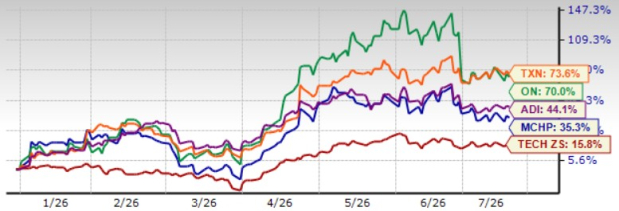

Microchip MCHP shares have jumped 35.3% year to date (YTD), outperforming the Zacks Computer and Technology sector’s appreciation of 15.8%. The outperformance can be attributed to a combination of a cyclical semiconductor recovery, execution on management's turnaround plan, improving profitability and growing AI, as well as data center exposure. However, the company’s prospects remain challenging due to supply chain constraints, rising costs and stiff competition from the likes of Texas Instruments TXN, Analog Devices ADI and On Semiconductor ON.

YTD, Microchip shares have underperformed Texas Instruments, Analog Devices and On Semiconductor, shares of which have returned 73.6%, 44.1% and 70%, respectively. Nevertheless, we believe MCHP’s share price is well-poised to appreciate, driven by expansion into higher-value AI infrastructure as well as recovery across industrial and automotive end markets. So, what should investors do with the stock? Let’s dig deep to find out.

MCHP Stock’s Price Performance

Image Source: Zacks Investment Research

MCHP’s Prospects to Ride on AI Tailwinds and Inventory Recovery

Improving fundamentals, along with rightsizing of manufacturing footprint, overhauling of distribution strategy and improving customer relationships, bodes well for Microchip’s prospects. This, along with reducing inventory level, a fall in net leverage below 3 times and strong free cash flow generation ability, bodes well for the company’s prospects.

Microchip has been benefiting from reducing inventory levels and expects inventory to be aligned with its long-term target in a short span of time. Management stated that inventory has reduced from 201 days in December to 185 days in March, while distributor inventory declined to 26 days, near the low end of the company’s historical range. MCHP management stated distributors have begun restocking, with April representing the highest booking month in almost four years. The company now expects book-to-bill well above 1, which reflects improving revenue visibility.

Microchip expects a broad-based recovery with strength across industrial, automotive, aerospace & defense, data center, and communications, which reduces investor concerns over cyclicality. Industrial remains roughly one-third of the company’s revenues, while automotive contributes about 17%. As customer inventories normalize, these historically strong markets should continue recovering alongside factory automation, electrification and embedded computing. MCHP is well positioned to benefit from the growing demand for mixed-signal microcontrollers (MCUs), leveraging its expanding footprint in industrial embedded control, broad product portfolio and total system solutions strategy. Mixed-signal MCUs remain the company's largest product category, accounting for nearly 50% of fiscal 2026 revenues, highlighting their importance to long-term growth.

Data Center prospects are most noticeable as Data Center & Compute already represents 18% of company revenues. MCHP expects the dedicated Data Center solutions business to grow from roughly $303 million in calendar 2025 to approximately $500 million in calendar 2026 (about 65% growth), driven by strong momentum in PCIe Gen6 switches, expansion into PCIe retimers, new CXL memory controllers and storage controller growth driven by AI inference. In fact, Microchip has disclosed eight Gen6 switch design wins and expects production ramps during fiscal 2027, including one design expected to generate roughly $100 million annually.

MCHP’s Earnings Estimate Revision Shows Positive Trend

The Zacks Consensus Estimate for fiscal 2027 earnings is pegged at $3.09 per share, up by a penny over the past 30 days and indicating 90.85% growth over fiscal 2026’s reported figure. The consensus mark for fiscal 2027 revenues is pegged at $6.23 billion, suggesting 32.26% growth from fiscal 2026’s reported figure.

Microchip Technology Incorporated Price and Consensus

Microchip Technology Incorporated price-consensus-chart | Microchip Technology Incorporated Quote

Microchip expects first-quarter fiscal 2027 net sales between $1.442 billion and $1.469 billion, which reflects 35.3% year-over-year growth at the midpoint and 11% sequentially. The company expects non-GAAP earnings of 67-71 cents per share.

The Zacks Consensus Estimate for first-quarter fiscal 2027 earnings is pegged at 69 cents per share, unchanged over the past 30 days and indicating 159.26% growth over the year-ago quarter’s reported figure. The consensus mark for fiscal first-quarter revenues is pegged at $1.46 billion, suggesting 35.39% growth from the year-ago quarter’s reported figure.

MCHP Shares Are Trading at a Premium

Microchip shares are trading at a premium as suggested by a Value Score of D.

In terms of the forward 12-month price-to-sales (P/S), the company is trading at 7.2X, a premium compared with the broader sector’s and On Semiconductor’s 6.85X and 5.3X, respectively. However, MCHP is trading at a discount compared with Texas Instruments’ and Analog Devices’ P/S multiple of 12.54X and 11.99X, respectively.

MCHP Stock’s Valuation

Image Source: Zacks Investment Research

Conclusion

Microchip has emerged from one of the industry’s toughest downturns with improving execution, strengthening demand and expanding exposure to attractive long-term growth markets. Inventory normalization, broad-based recovery across industrial and automotive markets, growing AI and data center opportunities, and improving profitability provide a solid foundation for sustained growth. While supply chain constraints, cost inflation, and intense competition remain risks, MCHP’s strengthening bookings, healthy earnings outlook and disciplined turnaround strategy position it well for continued momentum. Despite its premium valuation, Microchip’s improving fundamentals and expanding AI infrastructure portfolio make the stock an attractive choice for investors with a long-term investment horizon.

Microchip currently has a Zacks Rank #2 (Buy), which implies that investors should start accumulating the stock right now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microchip Technology Incorporated (MCHP): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

ON Semiconductor Corporation (ON): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).