Toast, Inc. TOST has built a strong name in restaurant technology by giving operators tools to manage payments, ordering, marketing, payroll, inventory and daily workflows from one platform. The company’s appeal is clear: restaurants are busy, margins are often tight, and owners want technology that saves time while helping them bring in more sales.

For investors, TOST has become a stock to watch because the business is moving past the early growth stage and showing stronger profitability. The company is still expanding locations, but it is also selling more products to existing customers. That mix gives Toast a chance to grow revenue while improving margins.

The stock has reflected that optimism. TOST has recovered sharply from earlier weakness, supported by better earnings, improving cash generation and enthusiasm around AI-led products.

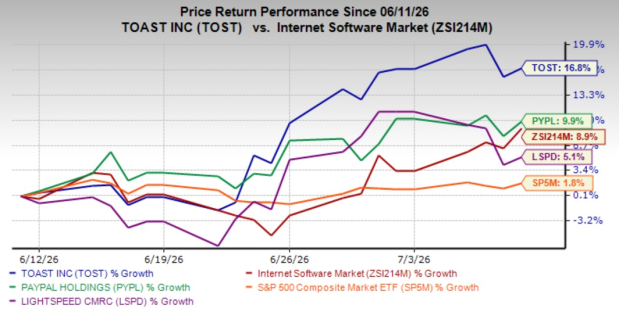

Over the past month, TOST has rallied more than 16%, well ahead of the industry’s increase of 8.9%. Meanwhile, peers like PayPal Holdings PYPL and Lightspeed Commerce Inc. LSPD have risen 9.9% and 5.1%, respectively, while the S&P 500 composite has inched up 1.8%.

One-Month Price Performance

Image Source: Zacks Investment Research

Toast’s Growth Engine Still Looks Healthy

Toast’s latest results show that demand remains solid. In the first quarter of 2026, the company’s recurring gross profit increased 27% and the annualized recurring run-rate increased 26%. It also added 7,000 net locations, ending the quarter with 171,000 live locations, up 22% from a year earlier.

That location growth is important because it gives Toast more customers to sell into over time. The company does not need to rely only on basic payment processing. It can add subscription software, fintech tools, marketing products, payroll services and other features that make the platform more valuable for restaurants.

Profitability is also moving in the right direction. Adjusted EBITDA reached $179 million in the quarter, and GAAP operating income margin crossed 20% for the first time. SaaS gross margin also moved above 80%, showing that Toast’s software revenue can carry attractive economics as the company scales.

AI Could Support the Next Phase for TOST

Toast is putting more focus on AI, and this could become a key part of the next growth cycle. Toast IQ is designed to help restaurant operators spot trends, find revenue opportunities and make faster decisions. Management said Toast IQ had 40,000 weekly active locations, suggesting that customers are already using the product in meaningful numbers.

Toast IQ Grow is another promising area. It helps restaurants build and manage marketing campaigns across channels such as email, SMS and social media. Management said pilot customers using Toast IQ Grow saw an average 8% sales increase compared with similar Toast restaurants.

This matters because many restaurant owners do not have the time or staff to run advanced marketing, reporting or back-office tasks on their own. If Toast can use AI to take more work off its plate, it may be able to increase customer loyalty and drive stronger monetization.

Expansion Adds More Runway for Toast

Toast is not limiting itself to small and mid-sized restaurants. The company is also moving into enterprise chains, international markets and retail. In enterprise, it has launched products such as drive-thru support and continues to win larger operators. Internationally, it is focusing on dense, high-value cities where restaurants are likely to benefit from handhelds and operational tools.

Retail is still early, but it gives Toast another possible growth path. Grocery is a near-term focus, and management said Toast serves more than 100 grocery locations with more than $5 million in sales. That suggests the platform could work beyond traditional restaurants, especially for businesses that need payments, inventory and workflow tools in one place.

But Toast Faces Concerns

Restaurant demand is a concern. GPV per location declined 1% in the first quarter, and management described consumer trends as stable rather than especially strong. If diners pull back, Toast may still add locations, but payment volume and customer expansion could become harder.

Costs also deserve attention. Hardware and professional services remain a drag, and management noted that tariff-related costs and inventory planning could weigh on results. The company expects the 2027 hardware impact on the profit and loss statement to be larger than in 2026, although it does not expect a long-term structural hit.

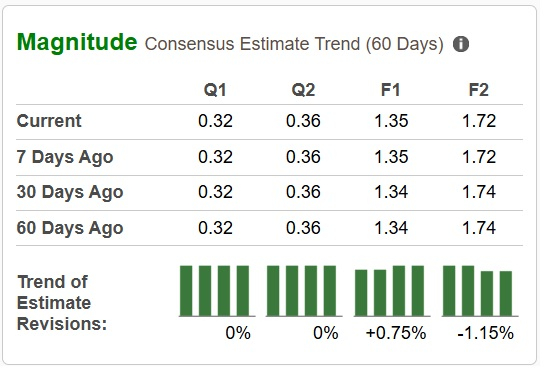

TOST’s Estimate Revisions Depict a Mixed Outlook

Over the past 30 days, earnings estimates for 2026 have been revised marginally upward, while the same for 2027 have been tweaked below, signaling a mixed outlook. However, these figures also suggest year-over-year growth of 51.69% and 27.04%, respectively.

Image Source: Zacks Investment Research

TOST’s Valuation Looks Supportable on Forward Sales

TOST trades at 1.85X forward 12-month sales per share versus 3.98X for the Zacks sub-industry. This valuation disparity might not be as favorable as it seems. On the other hand, PayPal trades at 1.14X forward 12-month sales per share, while Lightspeed Commerce trades near 1.09X forward 12-month sales per share.

The Value Score of C suggests that Toast may not be a bargain at current levels.

Image Source: Zacks Investment Research

Conclusion: Hold TOST Stock

Toast is a strong company with real growth, improving margins and a clear product strategy. Its restaurant focus, rising location count, AI roadmap and new-market expansion all support the long-term story. Compared with PayPal and Lightspeed Commerce, Toast looks more specialized.

Still, the stock’s rally has made the setup less one-sided. TOST looks like a quality business, but hardware costs and restaurant demand create enough risk to avoid chasing the shares aggressively. Therefore, it seems prudent for existing investors to continue holding the stock, while new investors may want to wait for a better entry point.

At present, TOST carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Toast, Inc. (TOST): Free Stock Analysis Report

PayPal Holdings, Inc. (PYPL): Free Stock Analysis Report

Lightspeed Commerce Inc. (LSPD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).