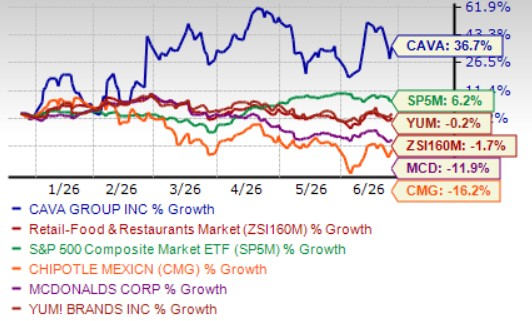

Shares of CAVA Group, Inc. CAVA have gained 36.7% in the past six months against the Zacks Retail - Restaurants industry’s decline of 1.7%. Over the same timeframe, the stock has also outperformed the S&P 500’s rise of 6.2%.

Much of this outperformance can be attributed to CAVA’s strong execution and resilient consumer demand amid a challenging industry backdrop. The stock has been well received on account of robust traffic growth, sustained same-restaurant sales momentum, disciplined pricing and healthy new restaurant productivity across both existing and newer markets. An improved 2026 outlook, coupled with broad-based strength across geographies and income cohorts, improved loyalty-driven frequency, stronger digital order execution and continued brand-awareness gains, likely further reinforced investor confidence.

The impressive run has sparked interest among investors, especially as CAVA pulls ahead of major industry players like Chipotle Mexican Grill, Inc. CMG, McDonald's Corporation MCD and Yum! Brands, Inc. YUM.

CAVA, CMG, MCD & YUM 6-Month Price Performance

Image Source: Zacks Investment Research

After CAVA’s 26% climb, investors face a more balanced decision: whether the rally still has room to run or whether patience is warranted at current levels. Let’s examine the company’s core growth drivers and emerging risks to determine the right course of action.

What’s Driving CAVA’s Stock Growth?

CAVA’s recent stock momentum reflects steady operating execution, resilient customer demand and growing confidence in the company’s long-term restaurant expansion story. The company is benefiting from healthy traffic trends, strong guest engagement and a differentiated Mediterranean platform built around health, taste, value and warm hospitality.

CAVA’s expansion strategy remains a central pillar of its growth narrative. The company continues to scale across new and existing markets while maintaining strong new restaurant productivity. CAVA stated that recent openings are performing in line with or ahead of prior strong cohorts, reinforcing confidence in the brand’s portability and long-term white-space opportunity.

The company is also deepening customer engagement through loyalty, digital channels and targeted marketing activations. With digital sales nearing 40% of the mix and loyalty participation supporting higher frequency, CAVA is developing a broader first-party relationship with guests. Its marketing efforts around cultural moments and athlete collaborations are further enhancing brand relevance and engagement.

Menu innovation is adding another layer to CAVA’s growth story. In the fiscal first quarter, the company highlighted the return of the roasted white sweet potato as a seasonal item and reported strong feedback and higher visit frequency, including from guests new to the brand. CAVA also launched its first seafood offering — Pomegranate-Glazed Salmon — across all restaurants nationwide, positioning it as a natural extension of the Mediterranean menu that broadens choice while staying true to the concept. Looking ahead, CAVA expects to sustain a steady cadence of innovation that supports traffic and mix without relying on broad discounting.

The company raised full-year 2026 guidance to 4.5%-6.5% same-restaurant sales growth (up from the prior expectation of 3%-5%) and $181-$191 million of Adjusted EBITDA (up from $176-$184 million). The company also noted that second-quarter trends are tracking in line with the first quarter and above the revised full-year range, while still embedding moderation later in the year.

What May Pull Back CAVA Stock?

Despite CAVA’s strong operating momentum, margin pressure remains an important watch point. The company expects the national rollout of Pomegranate-Glazed Salmon to create an approximately 100-basis-point restaurant-level margin-rate headwind. The outlook also incorporates a 20- to 40-basis-point headwind from elevated energy costs, including potential fuel surcharges, utilities and packaging-related inputs. Wage investments and a higher mix of third-party delivery may further limit near-term margin expansion.

Comparable sales growth is also expected to normalize from the fiscal first-quarter level. CAVA delivered 9.7% same-restaurant sales growth in first-quarter fiscal 2026, supported by 6.8% traffic growth, but its full-year outlook calls for a more moderate 4.5%-6.5% increase. While fiscal second-quarter trends were tracking in line with the first quarter at the time of the call, the full-year guidance assumes a slower pace for the balance of the year.

CAVA’s rapid development pace also requires disciplined execution. The company raised its fiscal 2026 opening outlook to 75-77 net new restaurants, while preopening costs are expected to rise as more units remain under construction and general managers are onboarded earlier for training. This investment supports long-term scalability, but it also raises the importance of operator readiness, labor depth and consistent restaurant execution. Any pressure on new restaurant productivity, opening cadence or service consistency could temper investor confidence in CAVA’s expansion-driven growth thesis.

CAVA’s Valuation: A Bargain or a Risk?

CAVA is trading at a premium to the industry, with a forward 12-month price-to-sales (P/S) multiple of 5.88, well above the industry average of 3.30. Other industry players, such as CMG, MCD and YUM, have P/S ratios of 2.99, 6.66 and 4.54, respectively.

CAVA’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

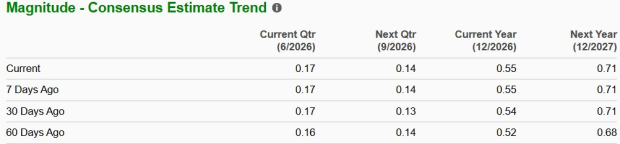

Over the past 60 days, the Zacks Consensus Estimate for CAVA’s fiscal 2026 earnings per share has increased from 52 cents to 55 cents. Over the same period, estimates for YUM have increased 1.1%, while the estimates for CMG and MCD have declined 0.9% and 2.1%, respectively.

CAVA Earnings Estimate Trend

Image Source: Zacks Investment Research

How to Play CAVA Stock?

CAVA’s long-term growth story remains intact, supported by traffic-led same-restaurant sales growth, strong new restaurant productivity, disciplined pricing and a sizable runway for unit expansion. The company’s digital mix, loyalty engagement, menu innovation and improving brand awareness further support customer frequency and broaden its growth opportunities.

However, near-term headwinds could limit additional upside after the stock’s sharp six-month rally. The salmon rollout, elevated energy costs, wage investments and a higher third-party delivery mix may pressure margins, while full-year same-restaurant sales growth is expected to moderate from the first-quarter pace. At a premium valuation, much of the optimism surrounding CAVA’s expansion strategy and traffic momentum appears to be reflected in the stock.

Given this setup, investors may prefer to hold steady rather than chase the recent rally. Existing shareholders can remain invested to benefit from CAVA’s long-term growth runway, while prospective investors may wait for a more attractive entry point.

CAVA currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CAVA Group, Inc. (CAVA): Free Stock Analysis Report

McDonald's Corporation (MCD): Free Stock Analysis Report

Yum! Brands, Inc. (YUM): Free Stock Analysis Report

Chipotle Mexican Grill, Inc. (CMG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).