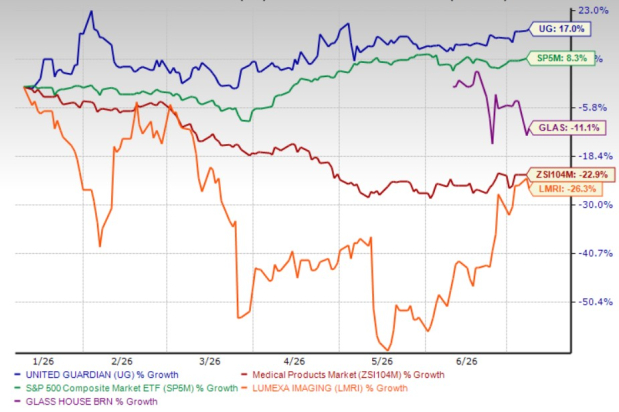

United-Guardian, Inc. UG has delivered an impressive market performance over the past six months, with its shares climbing 17%. The stock has significantly outperformed peers Lumexa Imaging Holdings, Inc.’s LMRI decline of 26.3% and Glass House Brands Inc.’s GLAS fall of 11.1% over the same period. UG has also held up far better than its broader industry’s decline of 22.9% and the S&P 500's 8.3% return. This strong performance reflects investors' confidence in the company's improving operating trends and growth initiatives.

Following this rally, the key question for investors is whether United-Guardian still offers attractive upside or whether the recent appreciation has already priced in much of its near-term potential.

Commercial Expansion Opens Growth Avenues

United-Guardian continues to expand its addressable market through targeted commercial initiatives. In January 2026, the company signed a distribution agreement with Brenntag Specialties to market its Natrajel sexual wellness ingredient portfolio across the United States, Canada and Mexico. The agreement also broadens the distribution of Lubrajel and Natrajel products in France, strengthening the company's international presence.

Management believes that the sexual wellness ingredients business has the potential to grow faster than its traditional personal care segment, creating an additional long-term revenue opportunity.

At the same time, the company is expanding the commercial reach of Renacidin through an insurance payer outreach program following formulary approvals from two major pharmacy benefit managers, effective in 2026. A newly launched physician awareness initiative supports the wider adoption of the product. Collectively, these efforts position United-Guardian to generate incremental revenues while reducing the dependence on its existing customer base.

Broad-Based Revenue Growth Supports Earnings Momentum

United-Guardian delivered a strong first-quarter 2026 performance, with net sales increasing 15.8% year over year to $2.87 million from $2.48 million. The rally was driven by strength across both its major operating segments.

Pharmaceutical sales rose 24% year over year to $1.45 million, benefiting from higher demand for Renacidin and Clorpactin. Cosmetic ingredient sales climbed 21% to $844,000, supported by stronger purchases from its largest distributor, Ashland Specialty Ingredients (“ASI”). Despite higher operating expenses, the increase in revenues enabled operating income to improve 5% year over year to $642,000.

Importantly, revenue growth across multiple product categories provides a healthier earnings profile than the reliance on a single business line, enhancing the company's long-term financial stability.

Normalized Distributor Demand Improves Cosmetic Business Outlook

Another encouraging development is the recovery in purchasing activity from Ashland Specialty Ingredients. During 2025, ASI had significantly reduced purchases as it worked through excess inventory, creating a temporary headwind for United-Guardian's cosmetic ingredients business.

Management has indicated that this inventory correction has now largely concluded. ASI's purchases increased approximately 45% year over year in the first quarter of 2026, contributing substantially to the segment's 21% sales growth. The normalization of ordering patterns restores an important revenue stream and suggests that cosmetic ingredient sales could remain more consistent in the coming quarters, improving visibility into future operating performance.

Trade & Supply-Chain Risks Remain a Key Overhang

While the company's operating momentum has improved, investors should remain mindful of several external risks.

Management noted that evolving U.S. trade policies introduced during 2025, including higher tariffs and retaliatory measures from trading partners, continue to create uncertainty around pricing, sales volumes, logistics and raw material availability. In addition, geopolitical tensions in several oil- and gas-producing regions have increased freight costs while contributing to greater volatility in petrochemical-based raw material prices.

Given United-Guardian's reliance on internationally sourced inputs and global markets, prolonged trade disruptions or higher input costs could pressure margins and weigh on future profitability.

Valuation

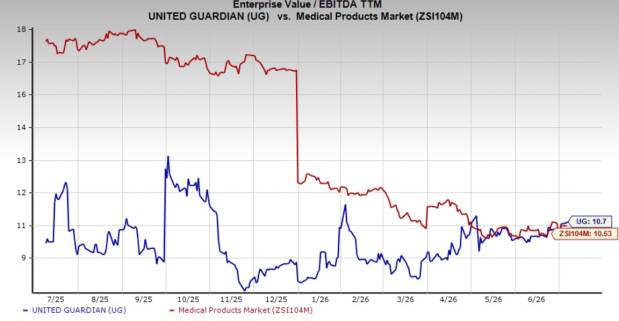

From a valuation standpoint, United-Guardian no longer appears particularly inexpensive. The stock currently trades at a trailing 12-month EV/EBITDA multiple of 10.7X, modestly above the broader industry average of 10.53X.

Although the premium is relatively small, it suggests that investors have already recognized much of the company's recent operational improvement. With the stock trading slightly above industry valuation despite ongoing macroeconomic and supply-chain uncertainties, the margin of safety appears somewhat limited.

Should Investors Buy UG Stock Now?

United-Guardian has strengthened its investment case through expanding distribution partnerships, improving pharmaceutical sales, recovering cosmetic ingredient demand and broader commercial initiatives that could support sustainable long-term growth. The company's first-quarter results also demonstrate healthy execution across multiple business segments, providing greater confidence in its earnings outlook.

However, unlike many undervalued opportunities, UG currently trades at a slight premium to the industry average. Combined with continuing tariff uncertainty, raw material cost pressures and geopolitical risks, the current valuation leaves less room for execution missteps.

Overall, long-term fundamentals remain encouraging, but investors may be better served waiting for a more attractive entry point rather than chasing the stock after its recent rally.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

United-Guardian, Inc. (UG): Free Stock Analysis Report

Lumexa Imaging Holdings, Inc. (LMRI): Free Stock Analysis Report

Glass House Brands Inc. (GLAS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).