Primo Brands Corporation PRMB gives investors a mixed case. Sales are improving, premium brands are gaining traction and cash generation remains useful.

The problem is conversion. Margins, leverage and integration costs still make the near-term payoff less clear, which supports patience over aggressive buying.

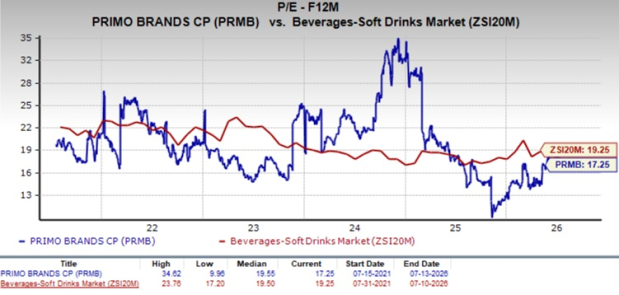

PRMB Valuation Looks Reasonable, Not Cheap

PRMB trades at 17.25X forward 12-month earnings. That is below the industry’s 19.25X and the S&P 500’s 21.23X, but slightly above the Zacks Consumer Staples sector’s 16.96X.

The stock also trades below its five-year median of 19.55X. Its five-year range runs from 9.96X to 34.62X, so today’s multiple is not extreme.

Image Source: Zacks Investment Research

Valuation alone does not settle the debate. A lower-than-market multiple is more useful when earnings quality is improving, and PRMB has not yet shown that consistently.

Primo Brands Has Real Sales Momentum

Comparable net sales increased 1.7% year over year in the first quarter of 2026. The gain included a 1.3% contribution from price and mix and a 0.4% contribution from volume.

Management raised 2026 comparable organic net sales growth guidance to 1%-3% from its prior flat-to-1% range. Retail trends improved across channels such as mass, club and away-from-home.

Premium water is the strongest part of the story. Premium water sales rose 42.8% to $105.5 million, while Saratoga and The Mountain Valley together grew 43%.

New distribution, added displays and Amazon Grocery availability give the sales case more support. Capacity investments, including Saratoga’s Texas capacity and The Mountain Valley’s new facility, also support premium mix.

The Coca-Cola Company KO remains a relevant comparison because its waters and hydration portfolio includes brands such as Dasani and smartwater. PepsiCo Inc. PEP is another useful reference point through Aquafina and LIFEWTR.

PRMB Earnings Quality Still Needs Work

The earnings side remains weak. Earnings from continuing operations fell to 7 cents per share from 9 cents in the year-ago quarter.

Adjusted earnings declined to 23 cents per share from 29 cents. Gross margin also fell to 28.6% from 32.3%, showing that costs absorbed much of the sales improvement.

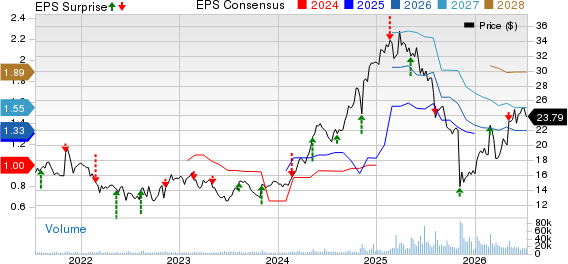

Primo Brands Corporation Price, Consensus and EPS Surprise

Primo Brands Corporation price-consensus-eps-surprise-chart | Primo Brands Corporation Quote

Operating income declined to $138 million from $153.2 million. Adjusted EBITDA fell 10.4% to $306 million.

Comparable adjusted EBITDA margin contracted 260 basis points to 18.8%. Higher Direct Delivery service spending, severe winter weather, tighter freight markets, incremental logistics costs and integration-related costs limited operating leverage.

Primo Brands Has Cash Flow Support

Cash flow keeps the investment case from turning too negative. Adjusted free cash flow improved $73.9 million year over year to $128.6 million in the first quarter.

Primo Brands maintained 2026 adjusted free cash flow guidance of $790-$810 million. Total liquidity stood at $874 million at quarter end.

The company refinanced its $3.1 billion term loan through 2031, reducing near-term refinancing pressure. It also paid a 12-cent quarterly dividend and repurchased $29 million of stock in the quarter.

Still, the balance sheet requires attention. Net leverage was 3.52X, and ongoing integration adjustments continue to make reported earnings and cash flow harder to read cleanly.

PRMB Ranking Signals Support a Hold View

The bottom line is that PRMB has visible operating positives, but not enough margin clarity to make the stock a straightforward buy. Sales momentum and cash flow support the case for ownership, while earnings quality argues for caution.

The stock currently carries a Zacks Rank #3 (Hold). That rank fits a company with improving sales signals but no clean all-clear on profitability.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

PRMB has a Value Score of B, Growth Score of B, Momentum Score of C and VGM Score of B. The B grades point to decent valuation and growth characteristics, while the Momentum Score of C keeps the timing backdrop more neutral.

For now, PRMB looks better suited for investors willing to wait for margin recovery than those looking for a clear buying signal today.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Primo Brands Corporation (PRMB): Free Stock Analysis Report

CocaCola Company (The) (KO): Free Stock Analysis Report

PepsiCo, Inc. (PEP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).