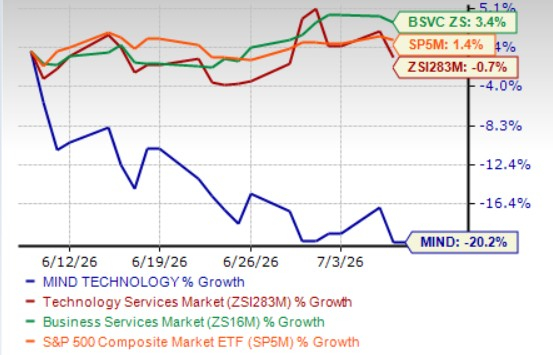

MIND Technology, Inc. MIND shares have lost 20.2% in the past month compared with the industry’s 0.7% decline. It has also lagged the broader Zacks Business Services sector’s 3.4% rise and the S&P 500’s 1.4% increase in the said time frame. The company has been grappling with persistent customer spending delays, declining order backlog, weaker revenue visibility and intense pricing competition.

Image Source: Zacks Investment Research

What’s Weighing on MIND’s Performance?

MIND Technology continues to face a challenging near-term demand environment as macroeconomic uncertainty, geopolitical tensions and limited customer visibility delay capital spending decisions. Management noted that customers remain hesitant to commit to large marine exploration and survey equipment purchases, particularly high-value system orders, resulting in slower order conversions and reduced revenue visibility despite a healthy long-term opportunity pipeline.

The company’s order backlog has declined significantly as previously delayed shipments were fulfilled, while new customer commitments remained slow. Firm backlog fell to approximately $7.6 million as of April 30, 2026 from $13.9 million at the fiscal year-end, reflecting prolonged customer decision-making rather than demand destruction. This weaker backlog could pressure near-term revenue, especially if expected pipeline opportunities take longer than anticipated to convert into firm contracts.

Management expects fiscal 2027 revenues to decline from fiscal 2026 levels because replicating the unusually strong system order volumes of the past two years will be difficult under current market conditions. The company also acknowledged that uncertainty surrounding exploration spending, combined with the timing of large projects, may create quarterly revenue volatility, making financial performance less predictable over the near term.

MIND Technology operates in a highly competitive marine technology industry, where purchasing decisions are driven by factors such as product quality, technological innovation, operational reliability and cost competitiveness. To sustain its market position, the company must continually invest in product development, enhance its technological capabilities and deliver strong customer support. Since many contracts are awarded through competitive bidding, pricing pressure and the emergence of advanced competing solutions could limit order wins or compress margins.

Stock Valuation

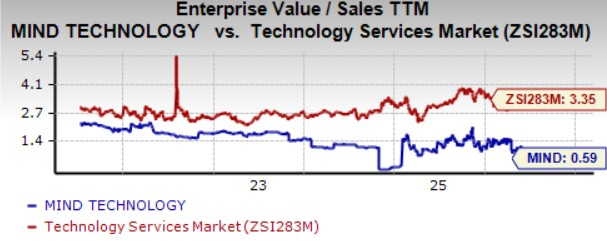

The stock is currently trading at a discount compared with the historical levels and industry average. It is trading at a trailing 12-month EV/sales multiple of 0.59X compared with the past five-year median of 1.5X and the industry’s figure of 3.35X. It is also lower than two of the company’s peers, Priority Technology Holdings, Inc. PRTH and Ralliant Corporation RAL, which stood at 1.55X and 3.99X, respectively.

Image Source: Zacks Investment Research

Can MIND Power Through the Challenges?

The company's expanding high-margin aftermarket business, which generates recurring revenues from spare parts, repairs and support services, remains a strength. Aftermarket activities contributed 50% of first-quarter fiscal 2027 revenues, providing resilience during periods of slower system orders. Coupled with a debt-free balance sheet, strong liquidity, ongoing cost optimization and opportunities to expand into offshore wind, carbon capture and other marine applications, MIND is well positioned for sustainable long-term growth.

A strong financial position and disciplined capital allocation strategy are added positives. The company maintains a debt-free balance sheet, significant working capital and ample liquidity, providing flexibility to pursue organic growth initiatives, strategic acquisitions and product expansion. Management believes this financial strength enhances its ability to capitalize on emerging opportunities while continuing to invest in innovation and long-term shareholder value creation.

Wrapping Up

Despite near-term headwinds from delayed customer spending, weaker backlog and revenue uncertainty, MIND Technology's resilient high-margin aftermarket business, debt-free balance sheet, strong liquidity and expanding opportunities in adjacent marine markets position it well to navigate the current downturn. Also, the stock seems undervalued at the moment. Therefore, the decline in its share price presents a lucrative opportunity for investors to add the stock to their portfolio.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

MIND Technology, Inc. (MIND): Free Stock Analysis Report

Priority Technology Holdings, Inc. (PRTH): Free Stock Analysis Report

Ralliant Corporation (RAL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).