Gross bookings at Uber Technologies UBER, the San Francisco-based ride-hailing giant, continue to grow despite geopolitical tensions because demand for its services remains strong. Notwithstanding the current turbulent scenario, people need rides to go to work, airports, restaurants and events, while food and grocery delivery continues to be part of everyday life. Uber also benefits from operating in many countries, so weaknesses in one market are often offset by strengths in others.

In addition, the company's Uber One membership program, expanding delivery business and ongoing improvements in its app are encouraging customers to use the platform more often and spend more, helping drive higher gross bookings.

Higher gross bookings are benefiting Uber by increasing both revenues and profitability. As more customers use the platform, Uber earns more fees while keeping costs under control, allowing profits and free cash flow to grow faster. Strong booking growth also attracts more drivers and merchants to the platform, making the service more reliable and improving the customer experience.

Despite the crisis in the Middle East, UBER’s Mobility business saw impressive demand in first-quarter 2026, with segmental revenues increasing 5% year over year on a reported basis and 1% on a constant currency basis to $8.2 billion.

Gross bookings from the unit were highly impressive, aiding the first-quarter results. Gross bookings from the Mobility segment in the March quarter increased 20% year over year on a constant-currency basis to $26.4 billion. Uber’s Delivery business also performed well in the quarter, with segmental revenues growing 23% year over year on a constant-currency basis. Gross bookings from the Delivery segment in the first quarter rose 23% year over year on a constant-currency basis to $26 billion. Total gross bookings jumped 25% to $53.7 billion, ahead of the Zacks Consensus Estimate of $52.9 billion.

The gross bookings forecast for the second quarter of 2026 is also very impressive, highlighting the bullishness surrounding the key metric. Despite the ongoing tensions in the Middle East and the resultant fuel price spike, gross bookings are projected in the range of $56.25-$57.75 billion, highlighting growth of 18% to 22% year over year on a constant-currency basis. The outlook assumes a roughly 2 percentage-point currency tailwind to total reported year-over-year growth.

Comparable Metrics of Other Ride-Hailing Entities

Gross bookings are strong at rival Lyft LYFT as well, mainly owing to the growing active rider base, expansion into new markets and the success of its customer-friendly "Price Lock" feature. In the March quarter, gross bookings increased 19% year over year to $4.9 billion at Lyft. This was the 20th consecutive quarter where Lyft demonstrated double-digit year-on-year growth in the key metric, demonstrating the resilience and momentum of its customer-friendly strategy. Active Riders increased 17% year over year to 28.3 million.

For the second quarter of 2026, Lyft anticipates gross bookings to grow 18-21% year over year, reaching $5.3-$5.43 billion.

Singapore-based Grab GRAB is benefiting from strong growth in its On-Demand Gross Merchandise Value (“GMV”). On-Demand GMV refers to the sum of GMV of the mobility and deliveries segments. In the first quarter of 2026, On-Demand GMV increased 21% year over year (on a constant currency basis) at Grab. Grab expects 2026 revenues between $4.04 billion and $4.1 billion, indicating 20-22% year-over-year growth.

UBER’s Share Price Performance, Valuation and Estimates

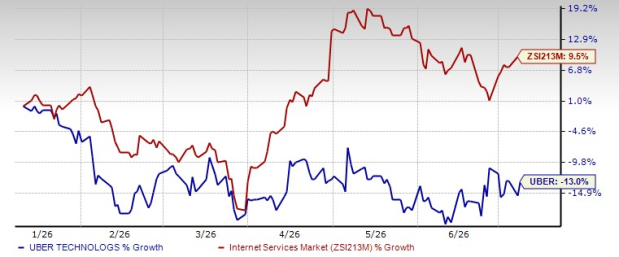

Shares of UBER have declined in double digits over the past six months. Courtesy of the downbeat performance, UBER’s shares have underperformed the Zacks Internet-Services industry over the same time frame.

6-Month Price Comparison

From a valuation standpoint, UBER trades at a 12-month forward price-to-sales of 2.42X. UBER is inexpensive compared with its industry.

See how the Zacks Consensus Estimate for Uber’s earnings has been revised over the past 90 days.

Uber’s Zacks Rank

Uber currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Uber Technologies, Inc. (UBER): Free Stock Analysis Report

Lyft, Inc. (LYFT): Free Stock Analysis Report

Grab Holdings Limited (GRAB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).