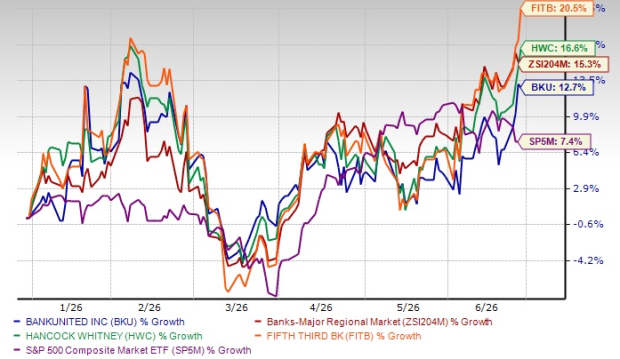

Shares of BankUnited Inc. BKU have gained 12.7% so far this year, outperforming the S&P 500 Index’s 7.4% growth. Investors have rewarded the bank’s improving deposit franchise, expanding net interest margin (NIM), better credit quality, continued commercial banking growth and disciplined capital management. Also, improving sentiment toward the overall regional banking sector (given easing funding pressure and stronger loan demand) has aided the BKU stock so far this year.

The industry to which BKU belongs has gained 15.3%. If we compare its price performance with its peers like Fifth Third Bancorp FITB and Hancock Whitney Corporation HWC, it appears that BKU has underperformed both.

So far in 2026, shares of Fifth Third Bancorp and Hancock Whitney have gained 20.5% and 16.6%, respectively.

YTD Price Performance

Image Source: Zacks Investment Research

Now, let us see if the BankUnited stock has more upside left despite recent strength in price. In order to understand this, we must dig deeper into its fundamentals and growth prospects.

Key Strengths of BankUnited

Revenue Growth: BankUnited has been witnessing robust top-line growth over the past several years (its revenues saw a compound annual growth rate of 4.3% over the five years ended 2025, with the uptrend continuing in the first quarter of 2026), supported by solid loan and deposit growth (net loans witnessed a CAGR of almost 1% amid continued run-off in residential and other loans, while core loans moved steadily higher).

Management’s efforts to increase low-cost deposits (targeting NIDDA to reach 34% of total deposits) have also been supporting top-line growth. As of March 31, 2026, non-interest-bearing demand deposits constituted 30.5% of total deposits.

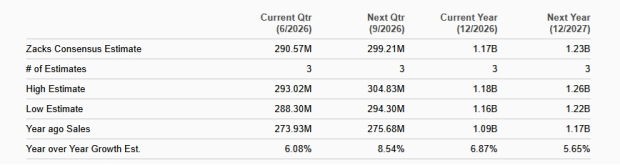

Supported by continued loan growth and growth in the company’s NIDDA, along with its efforts to strengthen fee income, total revenues are anticipated to keep improving in the quarters ahead. Management anticipates net interest income to grow 9% year over year in 2026, while non-interest income is projected to increase 6%, driven by organic growth in the company’s core commercial businesses, led by deposits/payment products. Total revenues are anticipated to rise 8%.

The Zacks Consensus Estimate for BKU’s 2026 and 2027 revenues is pegged at $1.17 billion and $1.23 billion, which indicates year-over-year growth rates of 6.9% and 5.7%, respectively.

Revenue Growth Expectation

Image Source: Zacks Investment Research

Improving Margins: BankUnited has been witnessing a rise in NIM on the back of declining funding costs and higher loan yields. The metric expanded to 2.95% in 2025 from 2.73% in 2024, 2.56% in 2023 and 2.68% in 2022. In first-quarter 2026, NIM expanded 18 basis points year over year to 2.99%.

The company’s modestly asset-sensitive balance sheet, robust loan demand and stabilizing funding costs will continue to provide support as the Federal Reserve turns slightly hawkish. We project NIM (fully tax equivalent or FTE) to be 3.11%, 3.22% and 3.30% in 2026, 2027 and 2028, respectively.

Management expects NIM to touch 3.20% by the end of fourth-quarter 2026.

Impressive Capital Distributions: BankUnited has an impressive capital distribution plan. Since 2022, it has been increasing its dividend payouts annually, with the latest hike announced in March 2026.

Also, it has a share repurchase program in place. In January 2026, the company increased the share buyback authorization by $200 million, with no expiration date. This, along with the previous plan, expands the repurchase program to $250 million. As of March 31, 2026, $195.9 million worth of authorization remained available.

The company's earnings strength is expected to help it sustain enhanced capital distribution activities, through which it will keep enhancing shareholder value.

What’s Hurting BKU’s Growth?

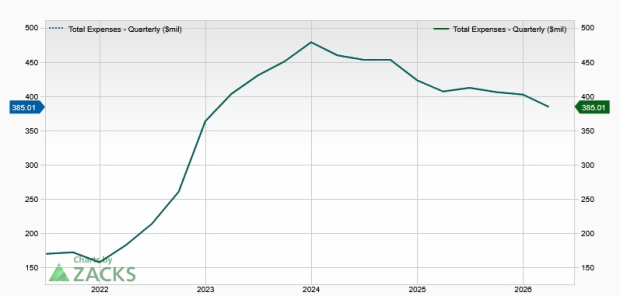

Elevated Expense Base: BankUnited’s expenses have witnessed a five-year (2020-2025) CAGR of 7.7%, with the uptrend persisting in the first three months of 2026. This increase was due to higher employee compensation and benefits costs, and technology expenses.

Expense Trend

Image Source: Zacks Investment Research

Overall costs are likely to remain elevated due to continued hiring, investments in technological upgrades and inflation. Management expects non-interest expenses to increase 4% this year.

Weak Asset Quality: BankUnited’s asset quality has been deteriorating over the past few years. While the company recorded negative provisions in 2021, the metric witnessed a CAGR of 40.3% over the six years ended 2025. Net charge-offs saw a CAGR of 26.4% over the same time frame. Both metrics increased in the first quarter of 2026 as well.

Due to a challenging operating backdrop and persistent inflation, the company’s asset quality is expected to remain under pressure.

Here’s How to Approach BKU Stock Now

BankUnited remains well-positioned for top-line growth, given its improving deposit mix, along with solid loan demand. The company’s NIM is expected to be positively impacted in the near term, supported by loan growth and stabilizing funding costs.

While increasing expenses and deteriorating credit quality are concerning, analysts have an optimistic stance regarding BKU’s earnings growth prospects. The Zacks Consensus Estimate for the company’s 2026 and 2027 earnings has been revised upward over the past 60 days. The 2026 estimate suggests year-over-year growth of 16.5% and the 2027 estimate indicates growth of 13.1%.

Earnings Estimate Revision

Image Source: Zacks Investment Research

It seems to be a wise idea to add the BankUnited stock to your portfolio now, given the company’s fundamental strength, and solid earnings and revenue growth expectations.

Currently, BKU sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today's Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BankUnited, Inc. (BKU): Free Stock Analysis Report

Fifth Third Bancorp (FITB): Free Stock Analysis Report

Hancock Whitney Corporation (HWC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).