Lumen Technologies, Inc. LUMN is trading at a forward 12-month price-to-sales ratio of 0.66X, a discount compared with the Zacks Diversified Comm Services industry’s 1.67X and the Zacks Utilities sector’s 3.34X.

Image Source: Zacks Investment Research

The stock also looks attractively valued relative to other peers like Verizon Communications VZ, AT&T T and Cogent Communications CCOI with forward 12-month P/S of 1.47X, 1.57X and 0.93X, respectively.

Often, discounted valuation signals investor concerns surrounding growth, execution challenges or balance sheet concerns. However, an undervalued stock can also represent a potential buying opportunity when the underlying fundamentals begin to improve.

And that is where Lumen starts to attract investor attention.

With tremendous focus on AI-driven capabilities and balance sheet deleveraging, the company appears to be laying the groundwork for a potential turnaround.

So, is Lumen a value trap or a buying opportunity?

Let’s do a deep dive.

LUMN’s Push to Deleverage Balance Sheet

After years of battling a massive debt load, Lumen is now heavily focused on de-leveraging. The sale of Mass Markets' fiber-to-the-home business (including Quantum Fiber, across 11 states) to AT&T for $5.75 billion in cash marks a defining pivot.

Upon completion of the transaction, management used cash on hand and $4.8 billion in net proceeds to fully retire super-priority bonds, thereby lowering annual cash interest expense by an additional $300 million. Total debt has now reduced by more than $5 billion since January 2025. Over the past 12 months, Lumen executed seven refinancing transactions totaling more than $11 billion.

Annual interest expense has been reduced by nearly $500 million in the past 12 months, unlocking massive cash flow gains. It also previously eliminated second-lien debt.

The sale of the fiber-to-the-home business reduces annual capex by more than $1 billion, allowing Lumen to focus investment on enterprise and AI infrastructure.

LUMN’s Cost Discipline Measures

Lumen exceeded its 2025 cost-reduction target, achieving more than $400 million in run-rate savings. It now targets $700 million exiting 2026 and $1 billion by year-end 2027.

This cost optimization, combined with improving revenue mix, underpins guidance for adjusted EBITDA of $3.1-$3.3 billion in 2026, with management expecting it to inflect to growth this year. At the Investor Day held last month, LUMN added that it was working on boosting adjusted EBITDA margins to approximately the mid 30% range by 2030 from 27.1% reported in 2025.

Long Term Story: AI-Tied PCF Deals & NaaS Traction

Lumen is repositioning itself as “the trusted network for AI.” Management’s strategy is centered on three pillars: building the AI backbone, cloudifying the network and expanding a connected ecosystem of partners.

The explosive growth of AI workloads is driving demand for low-latency, high-bandwidth fiber connectivity between data centers, cloud regions and enterprise clients, resulting in increasing demand for Lumen's Private Connectivity Fabric (“PCF”) and network-as-a-service (NaaS) solutions. Driven by significant AI-fueled connectivity demand, Lumen has secured a total of $13 billion in PCF deals at the end of the fourth quarter of 2025.

Lumen has inked deals with various tech giants like Microsoft, Amazon, Google Cloud and Meta Platforms to provide the network capabilities for AI innovation. The company recognized revenues of $41 million and $116 million for the fourth quarter and full-year 2025, respectively, associated with the $13 billion in PCF deals.

Beyond fiber, Lumen is building the NaaS business, with its customer base now exceeding 2000. Lumen highlighted that active NaaS customers were up 29% sequentially in the fourth quarter. Fabric ports deployed increased 31% and the number of services sold surged 26% sequentially. Management remains upbeat about Internet on Demand, or IoD Offnet, and expects this solution to boost market reach with more than 900 off-net ports sold already. The company projects the current digital total addressable market of $23 billion in 2026 to increase to nearly $32 billion by 2030.

At its Investor Day, LUMN noted digital capabilities, including NaaS, Edge Solutions, Security and the Connected Ecosystem, to deliver between $500 million and $600 million of incremental revenues exiting 2028 and $800-$900 million by 2030. PCF business will yield $400-$500 million of recurring revenues exiting 2028 and $550-$650 million by 2030.

Lumen Technologies, Inc. Price, Consensus and EPS Surprise

Lumen Technologies, Inc. price-consensus-eps-surprise-chart | Lumen Technologies, Inc. Quote

Lumen remains upbeat about its connected ecosystem strategy (with over 16 ecosystem partners like Palantir, Commvault and QTS), which is producing tangible results with more than 180 potential sales opportunities as highlighted on the fourth-quarter earnings call.

While the growth factors appear compelling, risks remain. Lumen must sustain the cost-saving momentum while stabilizing revenues and managing its debt profile.

Despite deleveraging, the debt is still hovering at about $13 billion.

Further, as the company shifts toward newer growth products like fiber and cloud-based offerings, the secular headwinds in the legacy business will continue to prove a strain on the top-line expansion, at least in the near term. More importantly, management expects total revenue growth only in 2029, implying at least two to three more years of structural decline.

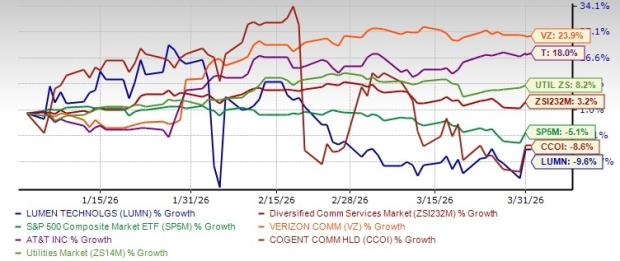

LUMN Stock in the Red

LUMN stock has disappointed in the first quarter of 2026, with the share price tanking 9.6%, underperforming the industry’s growth of 3.2%. The sector is up 8.2% while the S&P 500 is down 5.1% over the past three months.

Price Performance

Image Source: Zacks Investment Research

Verizon and AT&T stock prices have gained 23.9% and 18%, respectively, while Cogent is down 8.6%.

Cogent is a Tier 1 Internet Service Provider offering low-cost, high-speed Internet access, private network services and colocation services with ultra-low-latency data transmission. Verizon and AT&T are giants in the wireless communications space.

Value Trap or Buying Opportunity?

LUMN is aligning itself with the massive growth of AI, cloud computing and digital telecom services. Despite the competition in the AI space, increasing PCF demand and deals with tech giants are creating a strong foundation for growth. Expansion into NaaS markets is an additional tailwind. Extensive cost cuts and discounted valuation make LUMN a compelling investment opportunity.

At present, LUMN sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AT&T Inc. (T): Free Stock Analysis Report

Verizon Communications Inc. (VZ): Free Stock Analysis Report

Cogent Communications Holdings, Inc. (CCOI): Free Stock Analysis Report

Lumen Technologies, Inc. (LUMN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).