Sezzle Inc. SEZL has been one of the more exciting names in buy now, pay later, and the rally in SEZL has naturally made investors ask a simple question: Is the move already done, or is there still upside left?

The stock has earned attention because the business is not just growing; it is growing profitably. That matters in a fintech market where PayPal Holdings, Inc. PYPL and Shift4 Payments, Inc. FOUR still draw plenty of investor focus, but where investors are rewarding companies that can show clean execution.

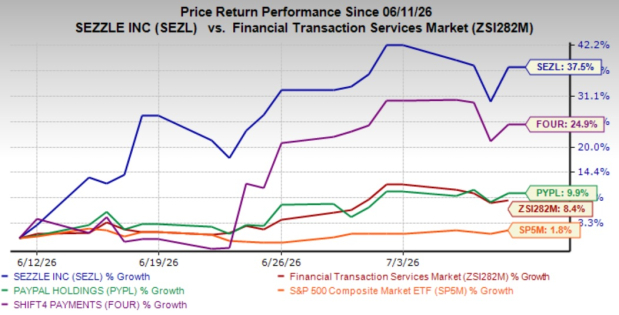

SEZL’s price performance has already been sharp, and that creates a higher bar. Over the past month, the company has rallied more than 37%, well ahead of its industry’s increase of 8.4%. Meanwhile, peers like PayPal Holdings and Shift4 Payments have risen 9.9% and 24.9%, respectively, while the S&P 500 composite has inched up 1.8%.

One-Month Price Performance

Image Source: Zacks Investment Research

SEZL’s Earnings Power is Driving the Thesis

Sezzle’s first-quarter 2026 results provide a strong foundation for the bullish case. Gross merchandise volume (GMV) rose 37.3% year over year to roughly $1.1 billion, while total revenues increased 29.2% to $135.5 million. Net income reached $51.3 million, equal to a 37.9% profit margin, and adjusted EBITDA was $71.1 million, representing a 52.5% margin.

Sezzle is not relying only on volume growth. The company is converting growth into earnings at a high rate, which gives the stock a stronger fundamental base after its rally. For a fintech company operating in a credit-sensitive category, that combination of revenue growth and profitability is especially important.

Management also raised its full-year 2026 outlook. Sezzle now expects revenue growth of 30-35%, adjusted net income of $180 million and adjusted EPS of $5.10. This guidance gives investors a clearer earnings anchor when thinking about valuation. SEZL is not a low-multiple stock after its run, but the premium looks more defensible if earnings continue scaling at this pace.

Sezzle’s Engagement Trends Point to Quality Growth

The strongest part of Sezzle’s operating story is user engagement. Average quarterly purchase frequency increased to 7.1 times from 6.1 times a year earlier. Active consumers reached about 3.1 million, while monthly on-demand users and subscribers stood at 887,000.

This matters because higher purchase frequency can support better unit economics over time. A customer who uses Sezzle more often is more valuable than one who appears only at checkout once or twice. The company’s subscriber base also continues to move in the right direction, with subscribers rising by 44,000 in the quarter to 714,000.

That subscriber focus is central to the investment thesis. Sezzle is prioritizing users with higher lifetime value, stronger repeat behavior and better engagement across the platform. This should help reduce dependence on one-time transactions and create a more durable revenue stream.

Product Expansion Adds Upside Optionality for SEZL

Sezzle is also widening its product set beyond its original Pay-in-4 offering. Pay-in-5, enhanced long-term lending, the virtual card in Canada and Sezzle Mobile all add more ways for consumers to use the platform. These products may not all become major profit drivers immediately, but they increase the number of touchpoints between Sezzle and its customers.

The company is also using AI to improve efficiency. Its AI support chatbot is resolving roughly 60-70% of chats without escalation, while internal tools are being used across chargebacks, support, business intelligence and engineering. That operating discipline is important because it supports margin expansion while the business continues to grow.

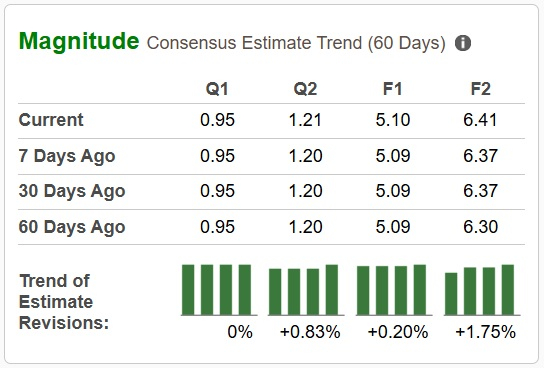

SEZL’s Estimate Revisions Depict a Bright Outlook

Over the past week, earnings estimates for both 2026 and 2027 have been revised marginally upward, signaling a bullish outlook from analysts. These figures also suggest year-over-year growth of 42.06% and 25.74%, respectively.

Image Source: Zacks Investment Research

Valuation is the Main Risk for SEZL

The main concern is valuation. SEZL’s rally has already priced in a lot of optimism, so the company needs to keep delivering strong quarters. The stock trades at 8.88X forward 12-month sales per share versus 5.00X for the Zacks sub-industry. This is no longer cheap, but it looks fair for a fintech growing revenue around 30% to 35% and producing strong adjusted EBITDA.

On the other hand, PYPL trades at 1.14X forward 12-month sales per share, while FOUR trades near 1.44X forward 12-month sales per share.

Image Source: Zacks Investment Research

Competition also remains a watch item, especially as PayPal and Shift4 Payments continue shaping investor expectations for BNPL and digital payments. Still, Sezzle’s current momentum is being driven by its own execution rather than broad sector enthusiasm alone.

Conclusion: SEZL Still Looks Like a Buy

SEZL has already rallied hard, but the move does not look empty. Sezzle is growing GMV, expanding revenue, lifting guidance, improving engagement and producing strong profits. Valuation is no longer cheap after the rally, and that raises the need for consistent execution. PayPal and Shift4 Payments remain important BNPL and payments peers, yet Sezzle offers a cleaner, high-growth, high-margin story.

Guidance, margins and subscriber growth support the view that the business can grow into its higher expectations. With earnings momentum still strong and multiple growth levers in place, SEZL remains a Buy for investors comfortable with volatility. Estimate revisions also echo a similar sentiment, and therefore, for investors, the recent rally looks justified rather than excessive.

At present, SEZL carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sezzle Inc. (SEZL): Free Stock Analysis Report

PayPal Holdings, Inc. (PYPL): Free Stock Analysis Report

Shift4 Payments, Inc. (FOUR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).