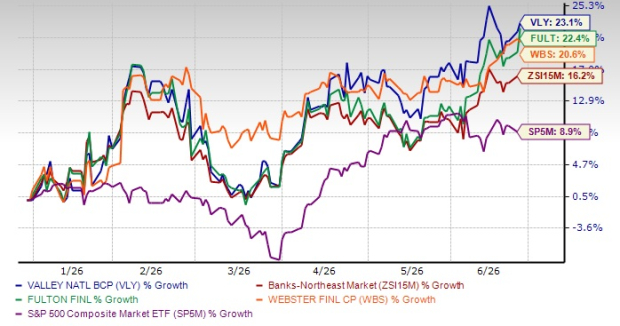

Supported by an impressive first-quarter 2026 performance, shares of Valley National Bancorp VLY have gained 23.1% so far this year, outperforming the industry’s 16.2% growth and the S&P 500 Index’s 8.9% rise.

The company witnessed an increase in net interest income (NII) in the March-end quarter for the fourth consecutive time (supported by growth in loan balances). Deposit costs declined, which helped sustain a net interest margin (NIM) of 3.17% (expanding 21 basis points year over year). Robust deposit growth, a reduction in higher-cost brokered funding, lower net charge-offs and better operating efficiency were other positives for the company.

If we compare VLY’s price performance with its peers, Fulton Financial Corporation FULT and Webster Financial Corporation WBS, it appears that VLY has performed better than both FULT and WBS. Year to date, the Webstar Financial stock has gained 20.6% and Fulton Financial has rallied 22.4%.

YTD Price Performance

Image Source: Zacks Investment Research

Now, let us see if the Valley National stock has more upside left despite recent strength in price. In order to understand this, we must dig deep into its fundamentals and growth prospects.

What’s Supporting the VLY Stock?

Robust Organic Growth: Valley National’s organic growth trajectory has been impressive. Its revenues have witnessed a compound annual growth rate (CAGR) of 9.2% over the last five years (2020-2025), supported primarily by a rise in loans (net loans also saw a CAGR of 9.2%). The uptrend for revenues and loans continued in the first quarter of 2026.

The company has also been making efforts to expand treasury management utilization, increase capital markets activity (including syndication, FX and swaps) and better integrate wealth management. These efforts are expected to drive fee income growth.

Supported by its efforts to bolster fee income, along with continued decent loan growth, VLY’s top line is expected to keep improving in the near term. Management projects NII to grow in the high end of 11-13% in 2026. Adjusted non-interest income is projected to rise 6-9% year over year in 2026.

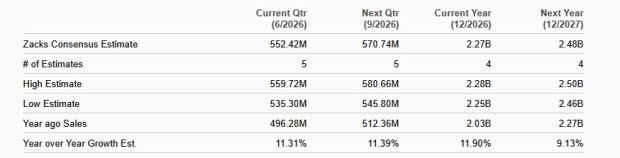

The Zacks Consensus Estimate for the company’s 2026 and 2027 revenues is pegged at $2.27 billion and $2.48 billion, which indicate year-over-year growth rates of 11.9% and 9.1%, respectively.

Revenue Growth Expectation

Image Source: Zacks Investment Research

Inorganic Expansion Initiatives: Given a solid balance sheet position, Valley National has been growing through acquisitions as well. In 2022, the company acquired Bank Leumi Le-Israel B.M.’s U.S. banking arm, while in 2021, it acquired Westchester Bank and Arizona-based advisory firm Dudley Ventures.

These and several past acquisitions are expected to be earnings accretive and help Valley National diversify revenues and footprint. Management is open to further buyouts if that “accelerates strategic initiatives.”

Improving Margins: Valley National’s NIM has been witnessing an uptrend over the past few years. While NIM on a tax-equivalent basis declined in 2023 and 2024 due to higher funding costs, the metric increased in 2020, 2021, 2022 and 2025, with the uptrend persisting in the first quarter of 2026.

Going forward, NIM growth is expected to continue, supported by stabilizing funding costs and loan growth. Management expects NIM expansion throughout 2026, driven by deposit repricing, and the replacement of higher-cost brokered funding and FHLB advances.

Impressive Capital Distributions: Supported by a robust balance sheet, Valley National announced a dividend for the first time in 2018. Since then, the company has maintained a quarterly dividend payment of 11 cents per share.

The company also has a share repurchase program in place. In February 2024, it announced a repurchase plan with an authorization of up to 25 million shares (which expired on April 26, 2026). In February 2026, the company once again authorized the buyback of up to 25 million shares, effective April 27, 2026, through April 27, 2028.

Given a strong capital position, the company is expected to keep boosting shareholder value through sustainable capital distribution activities.

What’s Hurting VLY’s Growth

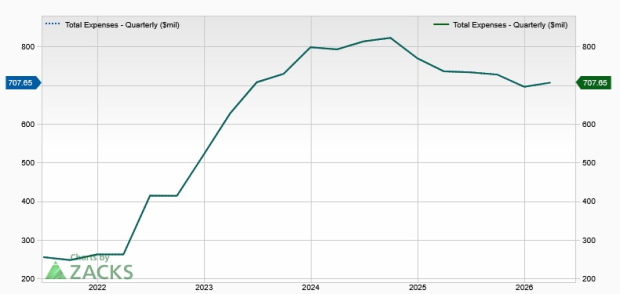

Elevated Expense Base: Over the last five years (2020-2025), the company’s expenses witnessed a CAGR of 12.1%, with the uptrend continuing in the first three months of 2026.

The rise has been mainly due to higher salary and employee benefits, and occupancy expenses. Valley National’s non-interest expenses are expected to remain elevated in the near term as the company continues to expand through acquisitions and invest in revenue growth areas.

Expense Trend

Image Source: Zacks Investment Research

Risky Loan Exposure: A major part of Valley National’s loan portfolio comprises commercial real estate (CRE) and residential mortgage loans. As of March 31, 2026, CRE loans accounted for 58.4% of total loans, while residential mortgages made up 11.5%.

Although the company built substantial reserves in 2024 to cushion against potential CRE-related stress and continues to tighten underwriting standards and limit exposure to non-owner-occupied and multi-family properties, the high concentration in CRE remains a key risk.

Any deterioration in economic conditions or weakness in the real estate market could pressure asset quality and weigh on Valley National’s financial performance.

How to Approach VLY Stock Now

Robust loan growth, inorganic expansion initiatives and efforts to bolster fee income (through steady investments) are expected to continue to aid VLY’s top line. Given a solid balance sheet and earnings strength, the company will be able to enhance shareholder value through efficient capital distributions.

However, analysts do not seem too optimistic regarding the company’s earnings growth prospects. The Zacks Consensus Estimate for VLY’s 2026 and 2027 earnings has been unchanged over the past 30 days.

Earnings Estimate Revision

Image Source: Zacks Investment Research

Also, high exposure to risky loan portfolios remains a major concern as it may put pressure on asset quality. Operating expenses are likely to stay elevated in the near term due to continued inorganic growth activities, thereby hurting the company’s bottom line.

Given the above-mentioned concerns, it does not seem a wise idea to invest in the VLY stock immediately.

However, those who already own the stock should hold on to it because, given its fundamental strength, the company is less likely to disappoint in the long term.

Currently, Valley National carries a Zacks Rank #3 (Hold). You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Webster Financial Corporation (WBS): Free Stock Analysis Report

Fulton Financial Corporation (FULT): Free Stock Analysis Report

Valley National Bancorp (VLY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).