Avanos Medical, Inc. AVNS is well-poised for growth in the coming quarters, courtesy of its impressive product line. The optimism, led by a strong performance in Specialty Nutrition Systems, supported by the Nexus Medical acquisition and the pending acquisition by American Industrial Partners, is expected to contribute further. However, margin challenges, tariff risks and weakness in Pain Management & Recovery business continue to weigh on performance.

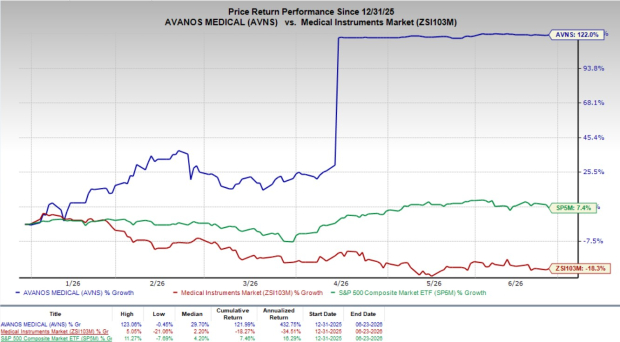

In the year-to-date period, this Zacks Rank #3 (Hold) stock climbed 122%, outperforming the industry’s 18.3% decline and the S&P 500’s 7.4% rise.

The renowned medical device solutions provider has a market capitalization of $1.17 billion. Avanos Medical’s earnings yield of 4.3% compares favorably with the industry’s negative yield being 3.5%.

Image Source: Zacks Investment Research

Factors Favoring AVNS’ Growth

Robust Performance in Specialty Nutrition: A key factor favoring Avanos Medical's growth is the continued momentum within its Specialty Nutrition Systems (SNS) segment, which delivered double-digit organic revenue growth in the first quarter of fiscal 2026. This segment is driven by high demand for enteral feeding and neonate solutions, with the company's flagship MIC-KEY tube remaining a dominant market offering. The integration of Nexus Medical has exceeded expectations, positioning the company for further double-digit growth in the neonatal space by leveraging established NICU sales channels.

Strategic Portfolio Optimization and M&A: Avanos Medical has aggressively reshaped its portfolio by divesting underperforming, low-margin assets to focus on its most profitable core competencies. Significant moves include the planned exit from the IV therapy segment in fiscal 2026 and the strategic divestiture of the hyaluronic acid business. These actions, coupled with the pending $1.27 billion acquisition by American Industrial Partners (AIP), are expected to provide the company with enhanced resources and operational expertise to accelerate its innovation roadmap and pursue more accretive M&A opportunities.

Global Expansion and Operational Efficiencies: Avanos Medical is expanding its international footprint, supported by favorable reimbursement trends in major markets such as the U.K. and Japan. Furthermore, the company is executing a strategic exit from its China-based manufacturing to mitigate long-term tariff exposure, a move projected to bolster margins starting in the second half of fiscal 2026. By focusing on cost containment and implementing guided-placement technologies like CORTRAK, management aims to drive higher procedure volumes and reach a long-term goal of $1 billion in revenues by fiscal 2030.

Factors That May Offset the Gains for AVNS

Persistent Tariff and Margin Pressures: Avanos Medical continues to face tariff-related challenges, which are expected to remain a headwind in fiscal 2026. The company guided to $30 million in tariff-related costs, a $12 million increase from fiscal 2025, with a significant portion tied to neonatal products sourced from China. While management is actively implementing mitigation strategies — including pricing actions, cost controls and supply chain adjustments — these measures will take time to fully offset the impact.

A key initiative is the exit from China-based syringe manufacturing by mid-2026, but until this transition is completed, tariff pressures are expected to weigh on profitability. Management indicated that gross margin improvement will be delayed, with a pause in fiscal 2026 before improvement begins in the second half and into fiscal 2027.

Weakness in PM&R and Uneven Business Performance: While the SNS segment continues to deliver strong growth, other parts of the business remain under pressure. The Pain Management & Recovery (PM&R) segment reported flat revenues in the first quarter of fiscal 2026 and posted an operating loss of $1.8 million, compared with a profit in the prior-year period. Lower procedure volumes weighed on surgical pain and recovery sales. This uneven performance across business segments could limit the company's overall growth momentum.

Portfolio Restructuring and Execution Risks: Avanos Medical is undergoing a broad portfolio transformation that carries execution risks. The company is exiting its IV therapy business, restructuring GAME READY and has already divested its hyaluronic acid business. While these actions are intended to improve long-term profitability and strategic focus, they may reduce near-term revenue contributions and create operational disruptions. Successful integration of acquisitions such as Nexus Medical will be critical to realizing expected growth and profitability benefits.

AVANOS MEDICAL, INC. Price

AVANOS MEDICAL, INC. price | AVANOS MEDICAL, INC. Quote

Estimate Trend

Avanos Medical is witnessing a negative estimate revision trend for fiscal 2026. In the past 60 days, the Zacks Consensus Estimate for earnings has moved 0.9% south to $1.06 per share.

The Zacks Consensus Estimate for the company’s second-quarter fiscal 2026 revenues is pegged at $173.5 million, indicating a 0.8% decline from the year-ago quarter’s reported number. The earnings estimate of 22 cents per share implies 29.4% year-over-year growth.

Stocks to Consider

Some better-ranked stocks in the broader medical space that have announced quarterly results are BrightSpring Health BTSG, Globus Medical GMED and Intuitive Surgical ISRG.

BrightSpring Health, currently sporting a Zacks Rank #1 (Strong Buy), reported first-quarter 2026 adjusted earnings per share (EPS) of 39 cents, which beat the Zacks Consensus Estimate by 34.5%. Revenues of $3.61 billion surpassed the Zacks Consensus Estimate by 8.35%. You can see the complete list of today’s Zacks #1 Rank stocks here.

BrightSpring Health has an estimated long-term earnings growth rate of 46.5%. BTSG’s earnings surpassed estimates in three of the trailing four quarters and missed once, the average surprise being 14.6%.

Globus Medical, currently carrying a Zacks Rank #2 (Buy), reported a first-quarter 2026 adjusted EPS of $1.12, which surpassed the Zacks Consensus Estimate by 22.1%. Revenues of $759.9 million beat the Zacks Consensus Estimate by 4.0%.

GMED has an estimated long-term earnings growth rate of 10.2%. The company’s earnings beat estimates in each of the trailing four quarters, the average surprise being 26.3%.

Intuitive Surgical, carrying a Zacks Rank #2 at present, reported first-quarter 2026 adjusted EPS of $2.50, which beat the Zacks Consensus Estimate by 20.2%. Revenues of $2.77 billion surpassed the Zacks Consensus Estimate by 6.2%.

Intuitive Surgical has a long-term estimated growth rate of 14.3%. ISRG’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 16.8%.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

AVANOS MEDICAL, INC. (AVNS): Free Stock Analysis Report

BrightSpring Health Services, Inc. (BTSG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).