Cincinnati Financial Corporation’s CINF shares have risen 31.3% in a year, outperforming the industry’s growth of 7.2%. Its share price closed at $192.03 on Thursday and reached a 52-week high of $192.09, reflecting investor confidence.

Strong underwriting performance, healthy premium growth, improved pricing and higher investment income, along with a robust capital position, have increased investors' confidence. The company has surpassed earnings estimates in each of the last four quarters, with an average of 27.5%. While its premium valuation may limit multiple expansion, continued underwriting discipline, healthy premium growth and improving investment income should support long-term earnings growth.

Cincinnati Financial’s shares have outperformed its peers, including Arch Capital Group Ltd. ACGL and W.R. Berkley Corporation WRB, which have gained 14.3% and 1.9%, respectively, while Palomar Holdings, Inc. PLMR has lost 3.7% in a year.

1-Year Price Performance: CINF, ACGL, WRB, PLMR & Industry

Image Source: Zacks Investment Research

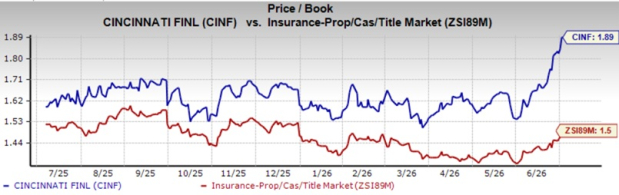

CINF’s Premium Valuation

Cincinnati Financial’s shares are trading at a premium to the industry. Its price-to-book value of 1.89X is higher than the industry average of 1.5X. However, it has a Value Score of B.

Image Source: Zacks Investment Research

CINF’s Growth Projection Encourages

The Zacks Consensus Estimate for Cincinnati Financial’s 2026 earnings per share (EPS) is pinned at $8.66, indicating a year-over-year increase of 8.9%. The estimate for 2026 revenues is pegged at $12.05 billion, implying a year-over-year improvement of 7.7%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 4.9% and 6.6%, respectively, from the corresponding 2026 estimates.

The expected long-term earnings growth is pegged at 5.3%. It has a Growth Score of B.

CINF’s Higher Return on Equity

Return on equity in the trailing-12 months was 10.6%, better than the industry average of 7.4%. This highlights the company’s efficiency in utilizing shareholders’ funds.

Factors Acting in Favor of CINF

Cincinnati Financial’s Commercial Lines Insurance segment has been consistently witnessing growth over the past several quarters, led by disciplined pricing, policy-level risk selection and strong independent agency relationships. The company continues to leverage its agency-centric model to expand Commercial Lines through deeper agency relationships, expand its product offerings and drive profitable premium growth. Its disciplined underwriting approach and focus on risk selection should continue to support Commercial Lines' profitability despite a moderating pricing environment.

Cincinnati Financial continues to strengthen its diversified insurance platform through pricing discipline and targeted growth initiatives. Management expects property and casualty underwriting results to benefit from continued price increases and the expansion of Cincinnati Re and Cincinnati Global, which enhance pricing precision, broaden product offerings and improve income stability.

The Excess & Surplus (E&S) business continues to benefit from strong new business, favorable renewal pricing and product expansion. Meanwhile, Personal Lines remains a key growth driver, which is supported by the Cincinnati Private Client business, higher renewal pricing and geographic diversification. These businesses diversify earnings, reduce volatility and support long-term profitable growth.

Net investment income increased 14% year over year in the first quarter of 2026, driven by higher reinvestment yields, growth in fixed-income investments, and robust operating cash flows, which more than doubled year over year to $656 million in the first quarter of 2026. Backed by a large, high-quality investment portfolio, these factors continue to provide a meaningful earnings tailwind alongside underwriting operations.

Cincinnati Financial’s expansion strategy is driven by its exclusive partnerships with local, independent insurance agencies. This relationship-based model fosters strong customer loyalty, high retention rates and consistent business growth. As the insurer expands its agency network into underserved markets, it remains well-positioned to drive sustainable premium growth, deepen market penetration and create long-term shareholder value.

Cincinnati Financial has returned capital to its shareholders through share buybacks, dividend hikes and special dividends. It has an excellent track record of raising dividends for 65 straight years. Its dividend yield of 2.% is better than the industry average of 0.3%, making the stock an attractive pick for yield-seeking investors.

Risks for CINF Stock

Cincinnati Financial’s results remain sensitive to catastrophe activity, particularly in property lines, and severity can vary sharply by period. Although reinsurance provides protection, elevated catastrophe losses could pressure underwriting margins.

Management continues to emphasize risk selection and segmentation, but rising loss costs, social inflation, larger jury awards and increasing claim severity could pressure profitability despite conservative reserves.

Conclusion

Strong performance at the Commercial Lines segment, pricing discipline, agent-focused business models, higher investment income, consistent cash flow and prudent capital deployment support growth. However, exposure to catastrophe losses and loss-cost trends, including social inflation, remains a risk.

Higher return on equity, favorable growth estimates and an impressive dividend history should continue to benefit Cincinnati Financial over the long term. A VGM Score of A instils confidence. Given the premium valuation, it is wise to adopt a wait-and-see approach on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cincinnati Financial Corporation (CINF): Free Stock Analysis Report

W.R. Berkley Corporation (WRB): Free Stock Analysis Report

Arch Capital Group Ltd. (ACGL): Free Stock Analysis Report

Palomar Holdings, Inc. (PLMR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).