emphasizing premiumization, helping improve product mix and support higher margins.

The company’s growth reflects a strategic mix of innovation, brand activity and strong commercial execution, bolstered by its ongoing focus on cost efficiency, productivity and disciplined capital management. Strength in its brand portfolio and in-market execution, along with elasticity across most categories, has been aiding KDP’s revenues. In addition, Keurig Dr Pepper continues to invest in productivity initiatives, supply-chain optimization and cost-saving measures to enhance operational efficiency and offset inflationary pressures.

Continued strength in the Refreshment Beverages segment for a while has been aiding KDP’s overall performance. Robust sales and a favorable mix of products, along with contributions from Electrolit, have been bolstering the segment’s performance. The continuation of this trend has been bolstering the top line. KDP’s consumer-focused innovation model, household penetration and loyalty have been driving its market share across key categories like liquid refreshment beverages, K-Cup pods and brewers across its major markets.

The company is strengthening its omnichannel distribution capabilities while expanding its retail presence and selectively pursuing international growth opportunities. These strategic actions, combined with Keurig’s strong brand equity and leadership in the at-home coffee market, are expected to support sustainable revenue growth and profitability over the long term, despite ongoing macroeconomic and competitive challenges. Keurig continues to strengthen its portfolio with a clear focus on faster-growing categories, including energy, sports hydration and functional beverages. All the aforesaid factors will continue to ignite the momentum.

KDP’s Price Performance, Valuation and Estimates

Shares of Keurig have gained 15.7% in the past three months compared with the industry’s growth of 7.8%.

Image Source: Zacks Investment Research

From a valuation standpoint, KDP trades at a forward price-to-earnings ratio of 12.8X compared with the industry’s average of 19.09X.

Image Source: Zacks Investment Research

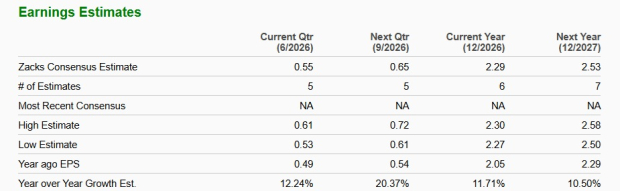

The Zacks Consensus Estimate for KDP’s 2026 and 2027 earnings per share (EPS) implies a year-over-year increase of 11.7% and 10.5%, respectively. The estimates for the aforesaid years have increased in the past 30 days.

Image Source: Zacks Investment Research

Keurig stock currently carries a Zacks Rank #3 (Hold).

Stocks to Consider in the Consumer Staples Space

The Chefs' Warehouse, Inc. CHEF, which is a distributor of specialty food products in the United States, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Chefs' Warehouse current financial-year sales indicates growth of 8.3% from the prior-year level. CHEF delivered a trailing four-quarter earnings surprise of 28.9%, on average.

Nomad Foods Limited NOMD, which manufactures and distributes frozen foods, currently carries a Zacks Rank #2 (Buy).

The consensus estimate for Nomad Foods’ current financial-year sales is expected to rise 0.5% from the year-ago reported figure. NOMD delivered a trailing four-quarter earnings surprise of 8.6%, on average.

Medifast, Inc. MED, which is a leading manufacturer and distributor of clinically-proven healthy living products and programs, currently carries a Zacks Rank of 2. MED delivered an average earnings surprise of 65.5% in the last reported quarter.

The Zacks Consensus Estimate for Medifast’s current financial-year sales indicates a decline of 26% from the year-ago number.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Chefs' Warehouse, Inc. (CHEF): Free Stock Analysis Report

MEDIFAST INC (MED): Free Stock Analysis Report

Nomad Foods Limited (NOMD): Free Stock Analysis Report

Keurig Dr Pepper, Inc (KDP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).