Pitney Bowes Inc. PBI entered 2026 with a sharper focus on cash generation, balance-sheet flexibility and operational discipline. Its first-quarter results showed meaningful progress, with operating cash flow and free cash flow turning sharply positive after year-ago outflows. For investors, the key question is whether this cash flow surge reflects a sustainable improvement in the business or a temporary benefit from working-capital timing.

The company generated $44.2 million in operating cash flow compared with an outflow of $16.7 million in the year-ago period, while free cash flow improved to $43.5 million from a negative $20.5 million. Supported by the stronger start to the year, Pitney Bowes reaffirmed its recently upgraded 2026 guidance, including free cash flow of $345-$380 million. For a company whose turnaround increasingly depends on financial flexibility rather than top-line growth alone, improving cash generation has become one of the most important measures of progress.

The improvement reflects more than favorable timing. During the earnings call, management pointed to stronger working-capital management, improving profitability, disciplined cost control and better operational execution across the business. The company noted that working-capital performance exceeded internal expectations during the quarter, providing a meaningful boost to operating cash flow. At the same time, adjusted EBIT increased 9% year over year to $130 million despite a 3% decline in revenues, while tighter expense management helped expand adjusted EBIT margin to 27.3% from 24.3% a year earlier. These results suggest that Pitney Bowes is becoming a more efficient business capable of converting a larger share of earnings into cash.

The key question is whether this momentum is sustainable. Management believes the business is becoming structurally stronger, with SendTech stabilizing and continued growth in digital shipping, software and Pitney Bowes Bank. Stronger cash generation has also enhanced capital allocation flexibility, enabling the company to repurchase 12.9 million shares for $136 million in the first quarter, bringing year-to-date repurchases to $186 million through May 1. The board also approved its fifth dividend increase in the past six quarters, raising the quarterly payout to $0.10 per share.

The first quarter suggests Pitney Bowes' turnaround is evolving beyond cost-cutting into stronger cash generation and capital discipline. The key question now is whether improving operations across SendTech and Presort can sustain this momentum, turning one strong quarter into a lasting cash flow story.

How Does Pitney Bowes' Cash Flow Recovery Compare With Peers?

Pitney Bowes' improving cash flow profile stands out within a competitive landscape dominated by logistics leaders such as FedEx Corporation FDX and United Parcel Service Inc. UPS. While all three companies are prioritizing profitability and shareholder returns over volume growth, their paths to stronger cash generation differ considerably.

FedEx is leveraging its massive global transportation network to drive free cash flow through Network 2.0, structural cost reductions and disciplined capital spending. The company generated $4.7 billion in adjusted free cash flow during fiscal 2026 and remains focused on achieving $6 billion by calendar 2029 while continuing dividend increases and share repurchases. Growth in premium B2B markets, healthcare, AI and data-center logistics is providing additional support for FDX’s earnings and cash generation.

UPS, meanwhile, continues to emphasize higher-quality revenues by focusing on healthcare logistics, small and medium-sized businesses, and premium parcel services while reducing exposure to lower-margin volumes. UPS’ strategy is centered on expanding margins and strengthening free cash flow through disciplined network optimization and pricing rather than aggressive shipment growth.

PBI’s Stock Price Performance & Valuation Trend

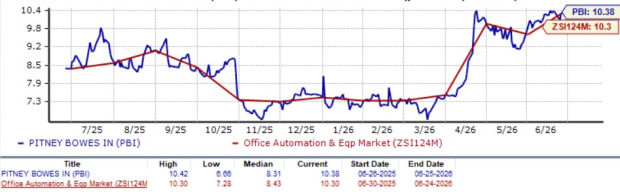

Shares of Pitney Bowes have surged 61% in the past three months, outperforming the Zacks Office Automation and Equipment industry, the broader Computer and Technology sector and the S&P 500 index.

Image Source: Zacks Investment Research

PBI stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 10.38, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of PBI

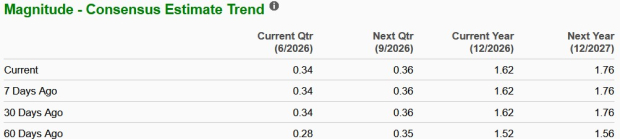

PBI’s earnings estimates for 2026 and 2027 have trended upward in the past 60 days to $1.62 and $1.76 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 20% and 8.4%, respectively.

Image Source: Zacks Investment Research

PBI stock currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Pitney Bowes Inc. (PBI): Free Stock Analysis Report

United Parcel Service, Inc. (UPS): Free Stock Analysis Report

FedEx Corporation (FDX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).